A few months ago, the federal government was once again confronted with the need to raise the statutory limit on the amount of debt issued by the Treasury. As in the past, the protracted stalemate and associated uncertainty led to calls to eliminate the debt ceiling. In this post, I make the counterargument. Likely because of its straightforwardness, the debt ceiling has been an effective “fiscal rule.” The reduction of the federal deficit from the mid-1980s to the mid-1990s was due in large part to a series of budget compromises, all of which were accompanied by the need to raise the debt ceiling.

It is widely accepted that the United States is on an unsustainable fiscal trajectory. From 36.2 percent at the end of fiscal year 2007, federal debt held by the public expressed as a percentage of GDP is projected to have reached around 67 percent by the end of fiscal year 2011, according to the Congressional Budget Office (CBO). Moreover, under current policies, it is projected to reach 95-100 percent by the end of fiscal year 2021. The debt ceiling of $14.294 trillion, which became effective in early 2010, became binding in May 2011. The Treasury resorted to methods learned in past debt ceiling impasses to continue meeting obligations while not exceeding the limit on debt. But those methods were projected to be exhausted by early August. For much of the month of July, the country was riveted to the crafting of legislation to raise the ceiling. Financial markets and the overall economy were confronted with the risk that the ceiling would not be raised in time, thereby resulting in a sharp decline in federal outlays. The situation led some to argue that the time has come to eliminate the debt ceiling. For example, columnist George Will noted that the United States is the only developed nation with such a law, and that it is potentially dangerous because there is a strong desire by some members of Congress to cast a symbolic vote against increasing it. Similarly, Moody’s argued that the debt ceiling “creates periodic uncertainty” and “adds a small probability of default that would not otherwise exist” if the debt ceiling were eliminated.

While in some cases, the raising of the debt ceiling is a routine matter that receives little attention, there have been many episodes in which it became a protracted and politically divisive affair. Indeed, that was the case the last time the United States faced an unsustainable fiscal trajectory. By 1985, the country had experienced three consecutive fiscal years of federal deficits of around 5 percent of GDP. While still relatively low, federal debt held by the public had risen by roughly 10 percentage points of GDP from 1980 to 1985, requiring that the debt ceiling be raised fourteen times over that six-year period. Concern about this rapid increase in debt intensified, both domestically and abroad, setting in motion a series of legislative efforts to put U.S. fiscal policy back on a sustainable path. This process began with the passage of Gramm-Rudman-Hollings I and II, enacted in 1985 and 1987, respectively, followed by the Omnibus Budget Reconciliation Act of 1990 and the Omnibus Budget Reconciliation Act of 1993. In all four cases, the need to raise the debt ceiling increased the sense of urgency and no doubt contributed to the various compromises that needed to take place. Below are brief descriptions of each Act.

- Balanced Budget and Emergency Deficit Control Act of 1985 (Gramm-Rudman-Hollings I)

This Act directed the relevant committees of the House and Senate to craft legislation creating an alternative minimum tax on corporations. It also set declining deficit maximums for each year through fiscal year 1991, at which point the budget was to be balanced. It established an enforcement mechanism for meeting those targets called “sequestration,” under which automatic and across-the-board reductions of previously approved spending (except for Social Security, interest, and certain entitlement programs) would take place if the projected deficit exceeded the target. The sequestration process was to be controlled by the General Accounting Office, a branch of Congress. First and foremost, however, the legislation was enacted to increase the debt ceiling to $2.079 trillion. - Balanced Budget and Emergency Deficit Control Reaffirmation Act of 1987 (Gramm-Rudman-Hollings II)

The Supreme Court ruled that having the sequestration trigger in the hands of the General Accounting Office was a violation of the Constitutional principle of separation of powers. Under this legislation, the sequestration trigger was placed in the hands of the Director of the Office of Management and Budget, an office of the Executive Branch. In addition, the deficit targets were revised and extended to fiscal year 1993, at which time the budget was to be balanced. The bill to which these changes in budget procedures were attached was one to increase the debt ceiling by $448 billion, to $2.8 trillion, following two small increases earlier in the year. - Omnibus Budget Reconciliation Act of 1990 (OBRA90)

The federal government did not meet the Gramm-Rudman-Hollings II deficit target for fiscal year 1989, and at the beginning of 1990 the CBO projected that the targets through 1993 would also not be met. This set in motion a protracted series of negotiations to craft a deficit reduction package, which was ultimately enacted in early November 1990. According to the CBO, the package included tax increases and spending reductions, along with interest, totaling roughly $500 billion over five years, which put the projected deficit on a declining path. Small increases in the debt ceiling were enacted in August and October 1990. But one title of the Act provided for a $915 billion increase in the debt ceiling, which was thought to be sufficient to get through the November 1992 national elections.Title XIII of the legislation is the Budget Enforcement Act, which significantly altered the budget enforcement mechanisms of Gramm-Rudman-Hollings. First, it effectively eliminated deficit targets. In their place, it established nominal ceilings, or “caps,” on discretionary budget authority and outlays over the period from fiscal year 1991 to fiscal year 1995. Discretionary outlays are those that are controlled by the annual appropriations process. The caps were adjustable to accommodate “emergencies” as well as other extenuating circumstances, such as funding for the International Monetary Fund. When the legislation was initially enacted in 1990, there were three separate caps for defense, international, and nondefense domestic spending for the period from fiscal year 1991 through fiscal year 1993. Then from fiscal year 1994 to fiscal year 1995, there was a single cap covering the total discretionary category.

In addition, the Budget Enforcement Act established the “pay-as-you-go,” or “PAYGO,” process for revenues and direct spending. Direct spending is for the most part entitlements or transfer programs that are established through authorizing legislation. Outlays are determined not by annual appropriations but rather by the eligibility criteria and benefit formulas of the specific programs in combination with underlying economic and demographic conditions. Under PAYGO, all changes in the tax code and in direct spending enacted in a session of Congress must be “deficit neutral” over one-year and five-year horizons. The Senate subsequently enacted a ten-year horizon test as well. PAYGO does not require Congressional action if revenues fall or outlays grow due to changing economic or technical factors. PAYGO was enforced one year at a time, meaning that an overage in one year cannot be offset by an underage in another year. Moreover, an underage or overage in the PAYGO section of the budget cannot be transferred to the discretionary section of the budget and vice versa. Both the discretionary spending caps and PAYGO were enforced through the threat of sequestration.

- Omnibus Budget Reconciliation Act of 1993 (OBRA93)

Despite passage of OBRA90, in early 1993 the CBO projected that the federal deficit for fiscal year 1993 would be 5 percent of GDP and would still be 4 percent of GDP in fiscal year 1996. By the end of March 1993, the federal government was approaching the debt ceiling, which was increased by $225 billion in April. Eventually, a package of tax increases and spending reductions, including interest, totaling about $430 billion over five years was enacted into law on August 10, 1993. In addition, the Act extended the discretionary spending caps and PAYGO through fiscal year 1998. Finally, the Act included a $530 billion increase in the debt ceiling, to $4.9 trillion.

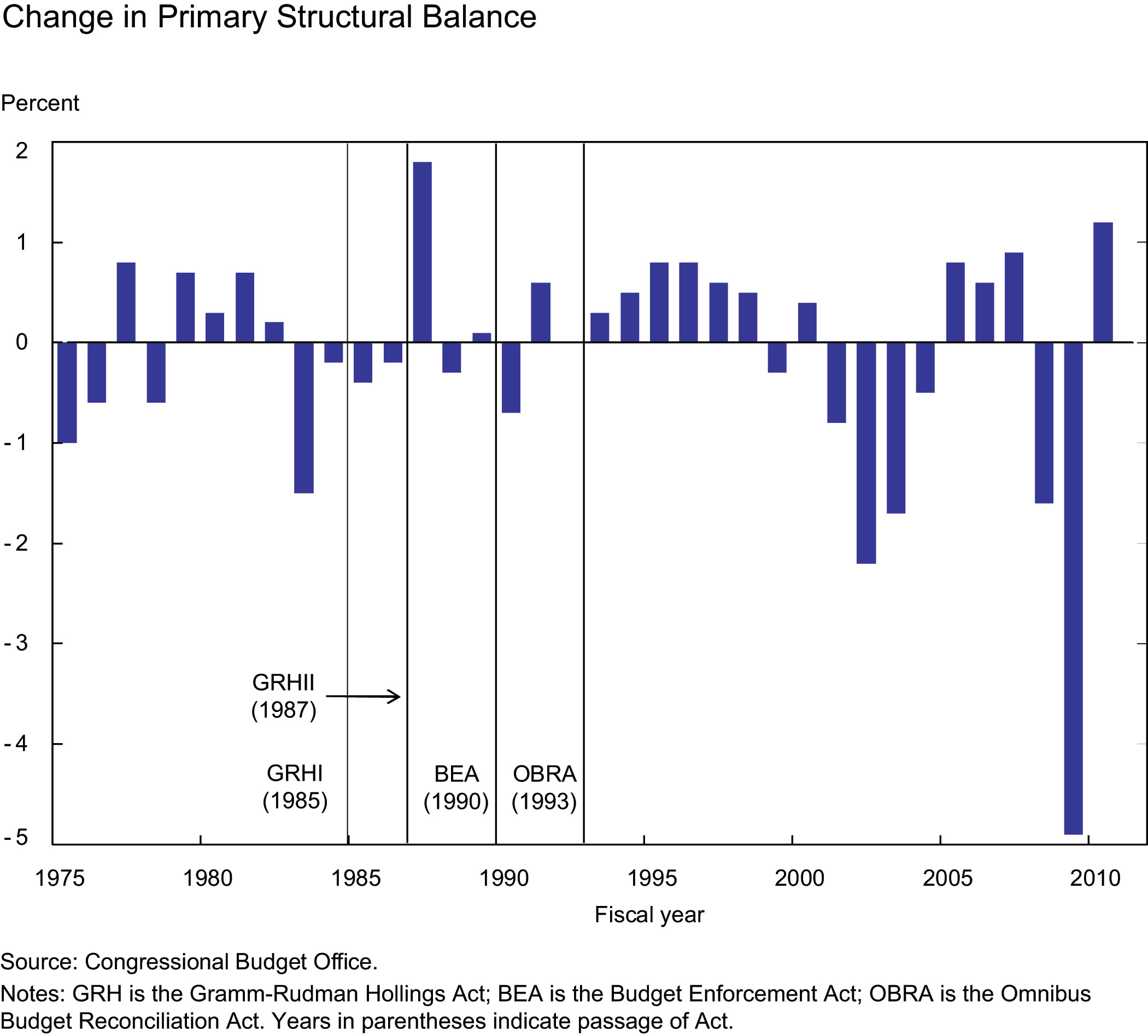

Of course, one can only argue that the debt ceiling is an effective fiscal rule if the legislation that it helped trigger is effective in reducing the deficit. One objective way of answering this question is to look at the change in the primary structural balance in the years immediately after enactment. The structural balance is the difference between what federal receipts and outlays would be if the economy was operating at potential or full employment. Accordingly, this measure of the fiscal balance is not affected by the business cycle. The primary structural balance is the structural balance excluding interest payments on the stock of outstanding debt. By excluding the interest cost of debt accumulated in the past, we are able to better assess the effect of the policy decisions of the present. If the change in the primary structural balance is positive, it signals that the fiscal balance is improving—smaller deficits or larger surpluses. If it is negative, it means that the balance is deteriorating.

The chart below presents changes in the primary structural balance as a percentage of potential GDP, estimated by the CBO, for fiscal years 1980-2010. Included in the chart are the dates of passage of the legislation discussed above. Following passage of Gramm-Rudman-Hollings I, the primary structural deficit continued to increase. Although it may have increased less than otherwise would have been the case, it is generally accepted that this first effort was not as successful as hoped. In the first year after passage of Gramm-Rudman-Hollings II, there was a substantial improvement in the structural balance followed by two years of essentially no change. The passage of the Budget Enforcement Act of 1990 initially resulted in a significant increase in the primary structural deficit, followed by a swing to surplus and then no change. The initial increase in the deficit is widely regarded to have been by design. The economy had entered a recession in mid-1990, and while OBRA90 established caps on discretionary spending, the caps put in place for fiscal year 1991 actually provided for a significant increase over the previous year. Finally, after passage of OBRA93, there were several consecutive years of primary structural surpluses.

One could reasonably argue that the compromises needed to reduce the deficit would have occurred anyway, and there is no way to disprove that position. But unlike many other aspects of the federal budget process, the debt ceiling—or credit limit, if you will—is very transparent. The need to raise it occasionally forces policymakers to confront painful choices that they might otherwise prefer to avoid.

Disclaimer

The views expressed in this blog are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York, or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics

{kind=link}