Editor’s Note: The chart notes for the first chart have been updated to correct errors in how we labeled the trend line colors. (March 25, 2026)

Since 2018, more than thirty states have legalized mobile sports betting, leading to more than a half trillion dollars in wagers. In our recent Staff Report, we examine how legalized sports betting affects household financial health by comparing betting activity and consumer credit outcomes between states that legalized to those that have not. We find that legalization increases spending at online sportsbooks roughly tenfold, but betting does not stop at state boundaries. Nearby areas where betting is not legal still experience roughly 15 percent the increase of counties where it is legal. At the same time, consumer financial health suffers. Our analysis finds rising delinquencies in participating states, with spillover effects across state lines. What is more, even though the share of people taking up sports betting after legalization is small (roughly 3 percent of the population), overall credit delinquency rises by about 0.3 percentage points. Our findings suggest that sports betting can have dramatic implications for household financial stability.

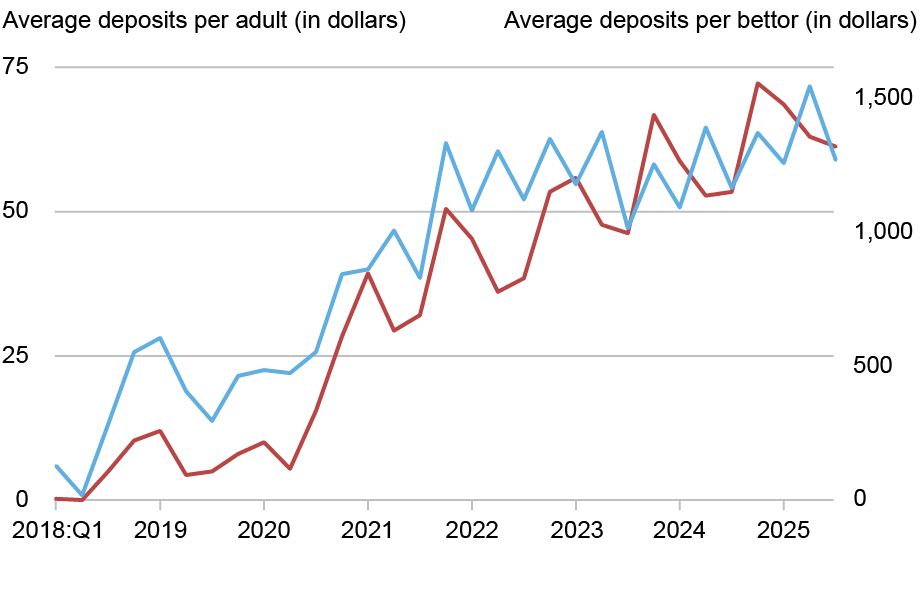

Legalization Leads to High Spending that Continues to Rise

Using anonymized transaction-level consumer spending data, we aggregate online sportsbook deposits at a county-quarter level to compare counties in legal states to those in not-legal states before and after legalization. The chart below plots two measures of average online sportsbook deposits within legal states over time. The red line (measured by the left axis), presents average deposits per adult. We see that spending grew dramatically after mid-2020, exhibits seasonal patterns consistent with the National Football League season, and continues to grow through the end of 2025.

The blue line (measured on the right axis) shows the total deposits divided by the number of individuals with at least one online sportsbook deposit each quarter. In contrast to average deposits in the population, average deposits per bettor have leveled since 2022. We conclude that long-run growth in total betting is driven less by rising deposits among existing bettors and more by broader participation and continued market expansion.

Average Deposits at Sportsbooks Rise Steeply After Mid-2020

Notes: The chart plots quarterly average deposits at sportsbooks per adult (left axis, red) and per bettor (right axis, blue) in counties with legal mobile sports betting. Both series are unweighted averages across all counties in states where mobile betting is legal in that quarter.

Betting Across Borders

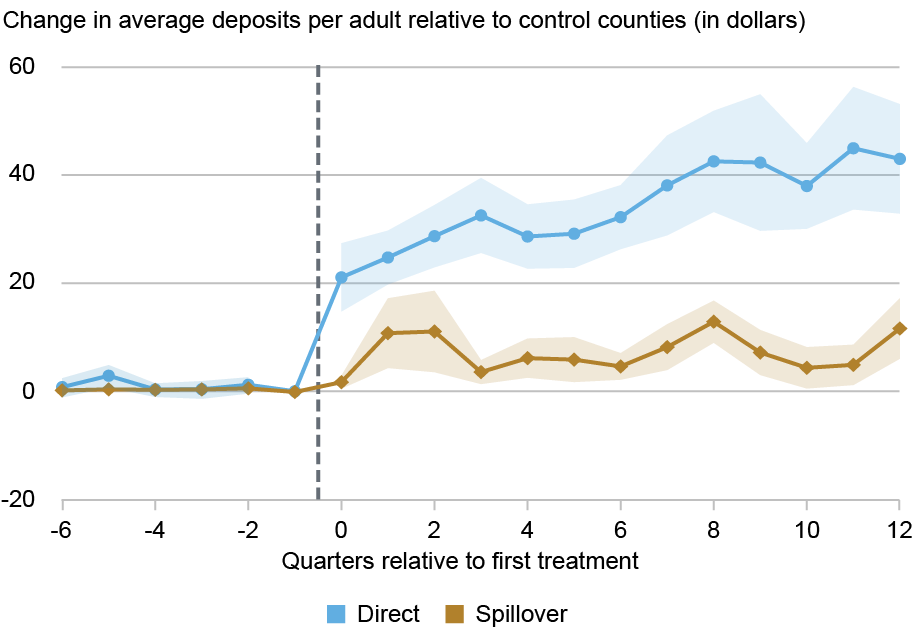

An interesting wrinkle to sports betting access is that potential bettors do not have to be residents of a legal state to place a wager. Since they only need to be physically present in a legal state at the time they make a bet, those living near legal states have relatively easy access to legal sports betting. To account for spillovers across borders in our analysis, we split our sample into three mutually exclusive groups in each quarter: a direct treatment group of counties within a legal state, a spillover group of counties near a legal state but in still-illegal states (within fifteen miles), and a control group of counties farther away from any legal states (at least sixty miles from a legal state). We then compare the evolution of online betting in each quarter relative to the first quarter of legal access (own legalization for the legal counties or nearby legalization for the spillover counties).

The chart below plots the estimated effect of legalization on average deposits at sportsbooks separately for the direct effect and the spillover effect in each quarter relative to the first quarter of legal access. We find a large increase in spending within state lines (blue line) with a similarly sharp but smaller increase in nearby spillover counties (gold line). On average, online betting deposits per adult increase by roughly $30 per quarter in the first few quarters after legalization and grow to around $40 after three years. Most striking is the magnitude of spillovers: for nearby counties that are not legal, the impact is roughly 15 percent the size of the direct effect, representing significant spending coming from across state lines.

Sportsbook Deposits Grow Dramatically After Legalization in Legal Counties and in Nearby Illegal Counties

Notes: The chart plots estimates (in circles and squares) and 95 percent confidence intervals (in shaded regions) for the change in average sportsbook deposits per adult in quarters relative to the first quarter of legal access. Legal access is defined as own-state legalization for counties in legal states (blue line) and nearby legalization for counties in spillover states (gold line). The full empirical specification can be found in Goss and Mangrum (2026).

Implications for Consumer Credit

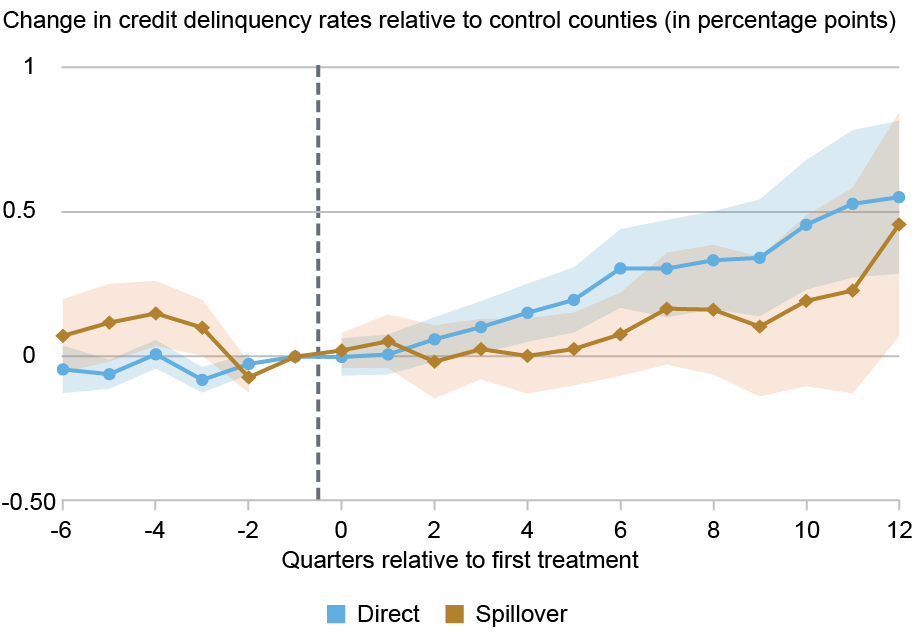

Next, we examine credit delinquencies using the New York Fed Consumer Credit Panel (CCP), a nationally representative 5 percent sample of anonymized Equifax credit reports, with the same geographic approach as above. The chart below shows the impact of legalization on the share of the county population with any account ninety or more days past due, with the blue line showing the direct effect and the gold line showing the spillover effect. Following legalization, delinquency rose steadily in legal counties and surpassed half a percentage point three years after legalization, representing a noticeable deterioration in repayment performance from a baseline of 10.7 percent. Spillover counties follow a similar pattern with a smaller magnitude increase in delinquencies, suggesting that, as with betting activity, the financial consequences extend across state lines. In our Staff Report, we show that the overall increase in delinquency is driven by borrowers under the age of 40. Following legalization, the share of under-40 borrowers who are delinquent rises by 1.02 percentage points for credit cards and 0.55 percentage point for auto loans.

Our consumer credit analysis explores the overall impact of sports betting on the full population without differentiating between those that gamble and those that do not. However, the spending analysis shows that only around 3 percent of the population newly takes up sports betting after legalization. If we instead focus on only the 3 percent of people who newly take up sports betting after legalization, the implied increase in delinquency rate conditional on take-up is 10 percentage points, roughly a doubling from the baseline rate.

Credit Delinquencies Increase Steadily After Sports Betting Legalization

Notes: The chart plots estimates (in circles and squares) and 95 percent confidence intervals (in shaded regions) for the change in credit delinquency rates in quarters relative to the first quarter of legal access. Legal access is defined as own-state legalization for counties in legal states (blue line) and nearby legalization for counties in spillover states (gold line). The full empirical specification can be found in Goss and Mangrum (2026).

Implications for Not-Yet-Legal States

In our Staff Report, we find that following the legalization of sports betting in a state, credit delinquencies increase, driven by those under 40 years old. In addition, betting activity, and the resulting consumer credit distress, do not stop at state boundaries. Some who live in not-yet-legal states near legal states travel across state lines to wager and delinquencies rise in these not-legal areas as well. In legal states, tax revenue from sports betting can help offset some of the negative impacts of legalized sports betting (states collected nearly $3 billion in such tax revenue in 2024 alone), but states that are not legal themselves bear negative consequences of sports betting without the tax revenue to offset these costs. As we show in the Staff Report, the negative consequences without compensating tax revenue may create incentives for states to legalize, particularly those with population centers near legal states.

Jacob Goss is a former research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group and a current graduate student at the University of Wisconsin—Madison.

Daniel Mangrum is a research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Jacob Goss and Daniel Mangrum, “Sports Betting Is Everywhere, Especially on Credit Reports,” Federal Reserve Bank of New York Liberty Street Economics, March 25, 2026, https://doi.org/10.59576/lse.20260325

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics