Housing is the largest component of assets held by households in the United States, totaling $48 trillion in 2025. When natural disasters strike, the resulting damage to homes can be large relative to households’ liquid savings. Homeowner’s insurance is the primary financial tool households use to protect themselves against property risk. Despite the economic importance of homeowner’s insurance, we know surprisingly little about how insurance contracts are actually designed with respect to property risk. In this post, which is based on our new paper, “Economics of Property Insurance,” we examine how homeowner’s insurance contracts are structured in practice. Using a new granular dataset covering millions of homeowner’s insurance policies, we document four striking patterns about coverage limits, deductibles, insurance pricing, and the distribution of property losses.

The Basic Structure of Homeowner’s Insurance Contracts

A homeowner’s insurance contract transfers the financial consequences of property damage from the household to the insurer in exchange for a monthly premium. The three main terms in the contract are: the premium, the coverage limit, and the deductible. The premium is the price households pay for insurance. The coverage limit sets the maximum amount the insurer will pay if a loss occurs. The deductible is the portion of the loss the household must pay before the insurer begins covering damages. Together, these contract terms determine how much risk is transferred to the insurer and how much remains with the household.

Why do these terms exist? Economic theory highlights the role of frictions due to information asymmetries between insurers and policyholders. In a frictionless setting, theory predicts that full insurance would be optimal, meaning that losses would be fully covered. In practice, however, frictions exist because insurers cannot perfectly observe how well homeowners maintain or protect their properties. Deductibles and coverage limits help address these frictions. By exposing households to part of the loss, these contract features can mitigate moral hazard by encouraging policyholders to maintain their homes and reduce damage risk.

We analyze millions of homeowner’s insurance contracts from 2021 using ICE McDash—contract-level data from residential mortgage servicers—merged with property-level disaster risk metrics from CoreLogic. ICE McDash captures each insurance policy’s premium, deductible, coverage limit, insurer, and associated mortgage loan. CoreLogic provides average annual loss and tail risk metrics for each property. By merging these datasets, we observe each policyholder’s insurance policy details and the disaster risk their home faces.

Fact 1: Coverage Limits Rarely Bind

Damages rarely approach the coverage limit. The median coverage limit equals 77 percent of the home’s recovery value (the cost to fully rebuild the property). Yet even in a severe one-in-one-hundred year event, losses for the median policy are only 1.4 percent of recovery value. This implies that realized losses almost never approach the coverage limit. As a result, reducing coverage limits would have little effect on expected insurer payouts.

Instead, the economically important margin of the contract is the deductible. Deductibles determine whether any payout occurs at all and therefore play a central role in shaping both household risk exposure and incentives for property maintenance.

This pattern has implications for how we interpret insurance prices. Measures such as premium divided by coverage limit are often used as proxies for the price of insurance. However, because coverage limits rarely bind, such measures may not be informative about the effective price of insurance. Expected payouts depend crucially on the deductible and the distribution of losses relative to it, not simply on the nominal coverage limit.

Fact 2: Deductibles Are Small Relative to Property Value but Large Relative to Expected Loss

Deductibles are typically offered in discrete, round-number increments, such as $500, $1,000, $1,500, $2,000, $2,500, or $5,000, with $1,000 being the most common choice. Therefore, compared to property value, deductibles appear small: the median deductible is about 0.3 percent of the home’s recovery value.

However, expected losses are even smaller. The median annual expected loss is only 0.09 percent of property recovery value, well below the median deductible. Even after adjusting expected losses to account for non-disaster-related components, we find that deductibles are large relative to expected losses. Because a sizable portion of losses occurs in the range of losses where the deductible applies, deductibles play a central role in determining household risk retention and in incentivizing owners to take due care of their properties.

Fact 3: Premiums Substantially Exceed Expected Losses

Premiums are much larger than the expected claims they pay out. The median ratio of annual expected loss to premium is 28 percent, indicating that expected claim costs account for only a portion of the premium households pay.

This pattern is robust to several adjustments. Excluding the flood component slightly reduces the ratio to 26 percent, while adjusting for theft and liability shares increases it to 32 percent. Even under an aggressive assumption where CoreLogic captures only catastrophe events rather than the full loss distribution, the ratio reaches 43 percent—still implying that premiums substantially exceed expected losses. This pattern is consistent with risk-aversion of policyholders. Households are willing to pay more than the expected claim payout in order to transfer disaster risk off their balance sheets, generating a risk premium in insurance prices.

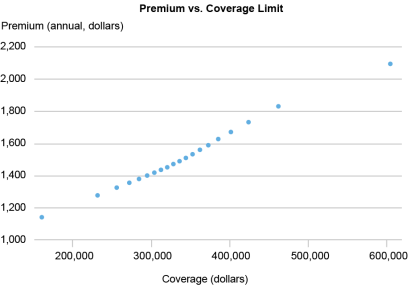

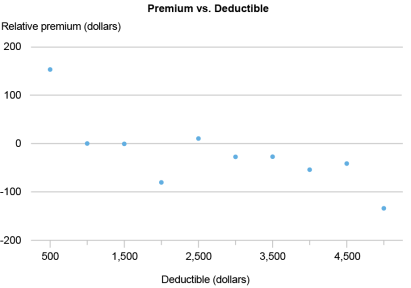

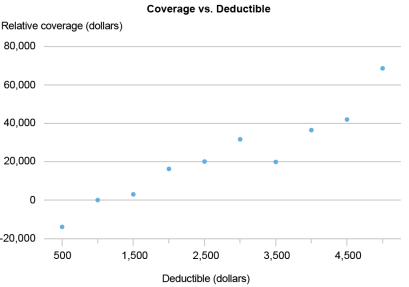

The chart below illustrates how premiums relate to other contract terms. The top panel shows that premiums increase with coverage after controlling for expected loss, property value, deductible, and insurer and state fixed effects. This reflects the fact that higher coverage shifts more potential losses to the insurer. The middle panel shows that premiums decrease as deductibles rise, holding coverage and risk constant, consistent with households retaining more of the initial loss. The bottom panel shows that deductibles tend to increase with coverage after controlling for premiums and the same set of variables.

Relationship Between Premiums, Coverage, and Deductibles

Fact 4: Damage Risk Is Low on Average But Skewed to the Right

Property losses are small on average but can be much larger in the tail of the distribution. The median expected annual loss rate is only 0.09 percent of property value. However, losses in rare events are much larger: the median 98th percentile loss rate is 0.8 percent, and the 99th percentile loss rate is 1.4 percent. In other words, although the expected annual loss is less than 0.1 percent of property recovery value, a one-hundred-year event is roughly sixteen times larger. This combination of a very small average loss and occasional large shocks implies that the distribution of property damages is highly right-skewed, with substantial mass near zero but a heavy upper tail.

Takeaways

Our analysis reveals four key patterns. Deductibles, not the nominal coverage limit, are the main economic determinants of homeowner’s insurance contracts. Coverage limits rarely bind, while deductibles frequently do. Premiums substantially exceed expected losses, reflecting the value households place on transferring rare but severe risks. And the underlying distribution of property losses is highly skewed, with small average damages but occasional large shocks.

These findings are robust across adjustments. Flood exposure, typically excluded from standard homeowner’s insurance policies, has minimal impact on results when removed. We also adjust for non-disaster claims, such as theft and liability claims, by comparing modeled damages with realized claims data. This adjustment modestly increases estimated losses but does not change the takeaway.

Looking Ahead

Several questions remain. How are premiums, deductibles, and coverage limits jointly determined? How much risk is ultimately retained by households? Does risk retention vary systematically across household types and insurers? And how severe and pervasive is moral hazard in homeowner’s insurance? In a future post, we will introduce a structural model of property insurance contracts that links household risk preferences, disaster risk, and optimal contract design.

Hyeyoon Jung is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

Jaehoon (Kyle) Jung is an assistant professor at the NYU Stern School of Business.

How to cite this post:

Hyeyoon Jung and Jaehoon (Kyle) Jung, “What Millions of Homeowner’s Insurance Contracts Reveal About Risk Sharing,” Federal Reserve Bank of New York Liberty Street Economics, April 13, 2026, https://doi.org/10.59576/lse.20260413

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics