Will developments in technology, geopolitics, and the financial market reduce the dollar’s important roles in the global economy? This post updates prior commentary [here, here, and here], with insights about whether recent developments, such as the pandemic and the sanctions on Russia, might change the roles of the dollar. Our view is that the evidence so far points to the U.S. dollar maintaining its importance internationally. A companion post reports on the Inaugural Conference on the International Roles of the U.S. Dollar jointly organized by the Federal Reserve Board and Federal Reserve Bank of New York and held on June 16-17.

Environmental Trends

Looking back over prior decades, the major developments pertinent for the current international financial architecture and dollar roles include the introduction of the euro in 2000, China’s rising status in the global economy, and post-financial-crisis changes in the U.S. policy and financial environment. Additional drivers of roles also historically include the strength of economic and financial market conditions, as well as institutions, across countries.

Some U.S. financial and regulatory approaches since the global financial crisis (GFC), on balance, supported the international roles of the dollar and the so-called safe-haven status of U.S. Treasuries. Crisis containment efforts included enhancing the Federal Reserve’s lender-of-last-resort role around dollar funding (for example, through central bank swap lines) and shoring up bank resiliency under the Dodd-Frank Act. This type of reinforcement of dollar roles has been strengthened since 2020, with dollar funding strains in stress periods reduced by access to the Fed’s swap lines. In addition, the new FIMA (Foreign and International Monetary Authority) Repo Accounts give those official institutions holding U.S. Treasuries the possibility to get dollar liquidity through liquifying, rather than liquidating, these Treasury assets. Goldberg and Ravazzolo (2021) show that the facility supported stabilization and normalization of financial market conditions, giving foreign officials, and private-market participants, confidence to hold U.S. dollar-denominated assets.

Reduced emphasis on unilateralism and protectionism in recent years has also worked in favor of the U.S. dollar’s international roles. While the financial sanctions imposed on Russia after the invasion of Ukraine are sometimes brought up in this context, these sanctions are imposed broadly, inclusive of major currency countries. In advance of the invasion, Russia had already been reducing its reliance on the U.S. dollar in its holdings of official foreign exchange reserves. Of course, it is possible that the desire to avoid this type of sanctions environment could lead to de-dollarization for some other countries, in which case such incremental movements could lead to larger cumulative reductions and fragmentation in the dollar’s international roles.

Over the past several years, another key trend has been the prevalence and growth in the use of digital currencies such as central bank digital currencies (CBDCs) and cryptocurrencies—a development that raises questions about whether such alternatives could eventually supplant a significant portion of the dollar’s international role in cross-border payments and investment and trade transactions. The most relevant developments are in the payments infrastructure space, including around stablecoins. Noteworthy here is the preponderance of efforts to anchor stablecoins against the U.S. dollar: virtually all stablecoins (on a value weighted basis) aim to maintain a “peg” with the dollar. This increased interest in using dollars could be reinforcing, not diminishing, the status of the dollar as an international currency.

CBDCs adopted and studied so far have tended to be focused on domestic retail sectors and therefore would not impinge on the U.S. dollar’s role as an international medium of exchange. As stores of value, CBDCs don’t necessarily increase the attractiveness of their usage vis-à-vis the U.S. dollar. As most are backed by the issuing country’s local currency, they may face the same constraints that prevent the local currency from gaining wider global acceptance and usage, such as credit and liquidity risks and legal protections, as well as openness of the capital account and investment opportunities. Some CBDCs may strengthen the international role of the dollar, notably if they are backed by U.S. dollars, for example, in small open economies.

Evidence

The dollar has many roles globally. First, the dollar is a reserve currency meaning that dollar assets are held by official institutions like central banks and governments, and it is sometimes the anchor currency against which local exchange rates are stabilized.

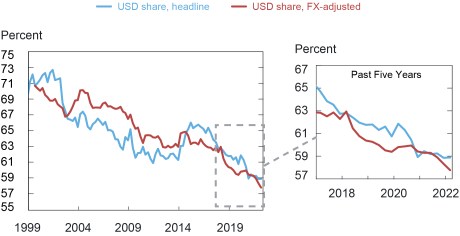

Taking a longer-term perspective, the share of U.S. dollars in global foreign exchange (FX) reserves has slowly but steadily declined over the past two decades, though it remains by far the dominant currency in central bank foreign reserve portfolios (see chart below). Growth in the use of traditional reserve currencies, such as the euro, yen, and pound sterling, has been flat with slight increases in other alternative currencies owing to the search for yield. The Chinese yuan continues to make gradual gains, though still only represents 3 percent of global FX reserves, up from 1 percent in 2017.

The Dollar Share of Global Reserves Has Fallen, but Remains High

Notes: The FX-adjusted series based to 1999 exchange rates.

Meanwhile, the U.S. dollar continues to play a disproportionately large role among FX and payment transactions, global private and official holdings of foreign-denominated assets, and cross-border capital and trade flows. The prominence of the U.S. dollar is typically much greater than that of the second closest rival (euro), with no evidence of this pattern shifting.

In private transactions, although the United States only makes up a quarter of global GDP and just over 16 percent of world exports and imports, the U.S. dollar continues to be represented at a disproportionately higher rate in financial transactions. Approximately half of all cross-border loans, international debt securities, and trade invoices are denominated in U.S. dollars, while roughly 40 percent of SWIFT messages and 60 percent of global foreign exchange reserves are in dollars.

FX transactions are also heavily dollar-based, with close to 90 percent of all currency trades having the dollar as one leg of the transaction. The U.S. dollar remains by far the most traded currency according to the latest Bank for International Settlements (BIS) Triennial Survey in 2019, and it has steadily increased its share of representation on one side of an FX trade to almost 90 percent. Broken down by transaction type involving the dollar, roughly 50 percent of daily transactions are FX swaps, 30 percent are FX spot, and the remaining 20 percent are composed of forwards, options, and cross-currency swaps. Actively traded commodity contracts, such as oil futures, remain mostly denominated in U.S. dollars.

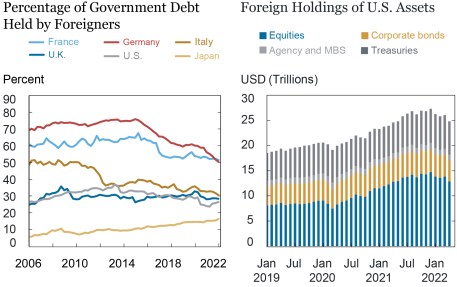

With respect to global sovereign debt, the United States has the largest investable market, thus providing a deep pool of liquidity for dollar-denominated investments. Foreign ownership of U.S. government debt is currently at around 25 percent, a notable decline from 37 percent in 2013, as increased U.S. Treasury issuance outpaced foreign investor demand (see chart below). While the total quantity of U.S. government debt outstanding is notably higher than any other sovereign debt market, the share held by foreigners is largely in line with those of other countries. When excluding Fed holdings, foreign ownership is at about 32 percent, a decline from 42 percent in 2013. Regarding foreign ownership of U.S. securities, while holdings of U.S. Treasuries, mortgage-backed securities, and corporate bonds have remained relatively stable, foreign holdings of U.S. equities have increased by as much as 83 percent in the past three years.

Foreigners Hold Substantial U.S. Private and Public Assets

The dollar also garners more interest from global banks than any other currency. It is the most commonly held denomination among external bank assets, which include loans to nonresidents and foreign-currency denominated securities, with a balance of around $16.7 trillion in the most recent data and up from a post-global-financial-crisis low of around $9 trillion. Global banks’ U.S. dollar-denominated liabilities have been steadily increasing since the GFC and are the highest among major international currencies, with a balance of over $15 trillion in 2021. The only other currency with a notable amount is the euro, at over $9 trillion of foreign-denominated bank liabilities. The share of U.S.-dollar-denominated external claims funded by FX swaps and forward instruments has significantly increased since the GFC to almost $1.4 trillion in 2021, surpassing that of euro-denominated claims in late 2016. In addition, approximately two-thirds of all dollars in circulation are also held abroad, illustrating its continued global appeal as a safe asset.

Concluding Remarks

The dollar’s international role, whether for trade, investment, or use as a global reserve currency, remains quite strong with nothing on the horizon likely to rival it. Some official-use indicators do point to some erosion, notably in foreign currency reserve holdings, and the use of economic sanctions has caused some countries to rethink their reliance on the U.S. dollar. Moreover, rising U.S. public debt levels and inflation could become more concerning to foreign investors. However, no currency replicates the characteristics of the U.S. dollar as a store of value, unit of account, and medium of exchange. Moreover, U.S. assets are viewed to be safe and liquid and have withstood the effects of global shocks. The use of key policy tools, such as the Fed’s dollar liquidity swap lines and FIMA repo, help to support the U.S. dollar’s international roles.

Linda S. Goldberg is a financial research advisor for Financial Intermediation Policy Research in the Federal Reserve Bank of New York’s Research and Statistics Group.

Robert Lerman is a policy and market monitoring advisor in the Bank’s Markets Group.

Dan Reichgott is a capital markets trading principal in the Bank’s Markets Group.

How to cite this post:

Linda S. Goldberg, Robert Lerman, and Dan Reichgott, “The U.S. Dollar’s Global Roles: Revisiting Where Things Stand,” Federal Reserve Bank of New York Liberty Street Economics, July 5, 2022, https://libertystreeteconomics.newyorkfed.org/2022/07/the-u-s-dollars-global-roles-revisiting-where-things-stand/.

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics