Oil prices have increased by nearly 60 percent since the summer of 2020, coinciding with an upward trend in global inflation. If higher oil prices are the result of constrained supply, then this could pose some stagflation risks to the growth outlook—a concern reflected in a June Financial Times article, “Why OPEC Matters.” In this post, we utilize the demand and supply decomposition from the New York Fed’s Oil Price Dynamics Report to argue that most of the oil price increase over the past year or so has reflected improving global demand expectations. We then illustrate what these changing global demand expectations might mean for near-term global inflation developments.

Recent Oil Price Developments

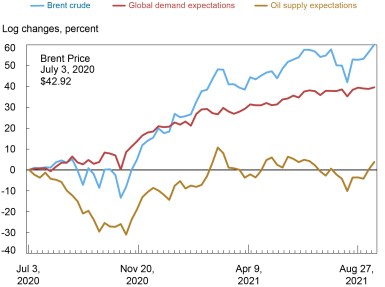

The statistical model underlying the New York Fed’s Oil Price Dynamics Report examines correlations between weekly oil price changes and a broad array of financial and oil production-related variables by means of a limited number of common factors. These are then interpreted as being related to either swings in anticipated global demand or oil supply developments. In the chart below, we plot the cumulative change of the Brent crude oil price since July 2020. The chart also depicts the corresponding expected demand and anticipated supply components of Brent crude prices from the oil price decomposition model. After the oil price collapse in the spring of 2020, Brent crude oil prices recovered very cautiously, as the demand outlook remained muted. Then, toward the end of 2020, oil prices headed into an upward trend, owing to upward revisions to expected demand and downward revisions to expected supply in the second half of 2020. The increases in 2021 up through the end of the summer largely reflect upward revisions to demand expectations.

The Rise in Global Demand Expectations Has Contributed to the Increase in Oil Prices

Source: Authors’ calculations.

Near-Term Global Inflation

Expectations of economic activity have dominated oil price moves over the past year, but what might that mean for near-term inflation globally? The next chart plots the six-month change in global year-over-year CPI inflation versus the expected demand component of the six-month change in Brent crude oil prices, lagged six-months. This chart suggests that current global demand expectations have leading information regarding the acceleration of global CPI inflation over the next six months.

Global Demand Expectations and Global Inflation Growth Have Both Increased Significantly in Previous Months

Source: Authors’ calculations.

Notes: Global inflation is constructed by aggregating inflation rates from Argentina, Brazil, Canada, Chile, China, Colombia, the Euro Area, Hong Kong, India, Indonesia, Japan, Mexico, Malaysia, Norway, the Philippines, Russia, Singapore, South Africa, South Korea, Sweden, Switzerland, Thailand, Turkey, the United Kingdom, the United States, and Vietnam via GDP weights.

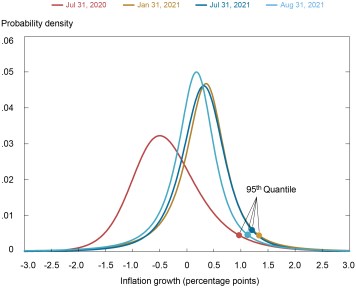

The previous chart highlights that the predictive power of expected demand-driven oil price changes for inflation acceleration over the next six months is stronger for certain periods than others. This link, then, might have varying importance for different parts of the inflation distribution—the tails versus the center, for example. To examine that phenomenon, we construct the forecasted conditional six-month-ahead inflation acceleration distributions, estimated using quantile regressions, as in Adrian et al. (2019). These regressions use the cumulative change in the expected demand component over the previous six months and the one-month change in annualized inflation to create a probability distribution of expected inflation. Furthermore, estimation of the quantile regressions is based on moving ten-year data windows to allow for time-variation in the relationship between demand-based oil price shocks and different parts of the inflation distribution.

In the chart below, we depict the conditional distributions of global inflation acceleration over the next six months on four dates: July 2020 (red), January 2021 (gold), July 2021 (dark blue), and August 2021 (light blue). The August 2021 conditional distribution not only incorporates the six-month cumulative change in the expected demand component of oil prices up to August, but it also adds the cumulative change of the expected demand component for the month of September. A year ago, during the summer of 2020, demand expectations-driven oil price moves suggested significant downside risks to global inflation. This changed dramatically in the subsequent six months, with the median expected six-month acceleration of yearly global inflation moving from -0.4 percentage point in July 2020 to +0.3 percentage point in January 2021. Over the same time span, the six-month cumulative change in the expected demand component of oil prices rose from -8 percent to 22 percent. Between January and July of 2021, this median expectation and corresponding conditional distributions remained broadly unchanged Since then, the median expected rate of inflation acceleration decreased slightly to 0.2 percent and the upside risk to this forecast moderated slightly.

Forecasted Global Inflation Growth Has Decreased Slightly over the Past Month

Source: Authors’ calculations.

Notes: Global inflation is constructed by aggregating inflation rates from Argentina, Brazil, Canada, Chile, China, Colombia, the Euro Area, Hong Kong, India, Indonesia, Japan, Mexico, Malaysia, Norway, the Philippines, Russia, Singapore, South Africa, South Korea, Sweden, Switzerland, Thailand, Turkey, the United Kingdom, the United States, and Vietnam via GDP weights. Aug 31, 2021 Forecast density incorporates changes in the demand component over the month of September.

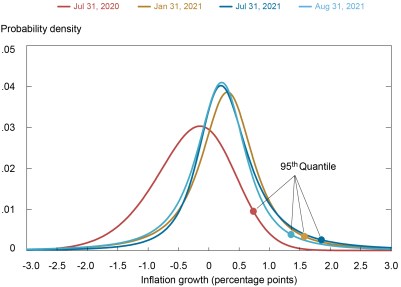

The next chart plots similar distributions for the advanced economies. As was the case globally, there was a dramatic increase in the median expected inflation acceleration inflation between the summer of 2020 (-0.2 percentage point) and the beginning of 2021 (0.3 percentage point) owing to the anticipated recovery of the global economy. Between January and July of 2021, the median expected inflation acceleration in the advanced economies remained unchanged, although the July 2021 distribution became seemingly more skewed to the upside.. Since then, the median expected inflation acceleration in the advanced economies decreased somewhat, from 0.3 percentage point in July to 0.2 percentage point in August, as the conditional distribution experienced a slight compression in its upside tail. This development coincided with a slowdown in the six-month cumulative growth in the demand expectations component of oil prices, from 22 percent at the start of the year to 11 percent in August.

Forecasted Inflation Growth for Advanced Economies Has Decreased Slightly over the Past Month

Source: Authors’ calculations.

Note: Inflation for advanced economies is constructed by aggregating inflations rates from Canada, the Euro Area, Japan, Norway, Sweden, Switzerland, the United Kingdom, and the United States via GDP weights. Aug 31, 2021 Forecast density incorporates changes in the demand component over the month of September.

Conclusion

Changing expectations with respect to global economic activity has driven oil prices up over the past year. Between the summer of 2020 and January 2021, this led to substantial upward shifts in the estimated conditional distributions of near-term global inflation changes. More recently, oil price moves indicate that the impact of changes in anticipated global demand on the near-term inflation outlook has broadly stabilized, as a somewhat lower rate of inflation acceleration over the next six months due to changing demand expectations seems to have been priced in since August.

Jan J. J. Groen is an officer in the Federal Reserve Bank of New York’s Research and Statistics Group.

Adam I. Noble is a senior research analyst in the Bank’s Research and Statistics Group.

Disclaimer

The views expressed in this post are those of the authors and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the authors.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics