Since the global financial crisis, the Federal Reserve has relied on two main rates to implement monetary policy—the rate paid on reserve balances (IORB rate) and the rate offered at the overnight reverse repo facility (ON RRP rate). In this post, we explore how these tools steer the federal funds rate within the Federal Reserve’s target range and how effective they have been at supporting rate control.

The Federal Reserve’s Monetary Policy Implementation Framework

The Federal Open Market Committee (FOMC) communicates its stance of monetary policy through a target range for the federal funds (fed funds) rate—the interest rate at which banks borrow funds overnight on an unsecured basis in the fed funds market. The Federal Reserve (the Fed) currently implements monetary policy in a regime of ample reserves, where control over the fed funds and other short-term interest rates is exerted through two administered rates set by the Fed: the IORB rate and the ON RRP rate.

The IORB is the rate that the Fed pays on the reserves that banks hold overnight in their Fed accounts, thereby setting a floor on the rates at which banks lend overnight in the fed funds market. The Fed has paid IORB since October 2008. Banks, however, are only responsible for a fraction of the lending activity in the fed funds market and other U.S. money markets. For this reason, the Fed employs a second lever: the ON RRP rate. The ON RRP facility allows eligible institutions, including money market funds, government-sponsored enterprises, and primary dealers, to invest overnight with the Fed at the ON RRP rate. This second lever, which was added to the Fed policy toolkit in 2014, works similarly to the IORB rate, establishing a floor on the rates at which these non-bank institutions are willing to lend funds overnight.

Changes in the Target Range and the Fed Funds Rate

When the FOMC announces a change in the target range for the fed funds rate, it implements this change through adjustments in the administered rates. But how much of the change passes through to the rates in the fed funds market?

To answer this question, we look at all FOMC meetings between December 2015 and June 2023 in which either the target range or the administered rates (IORB and/or ON RRP) were changed. There are twenty-seven such meetings. Since the width of the target range has remained constant, our results are the same whether we look at the top or bottom of the range. We use an event study methodology and compare the interest rates on fed funds transactions before and after the FOMC announcements.

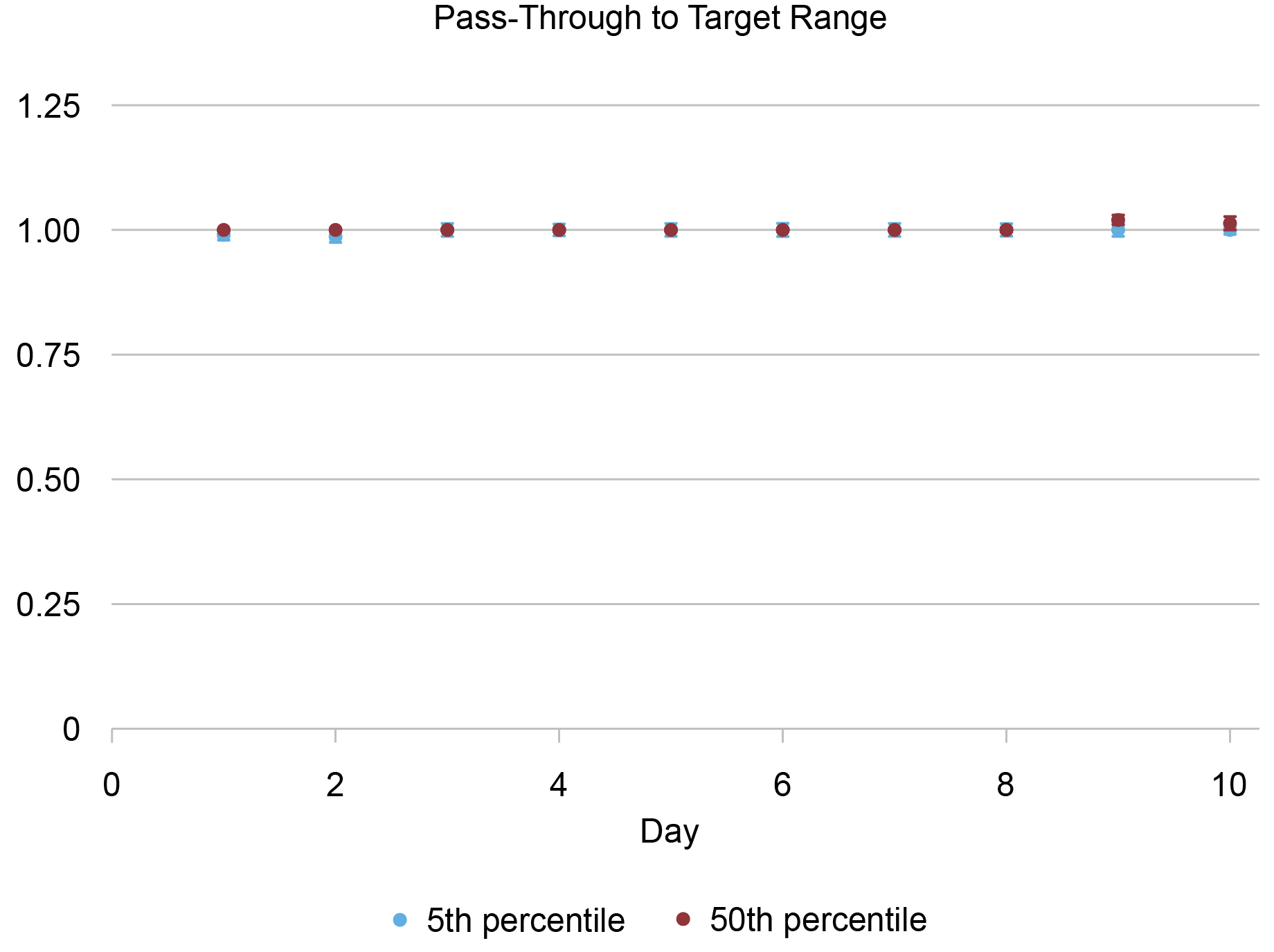

The chart below summarizes the results of a series of transaction-level quantile regressions estimating how the median (red) and the 5th percentile (blue) of the distribution of fed funds rates responded to a change in the target range. The coefficients on day 1 compare the rates prevailing one day before and one day after the meeting, on day 2, two days before and after the meeting, and so on, all the way to ten days before and after the meeting on day 10.

Changes in the Target Range Pass Through One-to-One to Fed Funds Rates

Sources: FR 2420, Report of Selected Money Market Rates, Federal Reserve Economic Data (FRED); authors’ calculations.

Note: Target range represents the Federal Open Market Committee target range for the federal funds rate.

For all time-windows, the response of the median fed funds rate to changes in the target range is very close to 1—that is, a 1 basis point increase in the target range moves the median fed funds rate by the same amount. The response is very similar for the left tail of the distribution (that is, for the 5th percentile). In addition to a pass-through close to 1, the effect is present on the first day after the FOMC communicates the change in policy stance.

Technical Adjustments

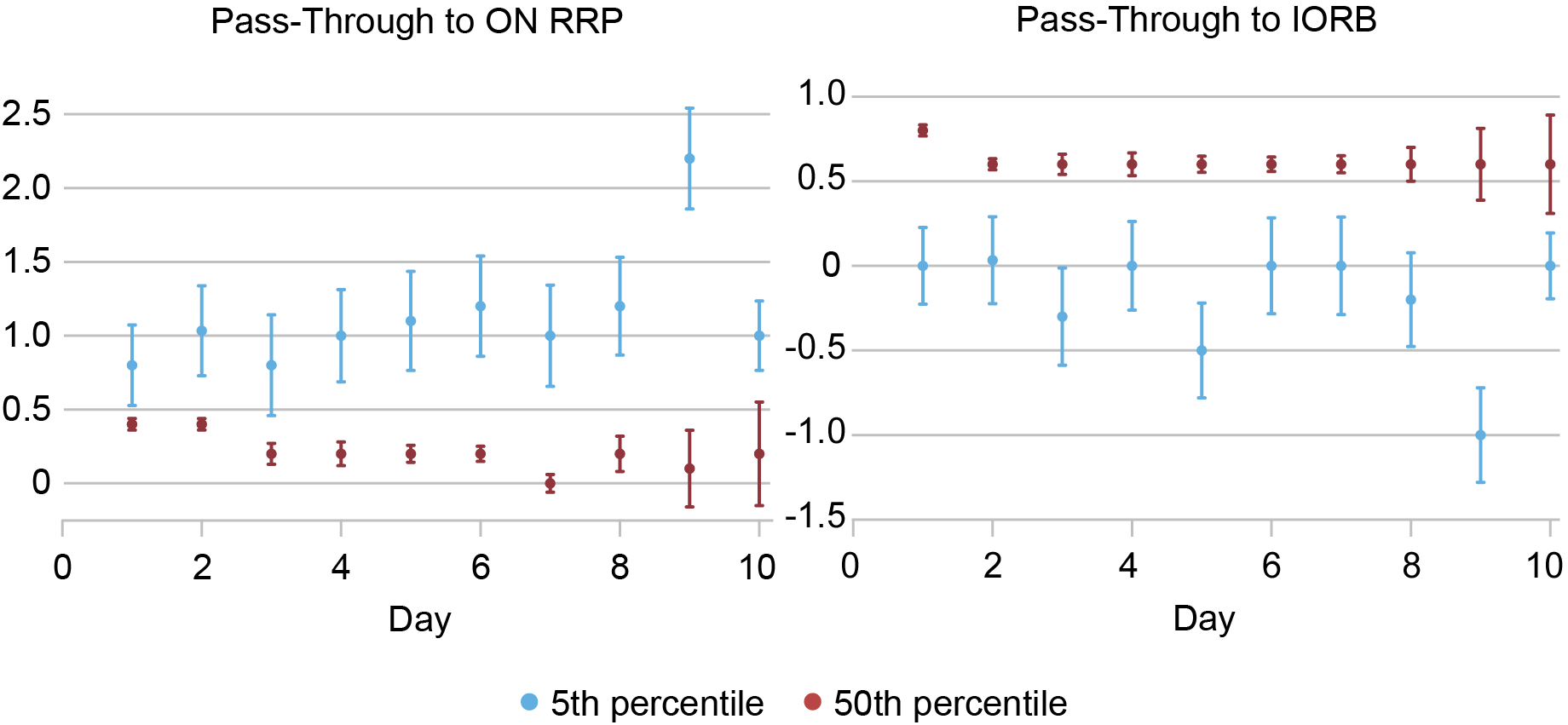

In most FOMC meetings, the IORB and ON RRP rates are adjusted by the same amount as the target range. However, in seven of the twenty-seven FOMC meetings in our sample, either the IORB or the ON RRP rate were adjusted by a different amount than the target range, a so-called technical adjustment. For instance, on May 2, 2019, the IORB rate was changed from 2.4 percent to 2.35 percent, whereas the target range and ON RRP rate were left unchanged. Because of this, we can estimate the impact of adjusting the level of these administered rates with respect to that of the target range.

The left panel of the chart below shows the estimated impact of changes in the ON RRP rate with respect to the target range on the median (red) and 5th percentile (blue) of the distribution of fed funds rates. The right panel presents similar estimates for adjustments in the IORB rate relative to the target range.

ON RRP and IORB Rates Pass Through to Fed Funds Rates Differently

Sources: FR 2420, Report of Selected Money Market Rates, Federal Reserve Economic Data (FRED); authors’ calculations.

Notes: ON RRP is the overnight reverse repo rate. IORB is the interest on reserve balances rate.

Adjusting the IORB and ON RRP rates with respect to the target range affects the distribution of rates on fed funds transactions differently. A change in the IORB rate relative to the target range mainly affects the median of the distribution, shifting it up or down by more if the IORB changes more than the range and by less otherwise.

In contrast, changes in the rate offered at the ON RRP facility with respect to the target range have a smaller impact on the median fed funds transaction while leading to a pass-through close to 1 for the 5th percentile—the left tail of the distribution. This is, indeed, consistent with the purpose of the ON RRP facility: firming the floor for transactions in the fed funds market.

Summing Up

The Fed relies on the IORB and ON RRP rates to implement monetary policy. These two administered rates have shown to be very effective at maintaining the fed funds rate within the target range. While they work through similar channels—steering the rates at which money market participants are willing to lend funds overnight—they influence the distribution of fed funds rates differently, with the IORB rate mainly affecting the median and the ON RRP rate the left tail.

Gara Afonso is the head of Banking Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Marco Cipriani is head of Money and Payments Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Gabriele La Spada is a financial research economist in Money and Payments Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

At the time this post was written, Peter Prastakos was a senior research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Gara Afonso, Marco Cipriani, Gabriele La Spada, and Peter Prastakos, “The Federal Reserve’s Two Key Rates: Similar but Not the Same?,” Federal Reserve Bank of New York Liberty Street Economics, August 14, 2023, https://libertystreeteconomics.newyorkfed.org/2023/08/the-federal-reserves-two-key-rates-similar-but-not-the-same/

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics