86 posts on "Regulation"

July 17, 2026

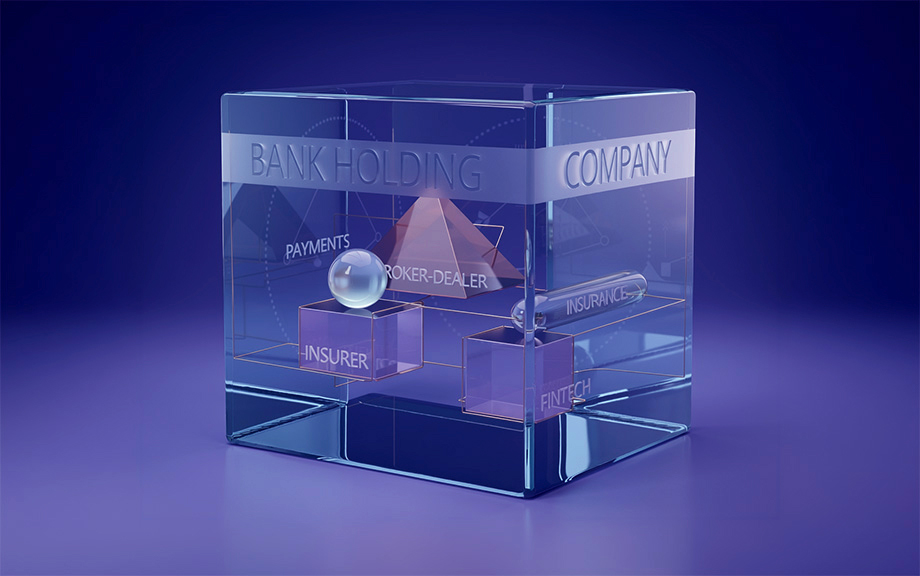

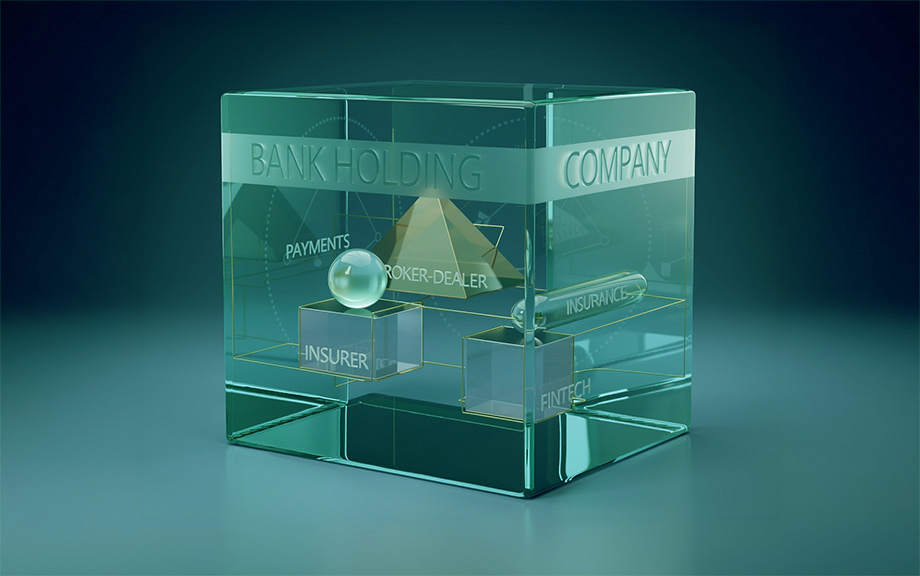

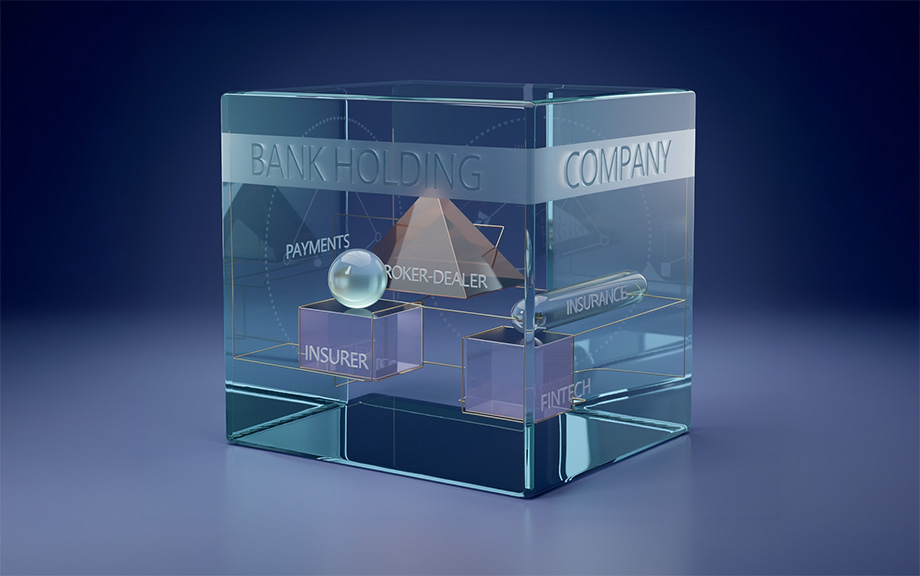

Nonbank Subsidiaries and the Hidden Fragility of Internal Capital Markets Reallocation

This post concludes a three-part series on how bank regulation interacts with the organizational structure of banking firms. The first post documented the equity-rich nonbank subsidiaries inside bank holding companies (BHCs); the second post showed that BHCs met Basel III by reallocating capital internally, moving equity from nonbank affiliates to bank subsidiaries rather than raising new external capital. Here we ask what that reallocation meant for financial stability. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 16, 2026

How Basel III Changes Where Capital Sits: Nonbank Subsidiaries as Equity Reservoirs

This post is the second in a three-part series on how bank regulation interacts with the organizational structure of banking firms. The first post documented that nonbank subsidiaries inside bank holding companies (BHCs) are large, equity-rich “reservoirs,” and that bank-level capital diverged sharply from consolidated capital after Basel III took effect in 2015. This post asks why, and traces the answer through the internal plumbing of the holding company. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 15, 2026

Capitalizing on Nonbanks: Regulatory Arbitrage Within Bank Holding Companies

This post is the first in a three-part series on how bank regulation interacts with the organizational structure of banking firms. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

December 15, 2025

Designing Bank Regulation with Accounting Discretion

Why does the banking industry remain prone to large and costly disruptions despite being so heavily regulated? Is there a need for more regulation, less regulation, or simply different regulation? Our recent Staff Report combines insights from academic research in economics, finance, and accounting to provide a deeper understanding of the challenges involved in designing and implementing bank regulation, as well as opportunities for future exploration. This post focuses on the regulation of bank capital, but the ideas are applicable more broadly.

February 14, 2025

How Censorship Resistant Are Decentralized Systems?

Public permissionless blockchains are designed to be censorship resistant, meaning access to the blockchain is unhampered. In practice, different blockchain ecosystem actors (such as users, builders, or proposers) can influence the degree to which a blockchain is resistant to censorship. In a recent Staff Report, we examine how sanctions imposed by the Office of Foreign Assets Control (OFAC) on Tornado Cash, a set of noncustodial cryptocurrency smart contracts on Ethereum, affected Tornado Cash and the broader Ethereum network. In this post, we summarize findings regarding sanction cooperation at the settlement layer by “block proposers”—a set of settlement actors specifically responsible for selecting new blocks to add to the blockchain.

April 15, 2024

Can I Speak to Your Supervisor? The Importance of Bank Supervision

In March of 2023, the U.S. banking industry experienced a period of significant turmoil involving runs on several banks and heightened concerns about contagion. While many factors contributed to these events—including poor risk management, lapses in firm governance, outsized exposures to interest rate risk, and unrecognized vulnerabilities from interconnected depositor bases, the role of bank supervisors came under particular scrutiny. Questions were raised about why supervisors did not intervene more forcefully before problems arose. In response, supervisory agencies, including the Federal Reserve and Federal Deposit Insurance Corporation, commissioned reviews that examined how supervisors’ actions might have contributed to, or mitigated, the failures. The reviews highlighted the important role that bank supervisors can play in fostering a stable banking system. In this post, we draw on our recent paper providing a critical review and summary of the empirical and theoretical literature on bank supervision to highlight what that literature tells us about the impact of supervision on supervised banks, on the banking industry and on the broader economy.

Posted at 7:00 am in Bank Capital, Banks, Federal Reserve, Financial Institutions, Regulation | Permalink

April 12, 2023

Does Corporate Hedging of Foreign Exchange Risk Affect Real Economic Activity?

Foreign exchange derivatives (FXD) are a key tool for firms to hedge FX risk and are particularly important for exporting or importing firms in emerging markets. This is because FX volatility can be quite high—up to 120 percent per annum for some emerging market currencies during stress episodes—yet the vast majority of international trades, almost 90 percent, are invoiced in U.S. dollars (USD) or euros (EUR). When such hedging instruments are in short supply, what happens to firms’ real economic activities? In this post, based on my related Staff Report, I use hand-collected FXD contract-level data and exploit a quasi-natural experiment in South Korea to measure the real effects of hedging using FXD.

February 27, 2023

Does the CRA Increase Household Access to Credit?

Congress passed the Community Reinvestment Act (CRA) in 1977 to encourage banks to meet the needs of borrowers in the areas in which they operate. In particular, the Act is focused on credit access to low- and moderate-income communities that had historically been subject to discriminatory practices like redlining.

Posted at 7:00 am in Banks, Credit, Equitable Growth, Inequality, Regulation | Permalink | Comments (2)

February 3, 2023

How the LIBOR Transition Affects the Supply of Revolving Credit

In the United States, most commercial and industrial (C&I) lending takes the form of revolving lines of credit, known as revolvers or credit lines. For decades, like other U.S. C&I loans, credit lines were typically indexed to the London Interbank Offered Rate (LIBOR). However, since 2022, the U.S. and other developed-market economies have transitioned from credit-sensitive reference rates such as LIBOR to new risk-free rates, including the Secured Overnight Financing Rate (SOFR). This post, based on a recent New York Fed Staff Report, explores how the provision of revolving credit is likely to change as a result of the transition to a new reference rate.

Posted at 7:00 am in Banks, Credit, Financial Institutions, Financial Intermediation, Regulation | Permalink | Comments (2)

January 9, 2023

Bank Profits and Shareholder Payouts: The Repurchases Cycle

During the height of the COVID-19 pandemic, the Federal Reserve placed restrictions on large banks’ dividends and share repurchases. These restrictions were intended to enhance banks’ resiliency by bolstering their capital in light of the very uncertain economic environment and concerns that banks might face very large losses should bad-case scenarios come to pass. When it became clear that the outlook had improved and that the losses banks experienced were unlikely to threaten their stability, the Federal Reserve removed these restrictions. In this post, we look at what happened to large banks’ dividends and share repurchases during and after the pandemic-era restrictions, tracking these shareholder payouts relative to bank profits to understand how these payments impacted large banks’ capital during this period.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics