106 posts on "Liquidity"

July 7, 2026

What Do Over 3,000 Bank Runs Teach Us About Banking Crises?

Runs on financial institutions are one of the salient markers of financial crises. But the role of runs in crises is a topic of longstanding debate. Runs can be seen as the key turning point, whereby even small shocks can generate severe crises with widespread bank failures. Another view is that runs are mainly a symptom of deeper rot in the financial system, exacerbating crises rather than being their primary cause. Understanding this debate has first order implications for how to think about financial crises and the appropriate policy responses. In this post, we use a new database of more than 3,000 bank runs (introduced in our companion post) to show that poor fundamentals are central to explaining both when runs occur and when they have severe economic effects. We argue that this evidence tempers the view that small shocks can have outsized real effects through self-fulfilling run dynamics.

Posted at 10:01 am in Artificial Intelligence (AI), Banks, Crisis, Liquidity | Permalink | Comments (1)

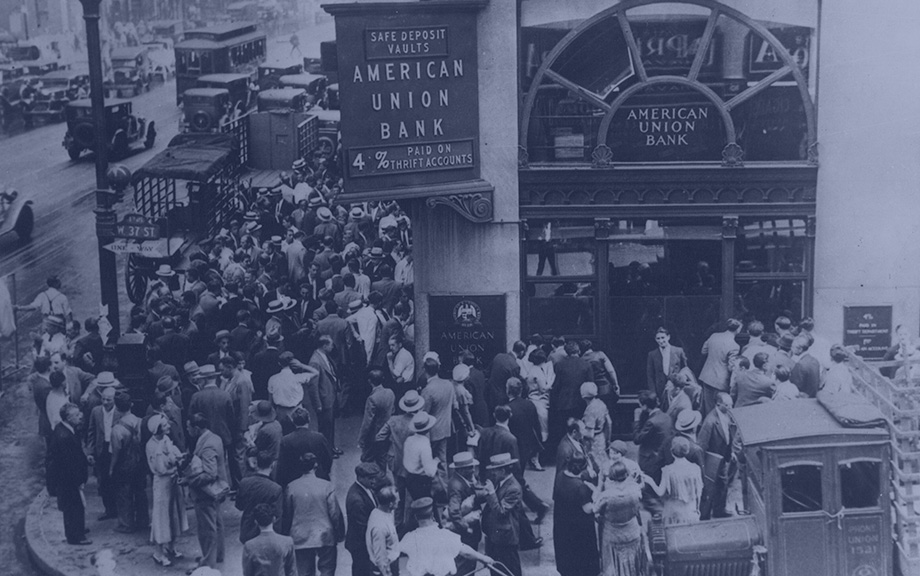

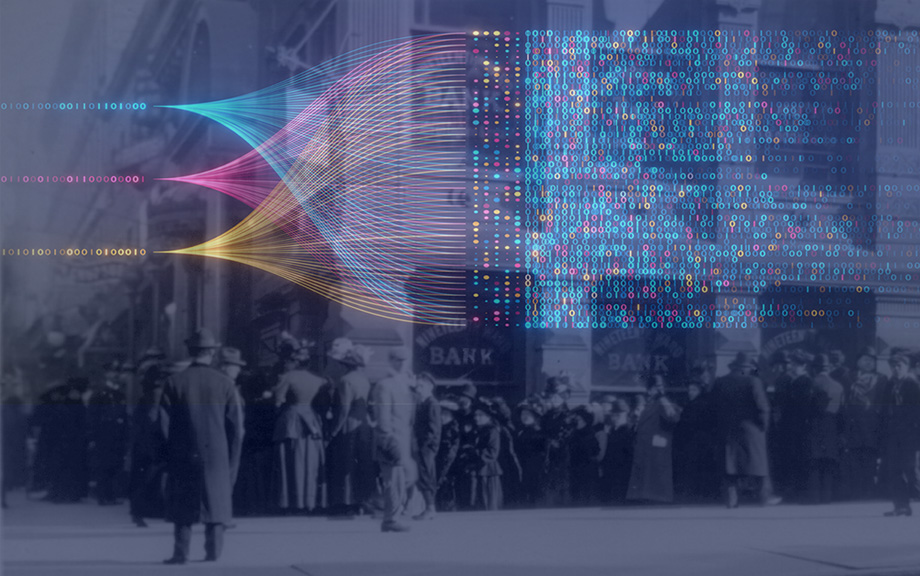

Using AI to Let History Speak About Bank Runs

Banking crises are commonly associated with bank runs and banking panics, yet our empirical understanding of bank runs is constrained by a lack of bank-level data. In a new paper, we use large language models (LLMs) to extract information on bank runs from millions of digitized historical newspaper pages, creating the most comprehensive database of bank runs in U.S. history. Every bank run episode that we identify is documented on a companion website where users can browse and examine individual episodes, and read the original newspaper articles. In this post, we describe how we built this dataset and discuss what its basic features reveal.

Posted at 10:00 am in Artificial Intelligence (AI), Banks, Crisis, Liquidity | Permalink | Comments (0)

July 1, 2026

The Disappearing Overnight Drift

In a 2021 Liberty Street Economics post, we documented the “overnight drift”—a large, persistent return to holding U.S. equity futures in the narrow window between 2:00 and 3:00 a.m. Eastern time, when European equity markets open. Five additional years of data later, that pattern appears to have faded: the 2:00–3:00 window that previously generated roughly 3.7 percent per annum has averaged close to zero since 2021. In this post, we revisit the overnight drift in light of the post-publication sample and use our inventory-risk framework to ask which of three observable channels—the dispersion of closing order imbalances, the level of return variance, or the risk-bearing capacity of liquidity providers—accounts for the change.

June 30, 2026

Liquidity Fades as Treasuries Age

More than $30 trillion U.S. Treasury debt is outstanding. Less than 4 percent of this amount, which is associated with the most recently issued Treasuries, called on-the-run securities, accounts for 65 percent of average daily trading volume. The remaining portion of the amount outstanding is accounted for by seasoned issues that have been replaced by newer benchmarks, which are referred to as off-the-run securities. In this post, we review the key results in our paper that uses transaction-level Treasury TRACE data to study how trading activity and liquidity evolve as securities move from on-the-run to off-the-run. We show three main patterns. First, off-the-run notes and bonds rely much more on dealer-to-customer intermediation than benchmark securities. Second, trading activity falls sharply and transaction costs increase as securities age. Third, securities that are cheapest to deliver into Treasury futures are an important exception: they trade more actively than other off-the-run bonds of similar age.

June 23, 2026

Synthetic Stablecoins and Financial Stability

On October 10, 2025, the announcement of a potential additional 100 percent tariff on Chinese goods drove risk-off moves across equities, Treasuries, credit spreads, and digital assets. Digital asset prices fell sharply, trading volumes surged, and liquidity vanished from key exchanges. In this post, we show how the price shock in digital assets was transmitted and amplified through a class of instruments called synthetic stablecoins—crypto assets whose structural design turned an external shock into a self-reinforcing deleveraging spiral within the crypto ecosystem.

April 16, 2026

Bank Failures: The Roles of Solvency and Liquidity

Do banks fail because of runs or because they become insolvent? Answering this question is central to understanding financial crises and designing effective financial stability policies. Long-run historical evidence reveals that the root cause of bank failures is usually insolvency. The importance of bank runs is somewhat overstated. Runs matter, but in most cases they trigger or accelerate failure at already weak banks, rather than cause otherwise sound banks to fail.

April 2, 2026

Treasury Market Liquidity Since April 2025

In this post, we examine the evolution of U.S. Treasury market liquidity over the past year, which has witnessed myriad economic and political developments. Liquidity worsened markedly one year ago as volatility increased following the announcement of higher-than-expected tariffs. Liquidity quickly improved when the tariff increases were partially rolled back and then remained fairly stable thereafter (through the end of our sample in February 2026), including after the recent Supreme Court decision striking down the emergency tariffs and the subsequent announcement of new tariffs.

November 12, 2025

How Has Treasury Market Liquidity Fared in 2025?

In 2025, the Federal Reserve has cut interest rates, trade policy has shifted abruptly, and economic policy uncertainty has increased. How have these developments affected the functioning of the key U.S. Treasury securities market? In this post, we return to some familiar metrics to assess the recent behavior of Treasury market liquidity. We find that liquidity briefly worsened around the April 2025 tariff announcements but that its relation to Treasury volatility has been similar to what it was in the past.

November 4, 2025

Banking System Vulnerability: 2025 Update

As in previous years, we provide in this post an update on the vulnerability of the U.S. banking system based on four analytical models that capture different aspects of this vulnerability. We use data through 2025:Q2 for our analysis, and also discuss how the vulnerability measures have changed since our last update one year ago.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Liquidity, Systemic Risk | Permalink

July 10, 2025

The Rise in Deposit Flightiness and Its Implications for Financial Stability

Deposits are often perceived as a stable funding source for banks. However, the risk of deposits rapidly leaving banks—known as deposit flightiness—has come under increased scrutiny following the failures of Silicon Valley Bank and other regional banks in March 2023. In a new paper, we show that deposit flightiness is not constant over time. In particular, flightiness reached historic highs after expansions in bank reserves associated with rounds of quantitative easing (QE). We argue that this elevated deposit flightiness may amplify the banking sector’s response to subsequent monetary policy rate hikes, highlighting a link between the Federal Reserve’s balance sheet and conventional monetary policy.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics