187 posts on "Banks"

July 17, 2026

Nonbank Subsidiaries and the Hidden Fragility of Internal Capital Markets Reallocation

This post concludes a three-part series on how bank regulation interacts with the organizational structure of banking firms. The first post documented the equity-rich nonbank subsidiaries inside bank holding companies (BHCs); the second post showed that BHCs met Basel III by reallocating capital internally, moving equity from nonbank affiliates to bank subsidiaries rather than raising new external capital. Here we ask what that reallocation meant for financial stability. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 16, 2026

How Basel III Changes Where Capital Sits: Nonbank Subsidiaries as Equity Reservoirs

This post is the second in a three-part series on how bank regulation interacts with the organizational structure of banking firms. The first post documented that nonbank subsidiaries inside bank holding companies (BHCs) are large, equity-rich “reservoirs,” and that bank-level capital diverged sharply from consolidated capital after Basel III took effect in 2015. This post asks why, and traces the answer through the internal plumbing of the holding company. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 15, 2026

Capitalizing on Nonbanks: Regulatory Arbitrage Within Bank Holding Companies

This post is the first in a three-part series on how bank regulation interacts with the organizational structure of banking firms. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 7, 2026

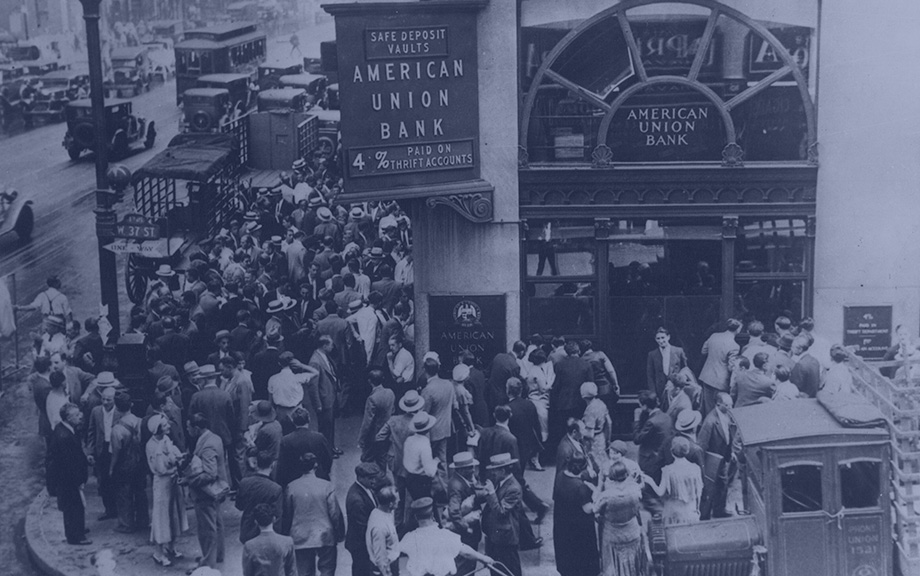

What Do Over 3,000 Bank Runs Teach Us About Banking Crises?

Runs on financial institutions are one of the salient markers of financial crises. But the role of runs in crises is a topic of longstanding debate. Runs can be seen as the key turning point, whereby even small shocks can generate severe crises with widespread bank failures. Another view is that runs are mainly a symptom of deeper rot in the financial system, exacerbating crises rather than being their primary cause. Understanding this debate has first order implications for how to think about financial crises and the appropriate policy responses. In this post, we use a new database of more than 3,000 bank runs (introduced in our companion post) to show that poor fundamentals are central to explaining both when runs occur and when they have severe economic effects. We argue that this evidence tempers the view that small shocks can have outsized real effects through self-fulfilling run dynamics.

Posted at 10:01 am in Artificial Intelligence (AI), Banks, Crisis, Liquidity | Permalink | Comments (1)

Using AI to Let History Speak About Bank Runs

Banking crises are commonly associated with bank runs and banking panics, yet our empirical understanding of bank runs is constrained by a lack of bank-level data. In a new paper, we use large language models (LLMs) to extract information on bank runs from millions of digitized historical newspaper pages, creating the most comprehensive database of bank runs in U.S. history. Every bank run episode that we identify is documented on a companion website where users can browse and examine individual episodes, and read the original newspaper articles. In this post, we describe how we built this dataset and discuss what its basic features reveal.

Posted at 10:00 am in Artificial Intelligence (AI), Banks, Crisis, Liquidity | Permalink | Comments (0)

May 8, 2026

Stress and Strain from NBFIs to Banks

Do the recent stresses in the NBFI space—notably the bankruptcies of Tricolor and First Brands, and the decision of Blue Owl Capital Corp II (OBDC II) to end its redemption program and return capital through a wind-down of the fund—create distress for banks? The general sentiment is that the recent stresses are unlikely to amount to systemic concerns, although it does not mean there might not be “some stress and strain” for banks and that policymakers are “watching carefully” for exposure across banks. In a series of previous posts, we showed that shocks to nonbank financial institutions (NBFIs) directly impact banks that have exposures to NBFIs. In this post, we show that bank stocks have been directly impacted by NBFIs yet again. In short, NBFI troubles do result in “stress and strain” for banks.

April 16, 2026

Bank Failures: The Roles of Solvency and Liquidity

Do banks fail because of runs or because they become insolvent? Answering this question is central to understanding financial crises and designing effective financial stability policies. Long-run historical evidence reveals that the root cause of bank failures is usually insolvency. The importance of bank runs is somewhat overstated. Runs matter, but in most cases they trigger or accelerate failure at already weak banks, rather than cause otherwise sound banks to fail.

April 2, 2026

Treasury Market Liquidity Since April 2025

In this post, we examine the evolution of U.S. Treasury market liquidity over the past year, which has witnessed myriad economic and political developments. Liquidity worsened markedly one year ago as volatility increased following the announcement of higher-than-expected tariffs. Liquidity quickly improved when the tariff increases were partially rolled back and then remained fairly stable thereafter (through the end of our sample in February 2026), including after the recent Supreme Court decision striking down the emergency tariffs and the subsequent announcement of new tariffs.

March 31, 2026

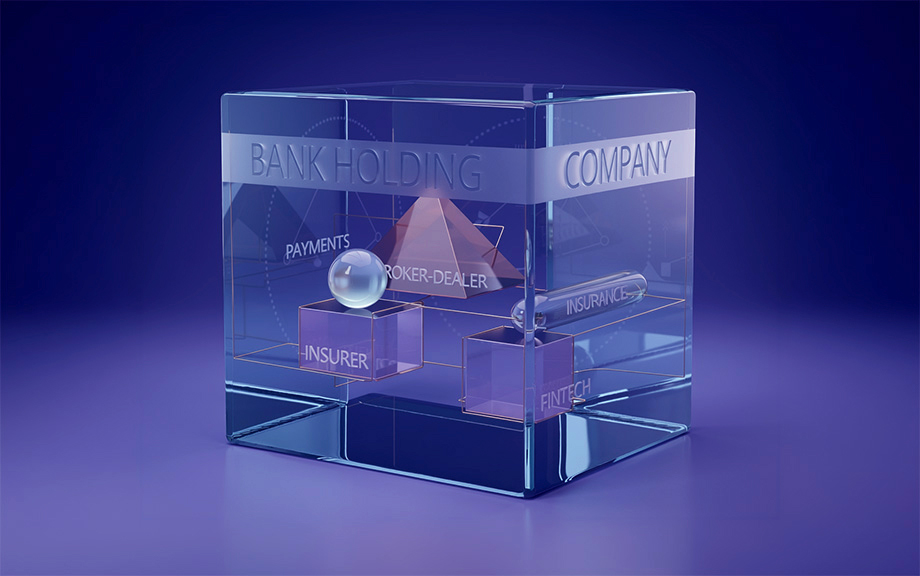

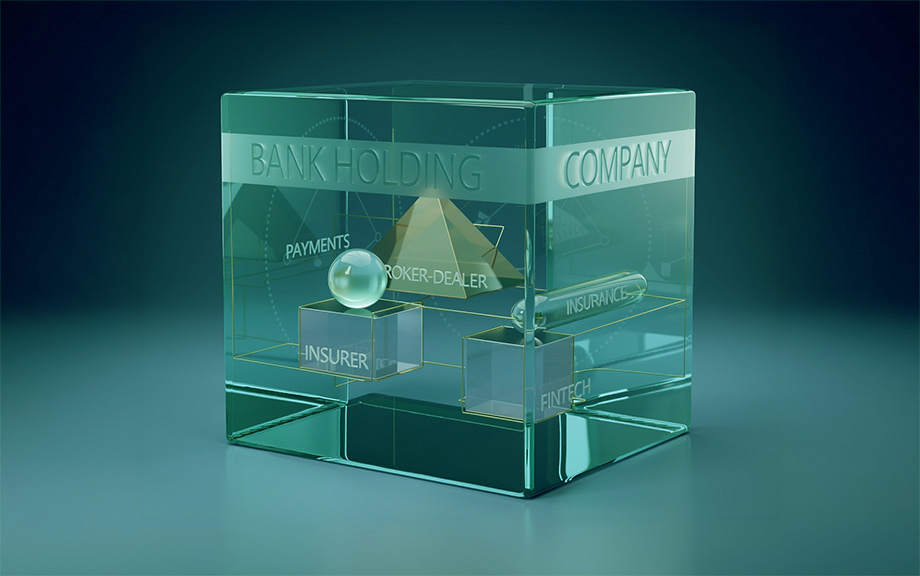

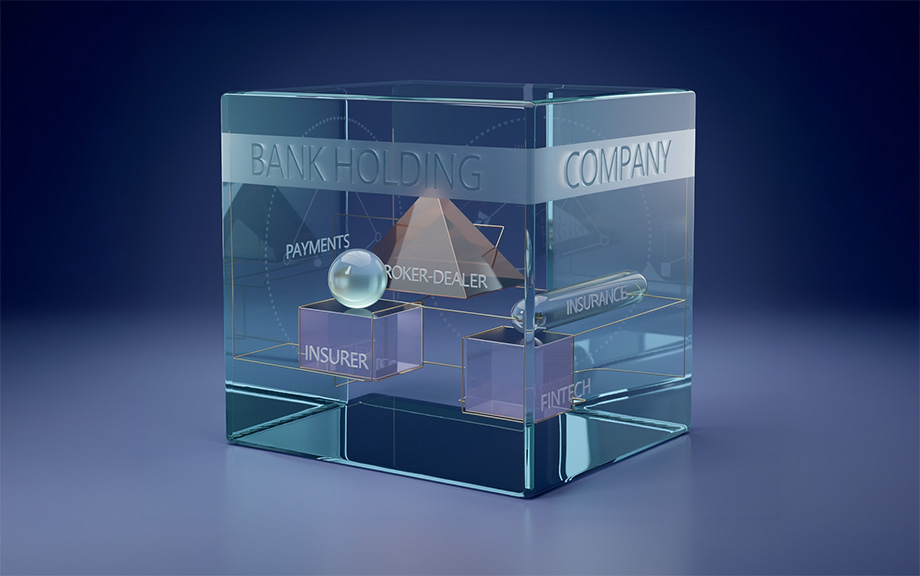

Behind the ATM: Exploring the Structure of Bank Holding Companies

Many modern banking organizations are highly complex. A “bank” is often a larger structure made up of distinct entities, each subject to different regulatory, supervisory, and reporting requirements. For researchers and policymakers, understanding how these institutions are structured and how they have evolved over time is essential. In this post, we illustrate what a modern financial holding company looks like in practice, document how banks’ organizational structures have changed over time, and explain why these details matter for conducting accurate analyses of the financial system.

December 22, 2025

A New Public Data Source: Call Reports from 1959 to 2025

Call Reports are regulatory filings in which commercial banks report their assets, liabilities, income, and other information. They are one of the most-used data sources in banking and finance. In this post, we describe a new dataset made available on the Federal Reserve Bank of New York’s website that contains time-consistent balance sheets and income statements for commercial banks in the United States from 1959 to 2025.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics