9 posts on "Haoyang Liu"

April 5, 2021

Do People View Housing as a Good Investment and Why?

Housing represents the largest asset owned by most households and is a major means of wealth accumulation, particularly for the middle class. Yet there is limited understanding of how households view housing as an investment relative to financial assets, in part because of their differences beyond the usual risk and return trade-off. Housing offers households an accessible source of leverage and a commitment device for saving through an amortization schedule. For an owner-occupied residence, it also provides stability and hedges for rising housing costs. On the other hand, housing is much less liquid than financial assets and it also requires more time to manage. In this post, we use data from our just released SCE Housing Survey to answer several questions about how households view this choice: Do households view housing as a good investment choice in comparison to financial assets, such as stocks? Are there cross-sectional differences in preferences for housing as an investment? What are the factors households consider when making an investment choice between housing and financial assets?

March 24, 2021

Did Dealers Fail to Make Markets during the Pandemic?

Sarkar and coauthors liquidity provision by dealers in several important financial markets during the COVID-19 pandemic: how much was provided, possible causes of any shortfalls, and the effects of the Federal Reserve’s actions to support the economy.

October 7, 2020

Are People Overconfident about Avoiding COVID‑19?

More than six months into the COVID-19 outbreak, the number of new cases in the United States remains at an elevated level. One potential reason is a lack of preventative efforts either because people believe that the pandemic will be short-lived or because they underestimate their own chance of infection despite it being a public risk. To understand these possibilities, we elicit people’s perceptions of COVID-19 as a public health concern and a personal concern over the next three months to the following three years within the May administration of the Survey of Consumer Expectations (SCE). This post reports results from these survey questions.

July 17, 2020

MBS Market Dysfunctions in the Time of COVID‑19

Haoyang Liu, Asani Sarkar, and coauthors study a particular aspect of MBS market disruptions by showing how a long-standing relationship between cash and forward markets broke down, in spite of dealers increasing the provision of liquidity. The analysis also highlights an innovative response by the Federal Reserve that seemed to have helped to normalize market functioning.

Posted at 7:00 am in Financial Institutions, Financial Markets, Liquidity, Pandemic | Permalink | Comments (2)

July 8, 2020

Who Has Been Evicted and Why?

More than two million American households are at risk of eviction every year. Evictions have been found to cause prolonged homelessness, worsened health conditions, and lack of credit access. During the COVID-19 outbreak, governments at all levels implemented eviction moratoriums to keep renters in their homes. As these moratoriums and enhanced income supports for unemployed workers come to an end, the possibility of a wave of evictions in the second half of the year is drawing increased attention. Despite the importance of evictions and related policies, very few economic studies have been done on this topic. With the exception of the Milwaukee Area Renters Study, evictions are rarely measured in economic surveys. To fill this gap, we conducted a novel national survey on evictions within the Housing Module of the Survey of Consumer Expectations (SCE) in 2019 and 2020. This post describes our findings.

July 7, 2020

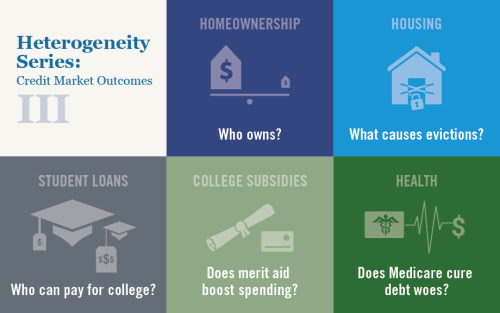

Introduction to Heterogeneity Series III: Credit Market Outcomes

Following up series on heterogeneity and inequality broadly and in labor market outcomes specifically, we turn our focus to further documenting heterogeneity in credit market outcomes, looking at disparities in home ownership rates, varying exposure to evictions, differing gains from tuition support and Medicare programs, and more.

May 20, 2020

The Paycheck Protection Program Liquidity Facility (PPPLF)

On April 9, 2020, the Federal Reserve announced that it would take additional actions to provide up to $2.3 trillion in loans to support the economy in response to the COVID-19 crisis. Among the measures taken was the establishment of a new facility intended to facilitate lending to small businesses via the Small Business Administration’s Paycheck Protection Program (PPP). Under the Paycheck Protection Program Liquidity Facility (PPPLF), Federal Reserve Banks are authorized to supply liquidity to financial institutions participating in the PPP in the form of term financing on a non-recourse basis while taking PPP loans as collateral. The facility was launched April 16, 2020. As of May 7, it had issued over $29 billion in loans (see the H.4.1 Statistical Release). This post lays out the background for the PPPLF and discusses its intended effects.

February 26, 2020

Did Subprime Borrowers Drive the Housing Boom?

The role of subprime mortgage lending in the U.S. housing boom of the 2000s is hotly debated in academic literature. One prevailing narrative ascribes the unprecedented home price growth during the mid-2000s to an expansion in mortgage lending to subprime borrowers. This post, based on our recent working paper, “Villains or Scapegoats? The Role of Subprime Borrowers in Driving the U.S. Housing Boom,” presents evidence that is inconsistent with conventional wisdom. In particular, we show that the housing boom and the subprime boom occurred in different places.

Posted at 7:00 am in Banks, Credit, Crisis, Household Finance, Housing, Recession | Permalink | Comments (8)

October 16, 2019

Optimists and Pessimists in the Housing Market

Haoyang Liu and Christopher Palmer examine how perceptions of past housing prices may shape predictions for the future, and investigate whether these tendencies shape participation in the housing market.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics