6 posts on "climate risk"

October 7, 2024

What Do Climate Risk Indices Measure?

As interest in understanding the economic impacts of climate change grows, the climate economics and finance literature has developed a number of indices to quantify climate risks. Various approaches have been employed, utilizing firm-level emissions data, financial market data (from equity and derivatives markets), or textual data. Focusing on the latter approach, we conduct descriptive analyses of six text-based climate risk indices from published or well-cited papers. In this blog post, we highlight the differences and commonalities across these indices.

Posted at 7:00 am in Climate Change | Permalink

November 20, 2023

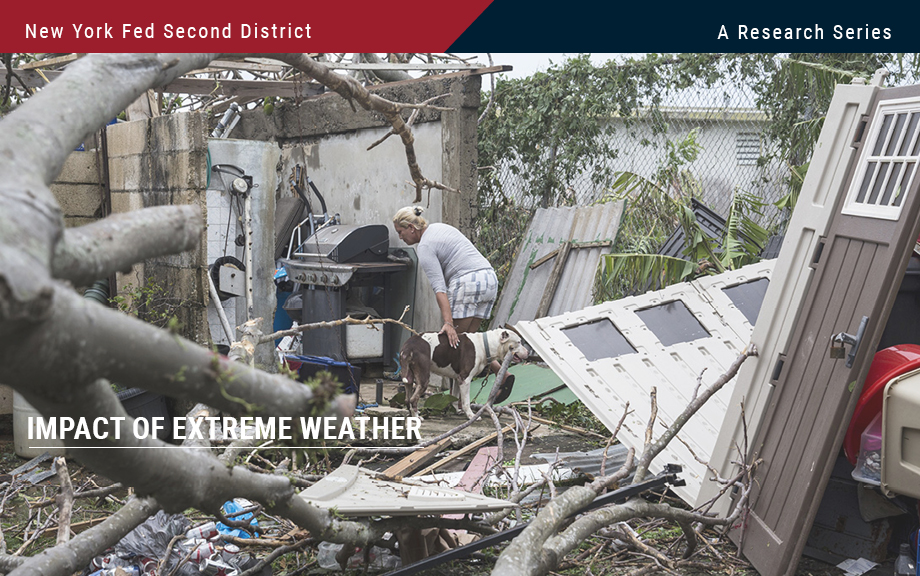

Banks versus Hurricanes

The impacts of hurricanes analyzed in the previous post in this series may be far-reaching in the Second District. In a new Staff Report, we study how banks in Puerto Rico fared after Hurricane Maria struck the island on September 17, 2017. Maria makes a worst case in some respects because the economy and banks there were vulnerable beforehand, and because Maria struck just two weeks after Hurricane Irma flooded the island. Despite the immense destruction and disruption Maria caused, we find that the island’s economy and banks recovered surprisingly quickly. We discuss the various protections—including homeowners’ insurance, federal aid, and mortgage guarantees—that helped buttress the island’s economy and banks.

November 17, 2023

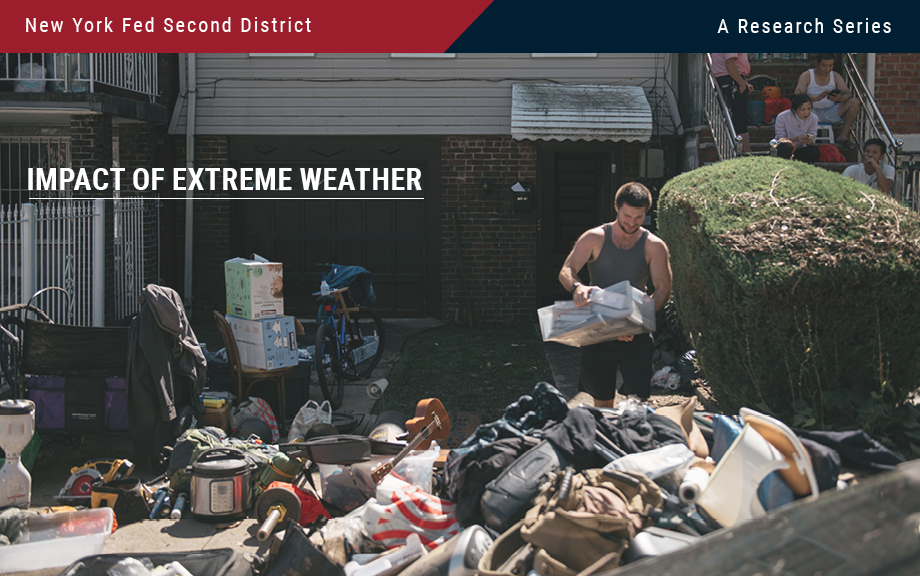

Flood‑Prone Basement Housing in New York City and the Impact on Low‑ and Moderate‑Income Renters

Hurricane Ida, which struck New York in early September 2021, exposed the region’s vulnerability to extreme rainfall and inland flooding. The storm created massive damage to the housing stock, particularly low-lying units. This post measures the storm’s impact on basement housing stock and, following the focus on more-at-risk populations from the two previous entries in this series, analyzes the attendant impact on low-income and immigrant populations. We find that basements in select census tracts are at high risk of flooding, affecting an estimated 10 percent of low-income and immigrant New Yorkers.

April 20, 2023

CRISK: Measuring the Climate Risk Exposure of the Financial System

A growing number of climate-related policies have been adopted globally in the past thirty years (see chart below). The risk to economic activity from changes in policies in response to climate risks, such as carbon taxes and green subsidies, is often referred to as transition risk. Transition risk can adversely affect the real economy through […]

Posted at 7:00 am in Climate Change, Financial Institutions, Financial Markets, Systemic Risk | Permalink

September 6, 2022

Small Business Recovery after Natural Disasters

The first post of this series found that small businesses owned by people of color are particularly vulnerable to natural disasters. In this post, we focus on the aftermath of disasters, and examine disparities in the ability of firms to reopen their businesses and access disaster relief. Our results indicate that Black-owned firms are more likely to remain closed for longer periods and face greater difficulties in obtaining the immediate relief needed to cope with a natural disaster.

How Do Natural Disasters Affect U.S. Small Business Owners?

Recent research has linked climate change and socioeconomic inequality (see here, here, and here). But what are the effects of climate change on small businesses, particularly those owned by people of color, which tend to be more resource-constrained and less resilient? In a series of two posts, we use the Federal Reserve’s Small Business Credit Survey (SBCS) to document small businesses’ experiences with natural disasters and how these experiences differ based on the race and ethnicity of business owners. This first post shows that small firms owned by people of color sustain losses from natural disasters at a disproportionately higher rate than other small businesses, and that these losses make up a larger portion of their total revenues. In the second post, we explore the ability of small firms to reopen and to obtain disaster relief funding in the aftermath of climate events.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics