42 posts on "Systemic Risk"

February 17, 2022

How (Un‑)Informed Are Depositors in a Banking Panic? A Lesson from History

How informed or uninformed are bank depositors in a banking crisis? Can depositors anticipate which banks will fail? Understanding the behavior of depositors in financial crises is key to evaluating the policy measures, such as deposit insurance, designed to prevent them. But this is difficult in modern settings. The fact that bank runs are rare and deposit insurance universal implies that it is rare to be able to observe how depositors would behave in absence of the policy. Hence, as empiricists, we are lacking the counterfactual of depositor behavior during a run that is undistorted by the policy. In this blog post and the staff report on which it is based, we go back in history and study a bank run that took place in Germany in 1931 in the absence of deposit insurance for insight.

Posted at 7:00 am in Banks, Financial Institutions, Financial Intermediation, Panic, Systemic Risk | Permalink

October 18, 2021

Were Banks Exposed to Sell‑offs by Open‑End Funds during the Covid Crisis?

Should open-end mutual funds experience redemption pressures, they may be forced to sell assets, thus contributing to asset price dislocations that in turn could be felt by other entities holding similar assets. This fire-sale externality is a key rationale behind proposed and implemented regulatory actions. In this post, I quantify the spillover risks from fire sales, and present some preliminary results on the potential exposure of U.S. banking institutions to asset fire sales from open-end funds.

June 22, 2021

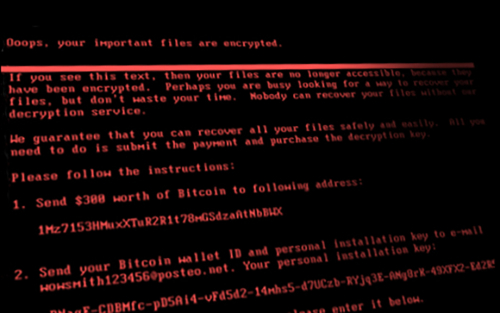

Cyberattacks and Supply Chain Disruptions

Cybercrime is one of the most pressing concerns for firms. Hackers perpetrate frequent but isolated ransomware attacks mostly for financial gains, while state-actors use more sophisticated techniques to obtain strategic information such as intellectual property and, in more extreme cases, to disrupt the operations of critical organizations. Thus, they can damage firms’ productive capacity, thereby potentially affecting their customers and suppliers. In this post, which is based on a related Staff Report, we study a particularly severe cyberattack that inadvertently spread beyond its original target and disrupted the operations of several firms around the world. More recent examples of disruptive cyberattacks include the ransomware attacks on Colonial Pipeline, the largest pipeline system for refined oil products in the U.S., and JBS, a global beef processing company. In both cases, operations halted for several days, causing protracted supply chain bottlenecks.

February 24, 2021

State‑of‑the‑Field Conference on Cyber Risk to Financial Stability

The Federal Reserve Bank of New York partnered with Columbia University’s School of International and Public Affairs (SIPA) for the second annual State-of-the-Field Conference on Cyber Risk to Financial Stability on December 14-15, 2020. Hosted virtually due to the COVID-19 pandemic, the conference took place amidst the unfolding news of a cyberattack against a major cybersecurity vendor and software vendor, underscoring vulnerabilities from cyber risk.

February 11, 2021

Did Subsidies to Too‑Big‑To‑Fail Banks Increase during the COVID‑19 Pandemic?

New Liberty Street Economics analysis by Asani Sarkar investigates whether the COVID-19 pandemic has led to an increase in implicit TBTF subsidies for large firms.

Posted at 7:00 am in Banks, Financial Institutions, Pandemic, Systemic Risk | Permalink | Comments (2)

September 30, 2020

Did Too‑Big‑To‑Fail Reforms Work Globally?

Once a bank grows beyond a certain size or becomes too complex and interconnected, investors often perceive that it is “too big to fail” (TBTF), meaning that if the bank were to fail, the government would likely bail it out. Following the global financial crisis (GFC) of 2008, the G20 countries agreed on a set of reforms to eliminate the perception of TBTF, as part of a broader package to enhance financial stability. In June 2020, the Financial Stability Board (FSB; a 68-member international advisory body set up in 2009) published the results of a year-long evaluation of the effectiveness of TBTF reforms. In this post, I discuss the main conclusions of the report—in particular, the finding that implicit funding subsidies to global banks have decreased since the implementation of reforms but remain at levels comparable to the pre-crisis period.

May 21, 2020

What Do Financial Conditions Tell Us about Risks to GDP Growth?

Boyarchenko and coauthors estimate the risks around the modal forecast of GDP growth as a function of financial conditions.

May 19, 2020

The Primary Dealer Credit Facility

On March 17, 2020, the Federal Reserve announced that it would re-establish the Primary Dealer Credit Facility (PDCF) to allow primary dealers to support smooth market functioning and facilitate the availability of credit to businesses and households. The PDCF started offering overnight and term funding with maturities of up to ninety days on March 20. It will be in place for at least six months and may be extended as conditions warrant. In this post, we provide an overview of the PDCF and its usage to date.

Posted at 7:00 am in Bank Capital, Banks, Central Bank, COVID-19 Facilities, Credit, Federal Reserve, Liquidity, Monetary Policy, Pandemic, Systemic Risk | Permalink

April 8, 2020

How Does Supervision Affect Bank Performance during Downturns?

New research finds that there is a cyclical nature to the benefits of bank supervisory attention: in normal times, the benefits are smaller, but during downturns the more closely supervised banks exhibit better loan performance and lower earnings volatility.

Posted at 7:00 am in Bank Capital, Banks, Crisis, Federal Reserve, Financial Institutions, Recession, Systemic Risk | Permalink

February 24, 2020

Understanding Heterogeneous Agent New Keynesian Models: Insights from a PRANK

To shed light on the macroeconomic consequences of heterogeneity, Acharya and Dogra develop a stylized HANK model that contains key features present in more complicated HANK models.

Posted at 7:00 am in Central Bank, Credit, Federal Reserve, Financial Institutions, Fiscal Policy, Inequality, Macroeconomics, Monetary Policy, Recession, Systemic Risk | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics