Businesses experienced substantial cost pressures in 2025 as the cost of insurance and utilities rose sharply, while an increase in tariffs contributed to rising goods and materials costs. This post examines how firms in the New York-Northern New Jersey region adjusted their prices in response to these cost pressures and describes their expectations for future price increases and inflation. Survey results show an acceleration in firms’ price increases in 2025, with an especially sharp increase in the manufacturing sector. While both cost and price increases intensified last year, our surveys reveal that these do not contribute to firms believing that inflation will be on the rise in the short or longer term. In fact, firms’ inflation expectations have moderated compared to what was expected a year ago. Firms now anticipate inflation of 3 percent in the year ahead, lower than what was expected last year at this time. Importantly, like last year, longer-term inflation expectations also remain well anchored.

Price Increases Picked Up Last Year

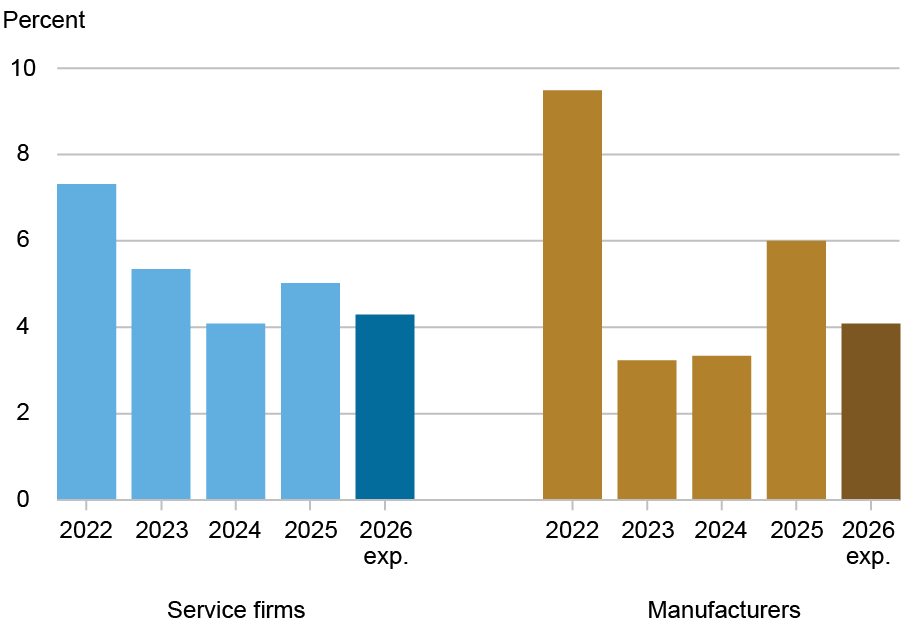

According to our surveys, on the heels of sharp price hikes during the post-pandemic inflationary period, firms’ price increases had moderated in 2023 and 2024, but the pace picked back up again in 2025. Service sector firms increased their prices by an average of 5.0 percent in 2025, up from 4.1 percent in 2024, as shown in the chart below, which plots average price increases among firms in our surveys. The increase in prices was even more pronounced in the manufacturing sector, where firms raised prices by 6.0 percent in 2025 on average, nearly double the 3.3 percent pace reported in 2024.

Price Increases Picked Up in 2025, But Are Expected to Moderate

Note: These averages represent a trimmed mean; the highest 5 percent and the lowest 5 percent of responses are excluded.

These realized price increases in 2025 were fairly close to what was expected by service firms when they were surveyed last year, but were somewhat higher than the 5.4 percent increase manufacturing firms had anticipated. Looking ahead to 2026, firms expect price increases to moderate somewhat, but to remain elevated at just over 4 percent. This expected pace of price increases represents a deceleration from 2025 levels but remains above price increases reported in 2024 when inflationary pressures were subsiding.

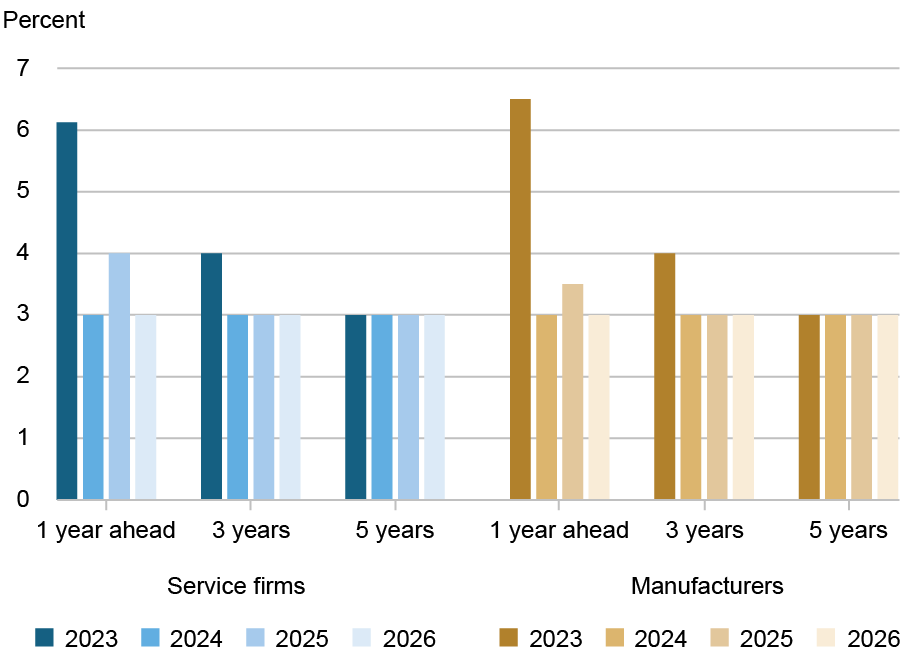

Year-Ahead Inflation Expectations Move Down

Despite a year of elevated cost and price increases, firms’ median year-ahead inflation expectations fell to 3.0 percent, returning to where expectations were in 2024, as shown in the chart below. This represents a moderation compared to last year, when service firms expected 4.0 percent inflation for 2025 and manufacturers expected 3.5 percent. These figures are consistent with the year-ahead inflation expectations of consumers, which also fell to around 3 percent in early 2026. This stability in inflation expectations could be partially attributed to firms interpreting tariff-induced cost increases in 2025 as a temporary, one-time adjustment rather than the beginning of sustained inflationary pressure. Firms may also be extrapolating from their own planned pricing behavior and expected future costs, as firms expect to raise prices and experience cost growth at a slower pace in 2026 than in 2025.

Firms’ Inflation Expectations Are Well Anchored

Note: Figures represent medians.

Longer-Term Inflation Expectations Remain Anchored

Like the expectations of households, firms’ longer-term inflation expectations at three- and five-year horizons remain anchored at 3.0 percent, meaning shorter-term expectations have come back down to the same level as longer-term expectations. This anchoring of inflation expectations is important. Firms’ expectations about future inflation can shape how they set wages and prices—in other words, expectations about the path of future inflation can affect how current inflation will evolve. If businesses and consumers expect inflation to be high in the future because it is elevated today, they may change their behavior accordingly, which can make inflation even more persistent. All in all, the fact that year-ahead expectations have moved lower and longer-term expectations have held steady despite the significant cost and price pressures firms faced last year suggests that firms’ behavior is less likely to induce more persistent inflation pressures going forward.

Jaison R. Abel is head of Microeconomics in the Federal Reserve Bank of New York’s Research and Statistics Group.

Richard Deitz is an economic policy advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Nick Montalbano is a data analytics specialist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Jaison R. Abel, Richard Deitz, and Nick Montalbano, “Firms’ Inflation Expectations Return to 2024 Levels,” Federal Reserve Bank of New York Liberty Street Economics, March 4, 2026, https://doi.org/10.59576/lse.20260304c

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics