40 posts on "Corporate Finance"

October 13, 2021

Insurance Companies and the Growth of Corporate Loan Securitization

Collateralized loan obligation (CLO) issuances in the United States increased by a factor of thirteen between 2009 and 2019, with the volume of outstanding CLOs more than doubling to approach $647 billion by the end of that period. While researchers and policy makers have been investigating the impact of this growth on the cost and riskiness of corporate loans and the potential implications for financial stability, less attention has been paid to the drivers of this phenomenon. In this post, which is based on our recent paper, we shed light on the role that insurance companies have played in the growth of corporate loans’ securitization and identify the key factors behind that role.

June 22, 2021

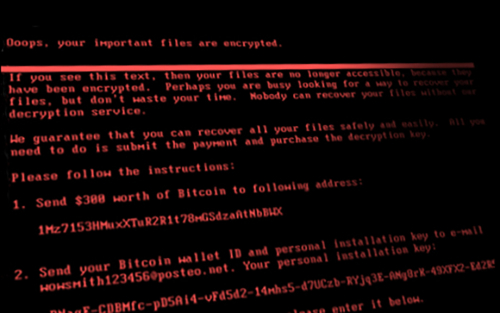

Cyberattacks and Supply Chain Disruptions

Cybercrime is one of the most pressing concerns for firms. Hackers perpetrate frequent but isolated ransomware attacks mostly for financial gains, while state-actors use more sophisticated techniques to obtain strategic information such as intellectual property and, in more extreme cases, to disrupt the operations of critical organizations. Thus, they can damage firms’ productive capacity, thereby potentially affecting their customers and suppliers. In this post, which is based on a related Staff Report, we study a particularly severe cyberattack that inadvertently spread beyond its original target and disrupted the operations of several firms around the world. More recent examples of disruptive cyberattacks include the ransomware attacks on Colonial Pipeline, the largest pipeline system for refined oil products in the U.S., and JBS, a global beef processing company. In both cases, operations halted for several days, causing protracted supply chain bottlenecks.

February 22, 2021

Measuring the Forest through the Trees: The Corporate Bond Market Distress Index

With more than $6 trillion outstanding, the U.S. corporate bond market is a significant source of funding for most large U.S. corporations. While prior literature offers a variety of measures to capture different aspects of corporate bond market functioning, there is little consensus on how to use those measures to identify periods of distress in the market as a whole. In this post, we describe the U.S. Corporate Bond Market Distress Index (CMDI), which offers a single measure to quantify joint dislocations in the primary and secondary corporate bond markets. As detailed in a new working paper, the index provides more salient information about the state of the corporate bond market relative to common measures of financial stress, thereby more accurately identifying periods of widespread dislocation in the market.

December 1, 2020

The Costs of Corporate Debt Overhang Following the COVID‑19 Outbreak

Leading up to the COVID-19 outbreak, there were growing concerns about corporate sector indebtedness. High levels of borrowing may give rise to a “debt overhang” problem, particularly during downturns, whereby firms forego good investment opportunities because of an inability to raise additional funding. In this post, we show that firms with high levels of borrowing at the onset of the Great Recession underperformed in the following years, compared to similar—but less indebted—firms. These findings, together with early data on the revenue contractions following the COVID-19 outbreak, suggest that debt overhang during the COVID-recession could lead to an up to 10 percent decrease in growth for firms in industries most affected by the economic repercussions of the battle against the outbreak.

October 19, 2020

How Has Post‑Crisis Banking Regulation Affected Hedge Funds and Prime Brokers?

“Arbitrageurs” such as hedge funds play a key role in the efficiency of financial markets. They compare closely related assets, then buy the relatively cheap one and sell the relatively expensive one, thereby driving the prices of the assets closer together. For executing trades and other services, hedge funds rely on prime brokers and broker-dealers. In a previous Liberty Street Economics blog post, we argued that post-crisis changes to regulation and market structure have increased the costs of arbitrage activity, potentially contributing to the persistent deviations in the prices of closely related assets since the 2007–09 financial crisis. In this post, we document how post-crisis changes to bank regulations have affected the relationship between hedge funds and broker-dealers.

Posted at 7:00 am in Bank Capital, Banks, Central Bank, Corporate Finance, Financial Institutions, Financial Markets, Regulation | Permalink

October 13, 2020

Weathering the Storm: Who Can Access Credit in a Pandemic?

Credit enables firms to weather temporary disruptions in their business that may impair their cash flow and limit their ability to meet commitments to suppliers and employees. The onset of the COVID recession sparked a massive increase in bank credit, largely driven by firms drawing on pre-committed credit lines. In this post, which is based on a recent Staff Report, we investigate which firms were able to tap into bank credit to help sustain their business over the ensuing downturn.

August 4, 2020

Tracking the COVID‑19 Economy with the Weekly Economic Index (WEI)

At the end of March, we launched the Weekly Economic Index (WEI) as a tool to monitor changes in real activity during the pandemic. The rapid deterioration in economic conditions made it important to assess developments as soon as possible, rather than waiting for monthly and quarterly data to be released. In this post, we describe how the WEI has measured the effects of COVID-19. So far in 2020, the WEI has synthesized daily and weekly data to measure GDP growth remarkably well. We document this performance, and we offer some guidance on evaluating the WEI’s forecasting abilities based on 2020 data and interpreting WEI updates and revisions.

Posted at 2:58 pm in Corporate Finance, Forecasting, Macroeconomics, Pandemic, Recession | Permalink

May 15, 2020

The Commercial Paper Funding Facility

This post documents dislocations in the commercial paper market following the COVID-19 outbreak that motivated the Fed to create the Commercial Paper Funding Facility, and tracks the subsequent improvement in market conditions.

Posted at 7:00 am in Central Bank, Corporate Finance, COVID-19 Facilities, Federal Reserve, Financial Markets, Liquidity, Pandemic | Permalink

April 17, 2020

Treasury Market Liquidity during the COVID‑19 Crisis

A key objective of recent Federal Reserve policy actions is to address the deterioration in financial market functioning. The U.S. Treasury securities market, in particular, has been the subject of Fed and market participants’ concerns, and the venue for some of the Fed’s initiatives. In this post, we evaluate a basic metric of market functioning for Treasury securities—market liquidity—through the first month of the Fed’s extraordinary actions. Our particular focus is on how liquidity in March 2020 compares to that observed over the past fifteen years, a period that includes the 2007-09 financial crisis.

Posted at 12:01 pm in Balance of Payments, Banks, Central Bank, Corporate Finance, Financial Markets, Pandemic | Permalink | Comments (1)

January 8, 2020

What’s in A(AA) Credit Rating?

Rising nonfinancial corporate business leverage, especially for riskier “high-yield” firms, has recently received increased public and supervisory scrutiny. For example, the Federal Reserve’s May 2019 Financial Stability Report notes that “growth in business debt has outpaced GDP for the past 10 years, with the most rapid growth in debt over recent years concentrated among the riskiest firms.” At the upper end of the credit spectrum, “investment-grade” firms have also increased their borrowing, while the number of higher-rated firms has decreased. In fact, there are currently only two U.S. companies rated AAA: Johnson & Johnson and Microsoft. In this post, we examine recent trends in the issuance of investment-grade corporate bonds and argue that the combination of increased BAA issuance and virtually nonexistent AAA issuance both reduces the usefulness of the BAA–AAA spread as a credit risk indicator and poses a financial stability concern.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics