51 posts on "Bank Capital"

April 16, 2026

Bank Failures: The Roles of Solvency and Liquidity

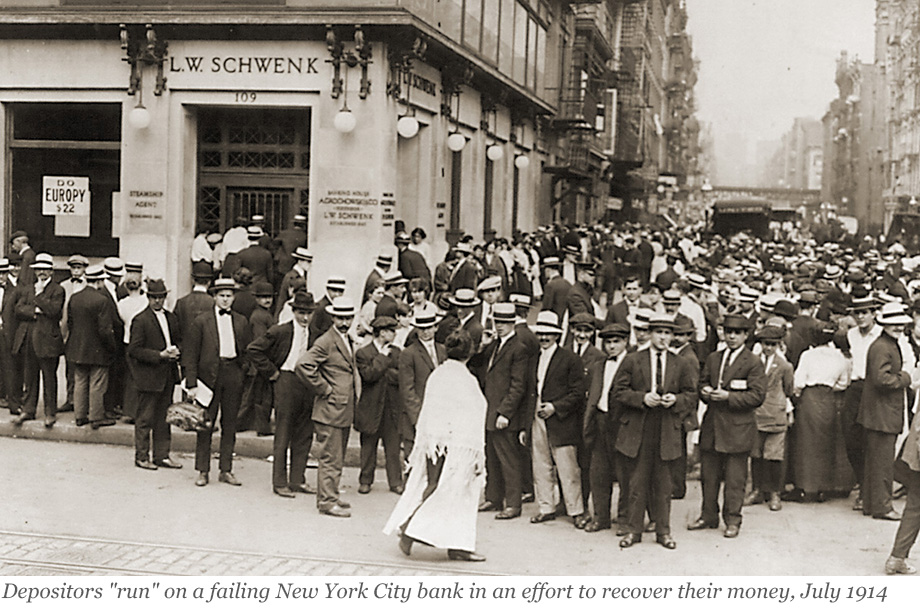

Do banks fail because of runs or because they become insolvent? Answering this question is central to understanding financial crises and designing effective financial stability policies. Long-run historical evidence reveals that the root cause of bank failures is usually insolvency. The importance of bank runs is somewhat overstated. Runs matter, but in most cases they trigger or accelerate failure at already weak banks, rather than cause otherwise sound banks to fail.

November 6, 2025

Economic Capital: A Better Measure of Bank Failure?

Bank failures and distress can be costly to the economy, causing losses to creditors and reducing the flow of credit and other financial intermediation services. Thus, there is significant value in being able to identify “at risk” banks in a timely and accurate way. In a previous post, we presented a new solvency metric, Economic Capital, and showed how solvency risks in the U.S. banking industry have evolved over time according to this measure. In this post, we continue to draw on our recent Staff Report to present analysis showing that Economic Capital identifies failing banks earlier and more accurately than more conventional solvency measures.

Posted at 7:00 am in Bank Capital | Permalink

November 4, 2025

Banking System Vulnerability: 2025 Update

As in previous years, we provide in this post an update on the vulnerability of the U.S. banking system based on four analytical models that capture different aspects of this vulnerability. We use data through 2025:Q2 for our analysis, and also discuss how the vulnerability measures have changed since our last update one year ago.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Liquidity, Systemic Risk | Permalink

September 22, 2025

Financial Intermediaries and Pressures on International Capital Flows

Global factors, like monetary policy rates from advanced economies and risk conditions, drive fluctuations in volumes of international capital flows and put pressure on exchange rates. The components of international capital flows that are described as global liquidity—consisting of cross-border bank lending and financing of issuance of international debt securities—have sensitivities to risk conditions that have evolved considerably over time. This risk sensitivity has been driven, in part, by the composition and business models of the financial institutions involved in funding. In this post, we ask whether these same features have led to changes in the pressures on currency values as risk conditions evolve. Using the Goldberg and Krogstrup (2023) Exchange Market Pressure (EMP) country indices, we show that the features of financial institutions in the source countries for international capital do influence how destination countries experience currency pressures when risk conditions change. Better shock-absorbing capacity in financial institutions moderates the pressures toward depreciation of currencies during adverse global risk events.

Posted at 7:00 am in Bank Capital, Exchange Rates, Financial Institutions, International Economics, Systemic Risk | Permalink

September 3, 2025

Economic Capital: A New Measure of Bank Solvency

Bank supervisors, industry analysts, and academic researchers rely on a range of metrics to track the health of both individual banks and the banking system as a whole. Many of these metrics focus on bank solvency—the likelihood that a bank will be able to repay its obligations and thus retain its funding and continue to supply services to consumers, businesses, and other financial institutions. We draw on our recent research to describe a new solvency metric that is more forward-looking, more timely, and more comprehensive in its assessment of solvency than many current measures.

Posted at 7:00 am in Bank Capital | Permalink

June 26, 2025

Financial Intermediaries and the Changing Risk Sensitivity of Global Liquidity Flows

Global risk conditions, along with monetary policy in major advanced economies, have historically been major drivers of cross-border capital flows and the global financial cycle. So what happens to these flows when risk sentiment changes? In this post, we examine how the sensitivity to risk of global financial flows changed following the global financial crisis (GFC). We find that while the risk sensitivity of cross-border bank loans (CBL) was lower following the GFC, that of international debt securities (IDS) remained the same as before the GFC. Moreover, the changes in risk sensitivities of these flows were related to balance sheet constraints of financial institutions that were intermediating these flows.

November 25, 2024

Why Do Banks Fail? Bank Runs Versus Solvency

Evidence from a 160-year-long panel of U.S. banks suggests that the ultimate cause of bank failures and banking crises is almost always a deterioration of bank fundamentals that leads to insolvency. As described in our previous post, bank failures—including those that involve bank runs—are typically preceded by a slow deterioration of bank fundamentals and are hence remarkably predictable. In this final post of our three-part series, we relate the findings discussed previously to theories of bank failures, and we discuss the policy implications of our findings.

November 21, 2024

Why Do Banks Fail? Three Facts About Failing Banks

Why do banks fail? In a new working paper, we study more than 5,000 bank failures in the U.S. from 1865 to the present to understand whether failures are primarily caused by bank runs or by deteriorating solvency. In this first of three posts, we document that failing banks are characterized by rising asset losses, deteriorating solvency, and an increasing reliance on expensive noncore funding. Further, we find that problems in failing banks are often the consequence of rapid asset growth in the preceding decade.

November 12, 2024

Banking System Vulnerability: 2024 Update

After a period of relative stability, a series of bank failures in 2023 renewed questions about the fragility of the banking system. As in previous years, we provide in this post an update of four analytical models aimed at capturing different aspects of the vulnerability of the U.S. banking system using data through 2024:Q2 and discuss how these measures have changed since last year.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Liquidity | Permalink | Comments (4)

April 15, 2024

Can I Speak to Your Supervisor? The Importance of Bank Supervision

In March of 2023, the U.S. banking industry experienced a period of significant turmoil involving runs on several banks and heightened concerns about contagion. While many factors contributed to these events—including poor risk management, lapses in firm governance, outsized exposures to interest rate risk, and unrecognized vulnerabilities from interconnected depositor bases, the role of bank supervisors came under particular scrutiny. Questions were raised about why supervisors did not intervene more forcefully before problems arose. In response, supervisory agencies, including the Federal Reserve and Federal Deposit Insurance Corporation, commissioned reviews that examined how supervisors’ actions might have contributed to, or mitigated, the failures. The reviews highlighted the important role that bank supervisors can play in fostering a stable banking system. In this post, we draw on our recent paper providing a critical review and summary of the empirical and theoretical literature on bank supervision to highlight what that literature tells us about the impact of supervision on supervised banks, on the banking industry and on the broader economy.

Posted at 7:00 am in Bank Capital, Banks, Federal Reserve, Financial Institutions, Regulation | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics