6 posts on "silicon valley bank"

December 20, 2024

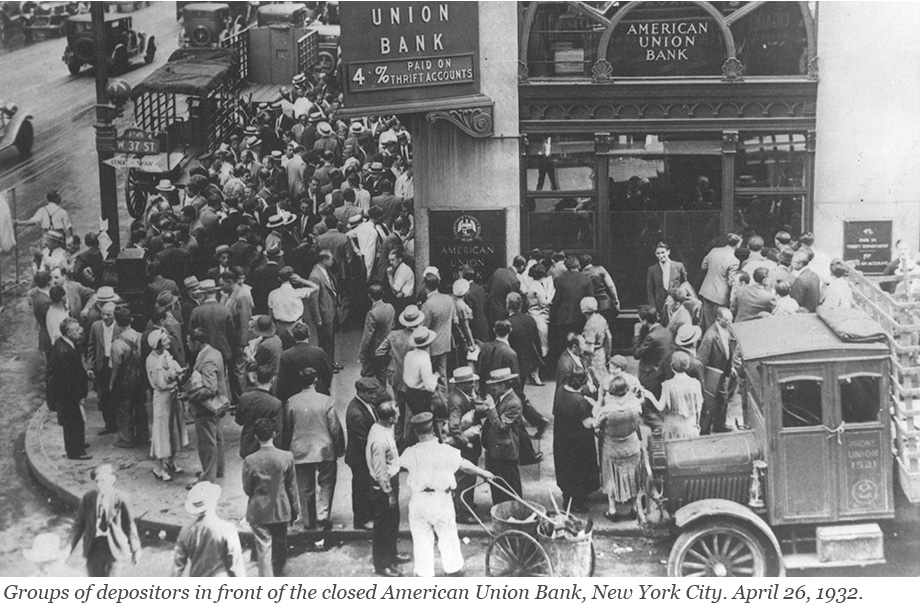

Anatomy of the Bank Runs in March 2023

Runs have plagued the banking system for centuries and returned to prominence with the bank failures in early 2023. In a traditional run—such as depicted in classic photos from the Great Depression—depositors line up in front of a bank to withdraw their cash. This is not how modern bank runs occur: today, depositors move money from a risky to a safe bank through electronic payment systems. In a recently published staff report, we use data on wholesale and retail payments to understand the bank run of March 2023. Which banks were run on? How were they different from other banks? And how did they respond to the run?

Posted at 6:30 am in Banks, Crisis, Financial Institutions, Lender of Last Resort, Panic | Permalink | Comments (1)

December 3, 2024

Documenting Lender Specialization

Robust banks are a cornerstone of a healthy financial system. To ensure their stability, it is desirable for banks to hold a diverse portfolio of loans originating from various borrowers and sectors so that idiosyncratic shocks to any one borrower or fluctuations in a particular sector would be unlikely to cause the entire bank to go under. With this long-held wisdom in mind, how diversified are banks in reality?

April 10, 2024

A Retrospective on the Life Insurance Sector after the Failure of Silicon Valley Bank

Following the Silicon Valley Bank collapse, the stock prices of U.S banks fell amid concerns about the exposure of the banking sector to interest rate risk. Thus, between March 8 and March 15, 2023, the S&P 500 Bank index dropped 12.8 percent relative to S&P 500 returns (see right panel of the chart below). The stock prices of insurance companies tumbled as well, with the S&P 500 Insurance index losing 6.4 percent relative to S&P 500 returns over the same time interval (see the center panel below). Yet, insurance companies’ direct exposure to the three failed banks (Silicon Valley Bank, Silvergate, and Signature Bank) through debt and equity was modest. In this post, we examine the possible factors behind the reaction of insurance investors to the failure of Silicon Valley Bank.

Posted at 7:00 am in Financial Institutions | Permalink

November 28, 2023

Bond Funds in the Aftermath of SVB’s Collapse

March 2023 will rightfully be remembered as a period of major turmoil for the U.S. banking industry. In this post, we go beyond banks to analyze how fixed-income, open-end funds (bond funds) fared in the days after the start of the banking crisis. We find that bond funds experienced net outflows each day for almost three weeks after the run on Silicon Valley Bank (SVB), and that these outflows were experienced diffusely across the entire segment. Our preliminary evidence suggests that the outflows from bond funds may have been an unintended consequence of the exceptional measures taken to strengthen the balance sheet of banks during this time.

May 12, 2023

Banks Runs and Information

The collapse of Silicon Valley Bank (SVB) and Signature Bank (SB) has raised questions about the fragility of the banking system. One striking aspect of these bank failures is how the runs that preceded them reflect risks and trade-offs that bankers and regulators have grappled with for many years. In this post, we highlight how these banks, with their concentrated and uninsured deposit bases, look quite similar to the small rural banks of the 1930s, before the creation of deposit insurance. We argue that, as with those small banks in the early 1930s, managing the information around SVB and SB’s balance sheets is of first-order importance.

May 11, 2023

Bank Funding during the Current Monetary Policy Tightening Cycle

Recent events have highlighted the importance of understanding the distribution and composition of funding across banks. Market participants have been paying particular attention to the overall decline of deposit funding in the U.S. banking system as well as the reallocation of deposits within the banking sector. In this post, we describe changes in bank funding structure since the onset of monetary policy tightening, with a particular focus on developments through March 2023.

Posted at 7:00 am in Bank Capital, Banks, Federal Reserve, Financial Institutions | Permalink | Comments (1)

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics