31 posts on "Nonbank (NBFI)"

July 17, 2026

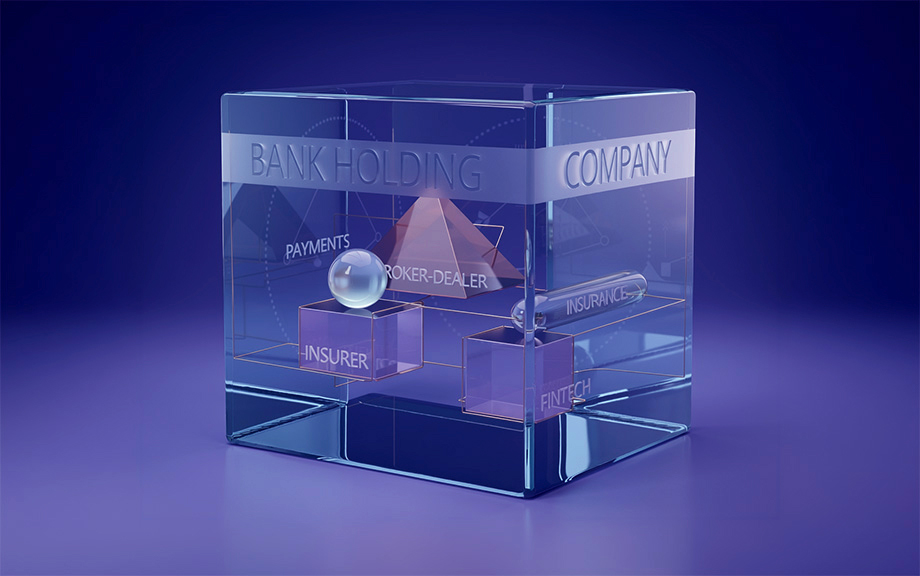

Nonbank Subsidiaries and the Hidden Fragility of Internal Capital Markets Reallocation

This post concludes a three-part series on how bank regulation interacts with the organizational structure of banking firms. The first post documented the equity-rich nonbank subsidiaries inside bank holding companies (BHCs); the second post showed that BHCs met Basel III by reallocating capital internally, moving equity from nonbank affiliates to bank subsidiaries rather than raising new external capital. Here we ask what that reallocation meant for financial stability. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 16, 2026

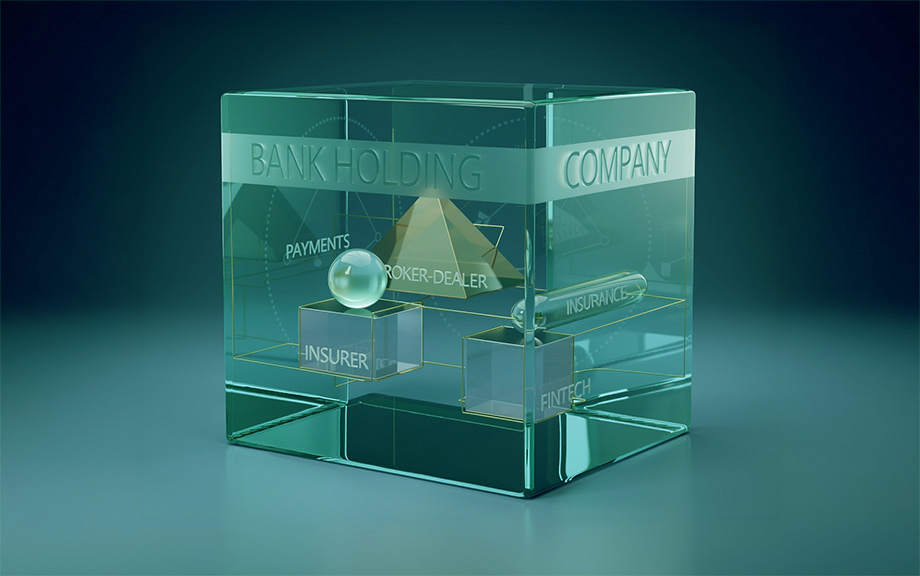

How Basel III Changes Where Capital Sits: Nonbank Subsidiaries as Equity Reservoirs

This post is the second in a three-part series on how bank regulation interacts with the organizational structure of banking firms. The first post documented that nonbank subsidiaries inside bank holding companies (BHCs) are large, equity-rich “reservoirs,” and that bank-level capital diverged sharply from consolidated capital after Basel III took effect in 2015. This post asks why, and traces the answer through the internal plumbing of the holding company. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 15, 2026

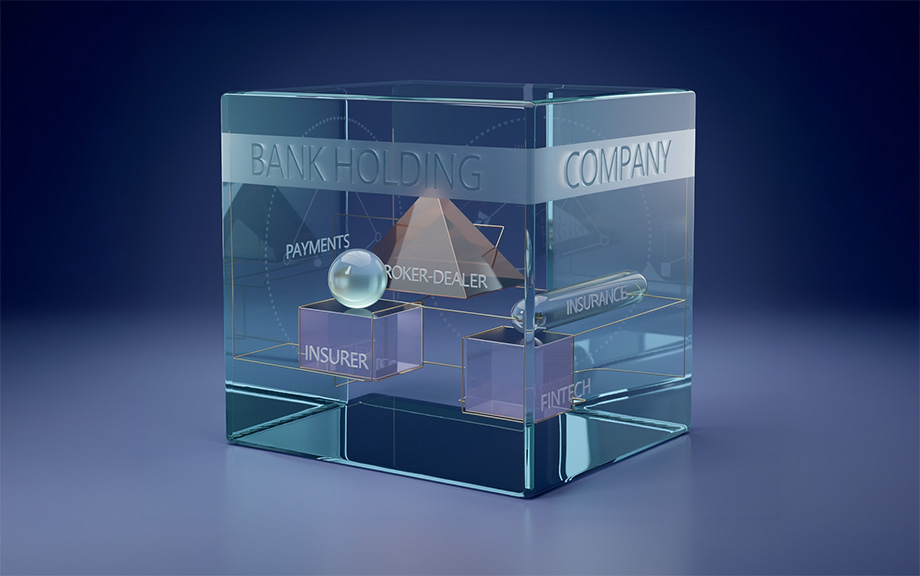

Capitalizing on Nonbanks: Regulatory Arbitrage Within Bank Holding Companies

This post is the first in a three-part series on how bank regulation interacts with the organizational structure of banking firms. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

May 8, 2026

Stress and Strain from NBFIs to Banks

Do the recent stresses in the NBFI space—notably the bankruptcies of Tricolor and First Brands, and the decision of Blue Owl Capital Corp II (OBDC II) to end its redemption program and return capital through a wind-down of the fund—create distress for banks? The general sentiment is that the recent stresses are unlikely to amount to systemic concerns, although it does not mean there might not be “some stress and strain” for banks and that policymakers are “watching carefully” for exposure across banks. In a series of previous posts, we showed that shocks to nonbank financial institutions (NBFIs) directly impact banks that have exposures to NBFIs. In this post, we show that bank stocks have been directly impacted by NBFIs yet again. In short, NBFI troubles do result in “stress and strain” for banks.

November 18, 2025

Banks Develop a Nonbank Footprint to Better Manage Liquidity Needs

In a previous post, we documented how, over the past five decades, the typical U.S. bank has evolved from an entity mainly focused on deposit taking and loan making to a more diversified conglomerate also incorporating a variety of nonbank activities. In this post, we show that an important driver of the evolution of this new organizational form is the desire of banks to efficiently manage liquidity needs.

U.S. Banks Have Developed a Significant Nonbank Footprint

In light of the rapid growth of nonbank financial institutions (NBFIs), many have argued that bank-led financial intermediation is on the decline, based on the traditional notion that banks operate to take in deposits and make loans. However, we argue that deposit-taking and loan-making have not accurately characterized U.S. banking operations in recent decades. Instead, as we propose in this post, absent regulatory restrictions, banks naturally expand their boundaries to include NBFI subsidiaries. A significant component of the growth of NBFIs has in fact taken place inside the boundaries of banking firms.

October 7, 2025

Dutch Treat: The Netherlands’ Exorbitant Privilege in the Eighteenth Century

The term “exorbitant privilege” emerged in the 1960s to describe the advantages derived by the U.S. economy from the dollar’s status as the de facto global reserve currency. In this post, we examine the exorbitant privilege that accrued to the Netherlands in the eighteenth century, when the Dutch guilder enjoyed global reserve currency status. We show how the private actions of financial institutions created and maintained this privilege, even in the absence of a central bank. While privilege benefited the Dutch financial system in many ways, it also laid the seeds of later financial crisis.

July 16, 2025

How Shadow Banking Reshapes the Optimal Mix of Regulation

Decisions that are privately optimal often impose externalities on other agents, giving rise to regulations aimed at implementing socially optimal outcomes. In the banking industry, regulations are particularly heavy, plausibly reflecting a view by regulators that the relevant externalities could culminate in financial crises and destabilize the broader economy. Over time, the toolkit for regulating banks and bank-like institutions has expanded, as has banks’ restructuring of activities into shadow banking to lessen the regulatory burden. This post, based on our recent Staff Report, explores the optimal mix of prudential tools for bank regulators in a wide range of environments.

July 14, 2025

Who Lends to Households and Firms?

The financial sector in the U.S. economy is deeply interconnected. In our previous post, we showed that incorporating information about this network of financial claims leads to a substantial reassessment of which financial sectors are ultimately financing the lending to the real sector as a whole (households plus nonfinancial firms). In this post, we delve deeper into the differences between the composition of lending to households and nonfinancial firms in terms of direct lending as well as the patterns of “adjusted lending” that we compute by accounting for the network of claims financial subsectors have on each other.

June 26, 2025

Financial Intermediaries and the Changing Risk Sensitivity of Global Liquidity Flows

Global risk conditions, along with monetary policy in major advanced economies, have historically been major drivers of cross-border capital flows and the global financial cycle. So what happens to these flows when risk sentiment changes? In this post, we examine how the sensitivity to risk of global financial flows changed following the global financial crisis (GFC). We find that while the risk sensitivity of cross-border bank loans (CBL) was lower following the GFC, that of international debt securities (IDS) remained the same as before the GFC. Moreover, the changes in risk sensitivities of these flows were related to balance sheet constraints of financial institutions that were intermediating these flows.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics