At its June 2021 meeting, the FOMC maintained its target range for the fed funds rate at 0 to 25 basis points, while two of the Federal Reserve’s administered rates—interest on reserve balances and the overnight reverse repo (ON RRP) facility offering rate—each were increased by 5 basis points. What do these two simultaneous decisions mean? In today’s post, we look at “technical adjustments”—a tool the Fed can deploy to keep the FOMC’s policy rate well within the target range and support smooth market functioning.

Administered Rates and Rate Control

As noted in the first post of this series, the FOMC chooses the target range for the fed funds rate to communicate the stance of monetary policy. The goal of monetary policy implementation is then to make sure that the effective federal funds rate (EFFR) remains in that range.

In the current framework, the Fed’s main implementation tools are interest on the reserve balances (IORB) that banks hold overnight in their accounts at the Fed, and the rate offered at the ON RRP facility to a broad set counterparties including money market funds and government-sponsored enterprises.

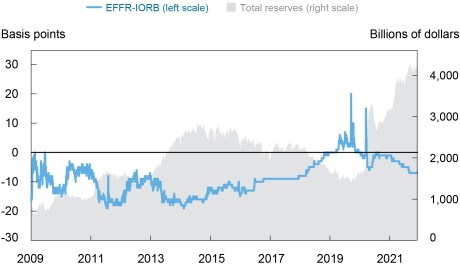

As displayed in the next chart, the spread between the EFFR and the IORB rate fluctuates modestly over time and changes with the level of reserves, among other factors. When the supply of reserves is very large, due to policies such as asset purchases as was the case between 2013 and 2014, the EFFR can print significantly below the IORB rate. The available supply of safe investments like Treasury bills can also influence the EFFR, as suggested in this Liberty Street Economics post. At such times, the ON RRP rate serves as a floor for the EFFR, limiting the range below the IORB rate at which it will print. As the supply of reserves declines, the spread tends to narrow, as can be seen between 2017 and 2019. In 2019, the EFFR briefly exceeded the IORB rate.

The Spread Between the EFFR and the IORB Rate is Subject to Periodic Fluctuations

Sources: Federal Reserve Economic Data (FRED); authors’ calculations.

Note: IORB is interest on reserve balances. EFFR is effective federal funds rate. Month-end observations are dropped.

Since the spread between the EFFR and the IORB rate can fluctuate over time, if the IORB rate remained in the same spot, relative to the target range, the EFFR could move to the top or bottom of the target range. One option the Fed has to prevent this is to implement a “technical adjustment” to steer trading in the fed funds market without changing the stance of monetary policy.

What’s a Technical Adjustment?

A technical adjustment is a change to the IORB rate and/or the ON RRP rate that is intended to enhance the effectiveness of policy implementation by fostering trading in the fed funds market at rates well within the target range, rather than change the stance of monetary policy. A technical adjustment can occur when there is no change in the target range and the Fed adjusts administered rates relative to the existing target range. It also can be coincident with a change in the FOMC’s target range. In this case, one or both administered rates are adjusted by a different amount than the shift in the target range. A technical adjustment, in and of itself, does not imply a change in the stance of monetary policy.

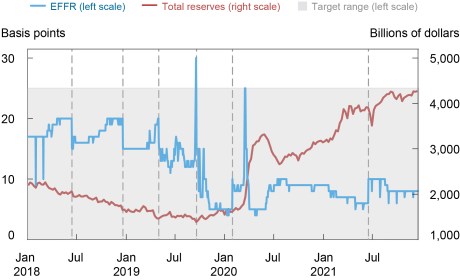

At the start of 2018, the IORB rate was set at the top of the target range, as it had been since the FOMC switched to a target range in late 2008. As the supply of reserves decreased over the first half of 2018, the EFFR drifted higher, closer to the top of the target range. With the EFFR printing just five basis points from the top of the target range, in June 2018, the Fed implemented its first technical adjustment. The IORB rate was lowered to five basis points below the top of the range, when the FOMC increased its target range and the ON RRP rate each by 25 basis points, while the IORB rate was only increased by 20 basis points. As the chart below shows, the EFFR responded quickly to adjustments in the IORB rate.

The EFFR Responds Quickly to Technical Adjustments

Sources: Federal Reserve Economic Data (FRED); authors’ calculations.

Note: EFFR is effective federal funds rate. Dashed vertical lines correspond to technical adjustments. Shaded area represents the FOMC target range for the federal funds rate. Rates are displayed as spreads relative to the lower bound of the target range.

The Fed implemented three additional technical adjustments through September 2019, each one with downward shifts in the IORB and/or ON RRP rates. The technical adjustments in 2018 and 2019 pushed the EFFR (and the distribution of trades in the fed funds market) lower, providing greater assurance that the EFFR would remain within the target range.

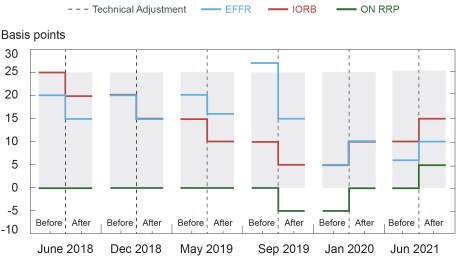

In contrast, the two technical adjustments in 2020 and 2021, when fed funds were trading close to the bottom of the target range, implemented upward shifts of the IORB and ON RRP rates to foster trading in the fed funds market well within the target range. In January 2020, the IORB and ON RRP rates were each increased 5 basis points after the EFFR printed as few as 4 basis points above the bottom of the range. In mid-June 2021, the Fed again shifted the IORB and ON RRP rates upward by 5 basis points, as the EFFR had printed within 5 basis points of the bottom of the target range. As with the initial four technical adjustments to incentivize fed funds trading lower in the target, the 2020 and 2021 technical adjustments were effective at fostering trading in the fed funds market at rates well within the target range, as the chart below shows.

EFFR Before and After Technical Adjustments

Sources: Bloomberg L.P., Federal Reserve Economic Data (FRED); authors’ calculations.

Note: EFFR is effective federal funds rate. IORB is interest on reserve balances. ON RRP is overnight reverse repurchase agreement rate. Rates correspond to averages over the two days prior and after a technical adjustment and are displayed as spreads relative to the lower bound of the target range. Shaded area represents the FOMC target range for the federal funds rate and is displayed relative to the lower bound of the target range.

In addition to helping maintain the EFFR within the FOMC’s target range, technical adjustments can support smooth functioning of money markets in some environments. As noted in a speech by SOMA manager Lorie Logan, the June 2021 adjustment in the ON RRP rate from zero to 5 basis points helped mitigate the risk of further downward pressure on rates that could have arisen if some money market investors, challenged by near zero secured rates, started to limit inflows.

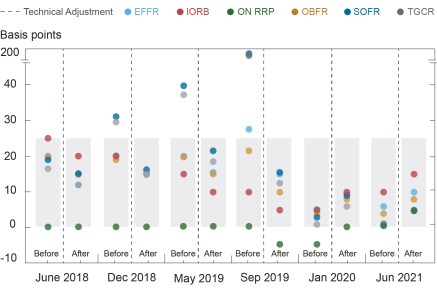

Do Technical Adjustments Work? Yes!

The chart above shows that when the Fed implemented a technical adjustment, the level of the EFFR adjusted immediately by a similar amount. Linkages and arbitrage relationships between money markets extend the impact of technical adjustments beyond the fed funds market to other short-term money markets including Eurodollar and repo markets. Following each of the six technical adjustments, passthrough to measures of overnight uncollateralized funding rates such as the overnight bank funding rate (OBFR), and of collateralized rates such as the secured overnight financing rate (SOFR) and the tri-party general collateral rate (TGCR), has been roughly one-for-one, as shown in the chart below. For example, in June 2021 when the IORB and ON RRP rates were increased by 5 basis points, the OBFR, SOFR, and TGCR all increased by 4 basis points, same as for the EFFR.

Selected Rates Before and After Technical Adjustments

Sources: Bloomberg, L.P., Federal Reserve Economic Data (FRED); authors’ calculations.

Note: EFFR is effective federal funds rate. IORB is interest on reserve balances. OBFR is overnight bank funding rate. SOFR is secured overnight financing rate. TGCR is tri-party general collateral rate. ON RRP is overnight reverse repurchase agreement rate. Rates correspond to averages over the two days before and after a technical adjustment and are displayed as spreads relative to the lower bound of the target range. Shaded area represents the FOMC target range for the federal funds rate and is displayed relative to the lower bound of the target range.

To Sum Up

The IORB and ON RRP rates are the primary tools the Fed uses to implement monetary policy. The level of these rates can be adjusted, relative to the target range, depending on conditions in money markets. Such a technical adjustment is an effective tool to reposition the EFFR within the target range.

Gara Afonso is an assistant vice president in the Federal Reserve Bank of New York’s Research and Statistics Group.

Lorie Logan is an executive vice president in the Bank’s Markets Group and manager of the System Open Market Account for the Federal Open Market Committee.

Antoine Martin is a senior vice president in the Bank’s Research and Statistics Group.

William Riordan is an assistant vice president in the Bank’s Markets Group.

Patricia Zobel is a vice president in the Bank’s Markets Group and deputy manager of the System Open Market Account for the Federal Open Market Committee.

Disclaimer

The views expressed in this post are those of the authors and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the authors.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics