Daily take-up at the overnight reverse repo (ON RRP) facility increased from less than $1 billion in early March 2021 to just under $2 trillion on December 31, 2021. In the second post in this series, we take a closer look at this important tool in the Federal Reserve’s monetary policy implementation framework and discuss the factors behind the recent increase in volume.

In yesterday’s post, we presented a stylized view of the Fed’s implementation framework for monetary policy, in which (i) the Federal Open Market Committee (FOMC) communicates the stance of monetary policy through a target range for the federal funds rate, (ii) interest on reserve balances (IORB) is a key tool, and (iii) an ample supply of reserves ensures that the interest rate paid on banks’ reserve balances maintains the effective federal funds rate (EFFR) within the target range. However, in the United States, banks are only a part of the money market ecosystem—nonbank financial institutions make up a significant share of lending activity.

As a result, the FOMC employs another tool called the ON RRP facility, which is available to a wide range of money market lenders. This facility is particularly important for monetary policy implementation in periods when reserves are elevated. As reserves grow, banks’ willingness to take on additional reserves diminishes, and they reduce the rates they pay for deposits and other funding. In this environment, market rates trade below the IORB rate because nonbank lenders are willing to lend at such rates. For example, the Federal Home Loan Banks (FHLBs), which are important lenders in the fed funds market and not eligible to earn IORB, are willing to lend at rates below the IORB rate rather than leave funds unremunerated in their accounts at the Fed. To provide a floor under the fed funds rate, the FOMC introduced the ON RRP facility.

What’s the ON RRP Rate and How Does It Work?

In concept, the ON RRP facility acts like IORB for a set of nonbank money market participants. Through the ON RRP facility, eligible institutions—money market funds, government-sponsored enterprises, primary dealers, and banks—can invest overnight with the Fed through a repurchase agreement (repo).

By setting the ON RRP rate, the FOMC establishes a floor on the rates at which these institutions are willing to lend to other counterparties. The floor improves these institutions’ ability to negotiate rates on private investments above the ON RRP rate and provides an alternative investment when more attractive rates are not available.

When Is the ON RRP Facility Used?

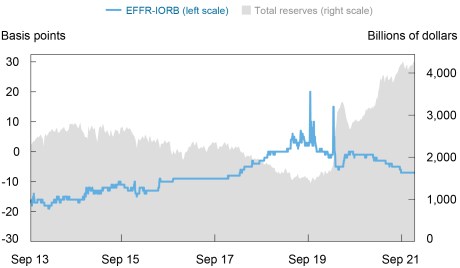

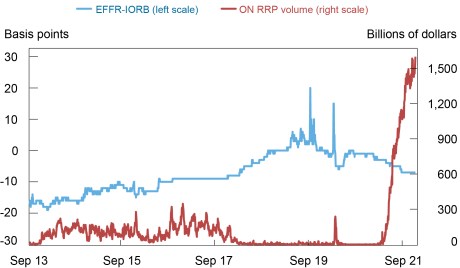

In periods when the EFFR is close to or above the IORB rate, we would not expect the ON RRP facility to see much take-up as money market participants have access to alternative investments at more favorable rates. This can be seen in the charts below. The first chart shows that as reserves steadily declined during the monetary policy normalization process, in 2018 and 2019, the EFFR increased relative to the IORB rate. The second chart shows that as the EFFR-IORB spread increased, take-up at the ON RRP facility decreased and was almost always very small, until the pandemic.

The Spread between the EFFR and the IORB Rate Tends to Decrease when Reserves Increase

Sources: Federal Reserve Economic Data (FRED); authors’ calculations.

Notes: IORB is interest on reserve balances. EFFR is effective federal funds rate. Month-end observations are dropped.

Take-up at the ON RRP Tends to Be Larger when the Spread between the EFFR and the IORB Is More Negative

Sources: Federal Reserve Economic Data (FRED); authors’ calculations.

Notes: ON RRP volume is the total value for overnight reverse repurchase agreements from September 23, 2013 to December 16, 2015, and the total value for overnight reverse repurchase agreements under the ON RRP facility from December 17, 2015 onward. EFFR is effective federal funds rate. Month-end observations are dropped.

In contrast, when reserves are plentiful and the EFFR moves closer to the bottom of the fed funds target range, the rate offered at the ON RRP facility becomes more attractive relative to alternative investments and we would expect to see an increase in take-up at the ON RRP facility. (The available supply of safe investments like Treasury bills can also influence the EFFR, as suggested in this Liberty Street Economics post.) At such times, the ON RRP facility is particularly important for the control of the EFFR. This is indeed what happened from 2013 through 2017, and in 2021 as well. As reserves have reached unprecedented levels over the last year, so has take-up at the facility.

Is the ON RRP Facility Too Large?

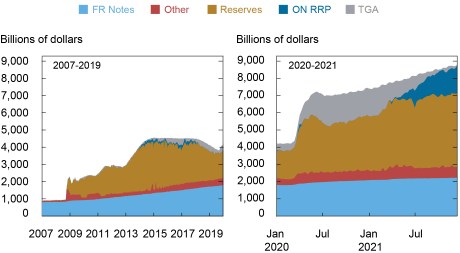

An ON RRP transaction—which is economically similar to a secured loan—does not change the size of the Fed’s balance sheet but does shift the composition of the Fed’s liabilities. For instance, when a money market fund reduces overnight deposits with a bank and directs those funds to the ON RRP facility, the increase in the ON RRP facility decreases reserve balances held by banks at the Fed. The ON RRP facility, thus, allows the Fed’s liabilities to be more broadly distributed among money market participants.

This broader distribution of Fed liabilities is particularly useful in environments where the FOMC uses asset purchases to stimulate the economy, and reserves rise as a result. Since reserves can only be held by banks, substantial growth in reserves can put pressure on bank balance sheets. Therefore, when the ON RRP facility grows it reduces these pressures by offering liabilities that can be held by a broader set of financial market participants, supporting the FOMC’s efforts to stimulate the economy through asset purchases.

The next chart shows that an increase in take-up at the ON RRP facility moderates the growth in reserve balances. Hence, when ON RRP take-up is high, as it is today, the supply of reserves is lower than it would be absent the ON RRP facility, and banks’ balance sheets are less impacted.

ON RRP Take-up Reduces the Supply of Reserves, Everything Else Equal

Sources: Federal Reserve Board (H.4.1 – Factors Affecting Reserve Balances); authors’ calculations.

How Effectively Does the ON RRP Facility Control Rates?

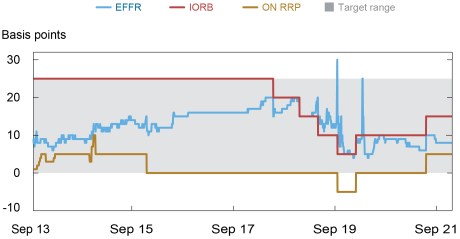

The Fed began testing ON RRPs in September 2013 and then transitioned the ON RRP facility to an implementation tool around the “lift-off” of interest rates in December 2015. Since that time, the EFFR has only printed below the target range once, at the end of 2015.

As shown in the next chart, the ON RRP facility has been very effective at providing a floor under the EFFR even as aggregate reserves have continued to grow in 2021, rising above the unprecedented level of $4 trillion in July.

ON RRP Facility Has Been an Effective Floor under the EFFR

Sources: Bloomberg L.P.; Federal Reserve Economic Data (FRED); authors’ calculations:

Notes: EFFR is effective federal funds rate. IORB is interest on reserve balances. ON RRP rate is the rate for overnight reverse repurchase agreements from September 23, 2013 to December 16, 2015, and the rate for overnight reverse repurchase agreements under the ON RRP facility from December 17, 2015 onward. Shaded area represents the Federal Open Market Committee’s target range for the federal funds rate. Month-end observations are dropped.

To Sum Up

To circle back to the beginning of the post, in the recent environment of abundant reserves, the ON RRP facility is working as expected. It is providing a floor under the fed funds rate and moderating the growth in reserve balances as the Fed continues to provide support to the U.S. economy.

Gara Afonso is an assistant vice president in the Federal Reserve Bank of New York’s Research and Statistics Group.

Lorie Logan is an executive vice present in the Bank’s Markets Group and manager of the System Open Market Account for the Federal Open Market Committee.

Antoine Martin is a senior vice president in the Bank’s Research and Statistics Group.

William Riordan is an assistant vice president in the Bank’s Markets Group.

Patricia Zobel is a vice president in the Federal Reserve Bank of New York’s Markets Group and deputy manager of the System Open Market Account for the Federal Open Market Committee.

How to cite this post:

Gara Afonso, Lorie Logan, Antoine Martin, William Riordan, and Patricia Zobel, “How the Fed’s Overnight Reverse Repo Facility Works,” Federal Reserve Bank of New York Liberty Street Economics, January 11, 2022, https://libertystreeteconomics.newyorkfed.org/2022/1/how-the-feds-overnight-reverse-repo-facility-works/.

Disclaimer

The views expressed in this post are those of the authors and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the authors.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics