9 posts from "November 2016"

November 30, 2016

Just Released: Subprime Auto Debt Grows Despite Rising Delinquencies

The latest Quarterly Report on Household Debt and Credit from the New York Fed’s Center for Microeconomic Data showed a small increase in overall debt in the third quarter of 2016, bolstered by gains in non-housing debt. Mortgage balances continue to grow at a sluggish pace since the recession while auto loan balances are growing steadily.

November 28, 2016

At the N.Y. Fed: Convening on the Evolution of Work

Nora Fitzpatrick, Laura Pilossoph, Anika Pratt, and Aysegul Sahin The Federal Reserve Bank of New York recently hosted “The Evolution of Work,” a conference that brought together thought leaders from academia, government, industry, labor, and the nonprofit sector to explore how the nature of work is evolving, including the expanding role of technology, shifts in […]

November 21, 2016

The FRBNY DSGE Model Forecast—November 2016

This post presents the latest update of the economic forecasts generated by the Federal Reserve Bank of New York’s (FRBNY) dynamic stochastic general equilibrium (DSGE) model.

Posted at 7:00 am in DSGE, Expectations, Forecasting, Macroeconomics, Monetary Policy | Permalink | Comments (2)

November 18, 2016

Just Released: Press Briefing on the Survey of Consumer Expectations

The New York Fed’s Survey of Consumer Expectations (SCE) collects information on household heads’ economic expectations and behavior. In particular, the survey covers respondents’ views on how inflation, spending, credit access, and the housing and labor markets will evolve over time. The SCE yields important insights that inform our monetary policy decisions. This morning, President Dudley joined Bank economists to brief the press on the design of the SCE and the latest releases of survey results. President Dudley introduced the briefing by speaking about the benefits of measuring consumers’ expectations.

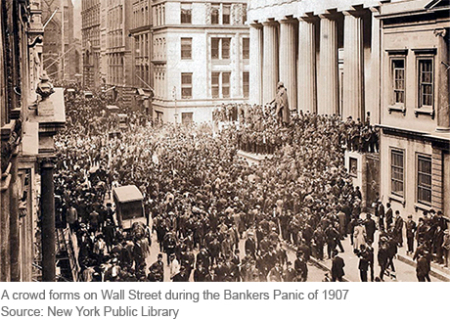

The Final Crisis Chronicle: The Panic of 1907 and the Birth of the Fed

The panic of 1907 was among the most severe we’ve covered in our series and also the most transformative, as it led to the creation of the Federal Reserve System. Also known as the “Knickerbocker Crisis,” the panic of 1907 shares features with the 2007-08 crisis, including “shadow banks” in the form high-flying, less-regulated trusts operating beyond the safety net of the time, and a pivotal “Lehman moment” when Knickerbocker Trust, the second-largest trust in the country, was allowed to fail after J.P. Morgan refused to save it.

Posted at 7:00 am in Crisis, Economic History, Financial Institutions, Financial Markets, Regulation, Treasury | Permalink

November 16, 2016

Escaping Unemployment Traps

Economic activity has remained subdued following the Great Recession. One interpretation of the listless recovery is that recessions inflict permanent damage on an economy’s productive capacity. For example, extended periods of high unemployment can lead to skill losses among workers, reducing human capital and lowering future output. This notion that temporary recessions have long-lasting consequences is often termed hysteresis. Another explanation for sluggish growth is the influential secular stagnation hypothesis, which attributes slow growth to long-term changes in the economy’s underlying structure. While these explanations are observationally similar, they have very different policy implications. In particular, if structural factors are responsible for slow growth, then there might be little monetary policy can do to reverse this trend. If instead hysteresis is to blame, then monetary policy may be able to reverse slowdowns in potential output, or even prevent them from occurring in the first place.

November 14, 2016

Inflation and Japan’s Ever‑Tightening Labor Market

Japan offers a preview of future U.S. demographic trends, having already seen a large increase in the population over 65.

Posted at 7:00 am in International Economics, Labor Market, Macroeconomics, Unemployment | Permalink | Comments (2)

November 9, 2016

Performance Bonds for Bankers: Taking Aim at Misconduct

Given the long list of problems that have emerged in banks over the past several years, it is time to consider performance bonds for bankers. Performance bonds are used to ensure that appropriate actions are taken by a party when monitoring or enforcement is expensive. A simple example is a security deposit on an apartment rental. The risk of losing the deposit motivates renters to take care of the apartment, relieving the landlord of the need to monitor the premises. Although not quite as simple as a security deposit, performance bonds for bankers could provide more incentive for bankers to take better care of our financial system.

Posted at 7:00 am in Corporate Finance, Expectations, Financial Markets, Regulation | Permalink | Comments (2)

November 7, 2016

What’s Driving the Recent Slump in U.S. Imports?

The growth in U.S. imports of goods has been stubbornly low since the second quarter of 2015, with an average annual growth rate of 0.7 percent.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics