3 posts on "Fedwire Funds"

December 20, 2024

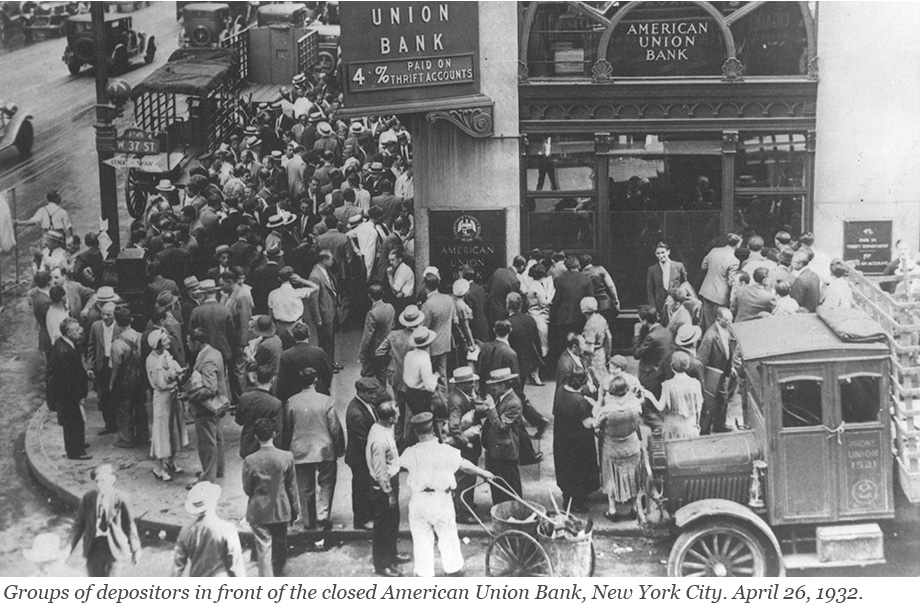

Anatomy of the Bank Runs in March 2023

Runs have plagued the banking system for centuries and returned to prominence with the bank failures in early 2023. In a traditional run—such as depicted in classic photos from the Great Depression—depositors line up in front of a bank to withdraw their cash. This is not how modern bank runs occur: today, depositors move money from a risky to a safe bank through electronic payment systems. In a recently published staff report, we use data on wholesale and retail payments to understand the bank run of March 2023. Which banks were run on? How were they different from other banks? And how did they respond to the run?

Posted at 6:30 am in Banks, Crisis, Financial Institutions, Lender of Last Resort, Panic | Permalink | Comments (1)

October 21, 2024

The Dueling Intraday Demands on Reserves

A central use of reserves held at Federal Reserve Banks (FRBs) is for the settlement of interbank obligations. These obligations are substantial—the average daily total reserves used on two main settlement systems, Fedwire Funds and Fedwire Securities, exceeds $6.5 trillion. The total amount of reserves needed to efficiently settle these obligations is an active area of debate, especially as the Federal Reserve’s current quantitative tightening (QT) policy seeks to drain reserves from the financial system. To better understand the use of reserves, in this post we examine the intraday flows of reserves over Fedwire Funds and Fedwire Securities and show that the mechanics of each settlement system result in starkly different intraday demands on reserves and differing sensitivities of those intraday demands to the total amount of reserves in the financial system.

August 25, 2014

Turnover in Fedwire Funds Has Dropped Considerably since the Crisis, but It’s Okay

Funds Service is a large-value payment system, operated by the Federal Reserve Bank of New York, that facilitates more than $3 trillion a day in payments.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics