5 posts on "deposit insurance"

November 25, 2024

Why Do Banks Fail? Bank Runs Versus Solvency

Evidence from a 160-year-long panel of U.S. banks suggests that the ultimate cause of bank failures and banking crises is almost always a deterioration of bank fundamentals that leads to insolvency. As described in our previous post, bank failures—including those that involve bank runs—are typically preceded by a slow deterioration of bank fundamentals and are hence remarkably predictable. In this final post of our three-part series, we relate the findings discussed previously to theories of bank failures, and we discuss the policy implications of our findings.

November 22, 2024

Why Do Banks Fail? The Predictability of Bank Failures

Can bank failures be predicted before they happen? In a previous post, we established three facts about failing banks that indicated that failing banks experience deteriorating fundamentals many years ahead of their failure and across a broad range of institutional settings. In this post, we document that bank failures are remarkably predictable based on simple accounting metrics from publicly available financial statements that measure a bank’s insolvency risk and funding vulnerabilities.

November 21, 2024

Why Do Banks Fail? Three Facts About Failing Banks

Why do banks fail? In a new working paper, we study more than 5,000 bank failures in the U.S. from 1865 to the present to understand whether failures are primarily caused by bank runs or by deteriorating solvency. In this first of three posts, we document that failing banks are characterized by rising asset losses, deteriorating solvency, and an increasing reliance on expensive noncore funding. Further, we find that problems in failing banks are often the consequence of rapid asset growth in the preceding decade.

May 12, 2023

Banks Runs and Information

The collapse of Silicon Valley Bank (SVB) and Signature Bank (SB) has raised questions about the fragility of the banking system. One striking aspect of these bank failures is how the runs that preceded them reflect risks and trade-offs that bankers and regulators have grappled with for many years. In this post, we highlight how these banks, with their concentrated and uninsured deposit bases, look quite similar to the small rural banks of the 1930s, before the creation of deposit insurance. We argue that, as with those small banks in the early 1930s, managing the information around SVB and SB’s balance sheets is of first-order importance.

February 17, 2022

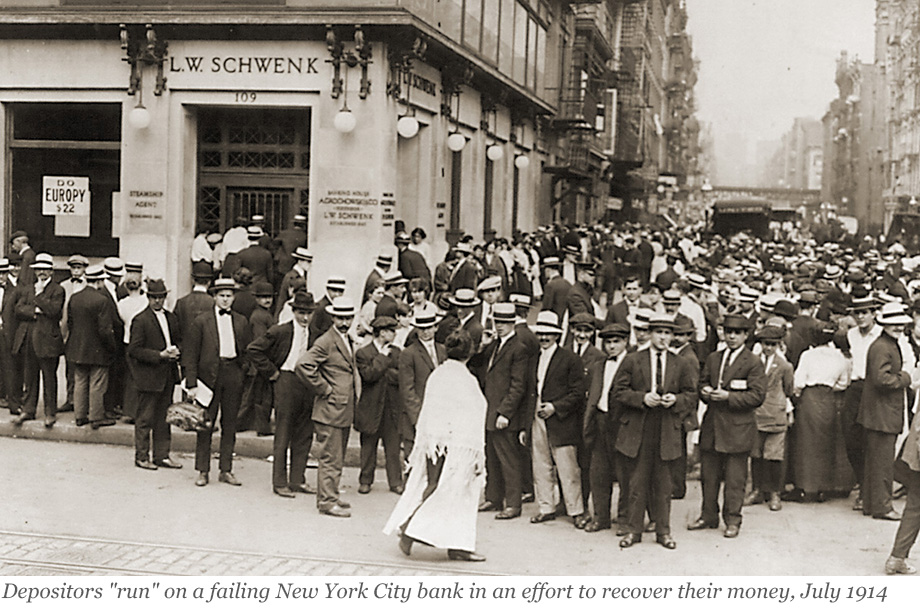

How (Un‑)Informed Are Depositors in a Banking Panic? A Lesson from History

How informed or uninformed are bank depositors in a banking crisis? Can depositors anticipate which banks will fail? Understanding the behavior of depositors in financial crises is key to evaluating the policy measures, such as deposit insurance, designed to prevent them. But this is difficult in modern settings. The fact that bank runs are rare and deposit insurance universal implies that it is rare to be able to observe how depositors would behave in absence of the policy. Hence, as empiricists, we are lacking the counterfactual of depositor behavior during a run that is undistorted by the policy. In this blog post and the staff report on which it is based, we go back in history and study a bank run that took place in Germany in 1931 in the absence of deposit insurance for insight.

Posted at 7:00 am in Banks, Financial Institutions, Financial Intermediation, Panic, Systemic Risk | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics