9 posts from "June 2021"

June 30, 2021

Hold the Check: Overdrafts, Fee Caps, and Financial Inclusion

The 25 percent of low-income Americans without a checking account operate in a separate but unequal financial world. Instead of paying for things with cheap, convenient debit cards and checks, they get by with “fringe” payment providers like check cashers, money transfer, and other alternatives. Costly overdrafts rank high among reasons why households “bounce out” of the banking system and some observers have advocated capping overdraft fees to promote inclusion. Our recent paper finds unintended (if predictable) effects of overdraft fee caps. Studying a case where fee caps were selectively relaxed for some banks, we find higher fees at the unbound banks, but also increased overdraft credit supply, lower bounced check rates (potentially the costliest overdraft), and more low-income households with checking accounts. That said, we recognize that overdraft credit is expensive, sometimes more than even payday loans. In lieu of caps, we see increased overdraft credit competition and transparency as alternative paths to cheaper deposit accounts and increased inclusion.

Banking the Unbanked: The Past and Future of the Free Checking Account

About one in twenty American households are unbanked (meaning they do not have a demand deposit or checking account) and many more are underbanked (meaning they do not have the range of bank-provided financial services they need). Unbanked and underbanked households are more likely to be lower-income households and households of color. Inadequate access to financial services pushes the unbanked to use high-cost alternatives for their transactional needs and can also hinder access to credit when households need it. That, in turn, can have adverse effects on the financial health, educational opportunities, and welfare of unbanked households, thereby aggravating economic inequality. Why is access to financial services so uneven? The roots to part of this problem are historical, and in this post we will look back four decades to changes in regulation, shifts in the ownership structure of retail financial services, and the decline of free/low-cost checking accounts in the United States to search out a few of the contributory factors.

Posted at 7:00 am in Banks, Credit, Financial Intermediation, Financial Markets, Inequality | Permalink

June 23, 2021

Central Banks and Digital Currencies

Recent developments in payments technology raise important questions about the role of central banks either in providing a digital currency themselves or in supporting the development of digital currencies by private actors, as some authors of this post have discussed in a recent IMF blog post. In this post, we consider two ways a central bank could choose to become involved with digital currencies and discuss some implications of these potential choices.

Posted at 7:00 am | Permalink

June 22, 2021

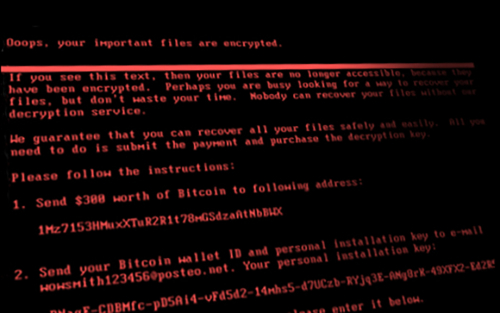

Cyberattacks and Supply Chain Disruptions

Cybercrime is one of the most pressing concerns for firms. Hackers perpetrate frequent but isolated ransomware attacks mostly for financial gains, while state-actors use more sophisticated techniques to obtain strategic information such as intellectual property and, in more extreme cases, to disrupt the operations of critical organizations. Thus, they can damage firms’ productive capacity, thereby potentially affecting their customers and suppliers. In this post, which is based on a related Staff Report, we study a particularly severe cyberattack that inadvertently spread beyond its original target and disrupted the operations of several firms around the world. More recent examples of disruptive cyberattacks include the ransomware attacks on Colonial Pipeline, the largest pipeline system for refined oil products in the U.S., and JBS, a global beef processing company. In both cases, operations halted for several days, causing protracted supply chain bottlenecks.

June 21, 2021

What Happened to the U.S. Deficit with China during the U.S.‑China Trade Conflict?

The United States’ trade deficit with China narrowed significantly following the imposition of additional tariffs on imports from China in multiple waves beginning in 2018—or at least it did based on U.S. trade data. Chinese data tell a much different story, with the bilateral deficit rising nearly to historical highs at the end of 2020. What’s going on here? We find that (as also discussed in a related note) much of the decline in the deficit recorded in U.S. data was driven by successful efforts to evade U.S. tariffs, with an estimated $10 billion loss in tariff revenues in 2020.

Posted at 2:00 pm | Permalink

Has Market Power of U.S. Firms Increased?

A number of studies have documented that market concentration among U.S. firms has increased over the last decades, as large firms have grown more dominant. In a new study, we examine whether this rising domestic concentration means that large U.S. firms have more market power in the manufacturing sector. Our research argues that increasing foreign competition over the last few decades has in fact reduced U.S. firms’ market power in manufacturing.

Posted at 7:00 am | Permalink

June 18, 2021

The Future of Remote Work in the Region

The coronavirus pandemic abruptly changed the way we work, in meaningful and potentially lasting ways. While working from home represented a small share of work before the pandemic, such arrangements became unexpectedly widespread once the pandemic struck. With the pandemic now being brought under control and conditions improving, workers have begun to return to the office. But just how much remote work will persist in the new normal? The New York Fed’s June regional business surveys asked firms about the extent of remote working before, during, and after the pandemic. Results indicate that before the pandemic, the average firm in the region conducted just a small share of its work remotely, a figure that currently stands at around a third among service firms but well below 10 percent among manufacturers. Once the pandemic is fully behind us, service firms expect double the amount of remote work than before the pandemic, though that figure is less than the share being done currently, while manufacturers expect the amount of remote work to return to where it was before the pandemic.

The New York Fed DSGE Model Forecast—June 2021

This post presents an update of the economic forecasts generated by the Federal Reserve Bank of New York’s dynamic stochastic general equilibrium (DSGE) model. We describe very briefly our forecast and its change since March 2021. As usual, we wish to remind our readers that the DSGE model forecast is not an official New York Fed forecast, but only an input to the Research staff’s overall forecasting process. For more information about the model and variables discussed here, see our DSGE model Q & A.

June 2, 2021

Sophisticated and Unsophisticated Runs

In March 2020, U.S. prime money market funds (MMFs) suffered heavy outflows following the liquidity shock triggered by the COVID-19 crisis. In a previous post, we characterized the run on the prime MMF industry as a whole and the role of the liquidity facility established by the Federal Reserve (the Money Market Mutual Fund Liquidity Facility) in stemming the run. In this post, based on a recent Staff Report, we contrast the behaviors of retail and institutional investors during the run and explain the different reasons behind the run.

Posted at 7:00 am in Financial Intermediation | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics