Households frequently use stimulus checks to pay down existing debt. In this post, we discuss the empirical evidence on this marginal propensity to repay debt (MPRD), and we present new findings using the Survey of Consumer Expectations. We find that households with low net wealth-to-income ratios were more prone to use transfers from the CARES Act of March 2020 to pay down debt. We then show that standard models of consumption-saving behavior can be made consistent with these empirical findings if borrowers’ interest rates rise with debt. Our model suggests that fiscal policy may face a trade-off between increasing aggregate consumption today and assisting those with the largest debt balances.

How Have Households Used Their Stimulus Payments?

We study the CARES Act, a large stimulus package passed by the U.S. federal government on March 27, 2020. As part of this package, all qualifying adults received a one-time transfer of up to $1,200, with $500 per additional child. In order to document how households used these payments, we draw on a special module fielded as part of New York Fed’s Survey of Consumer Expectations (SCE). In this module, respondents who had already received their CARES Act payments reported whether they used them to spend or donate, save or invest, or pay down debts.

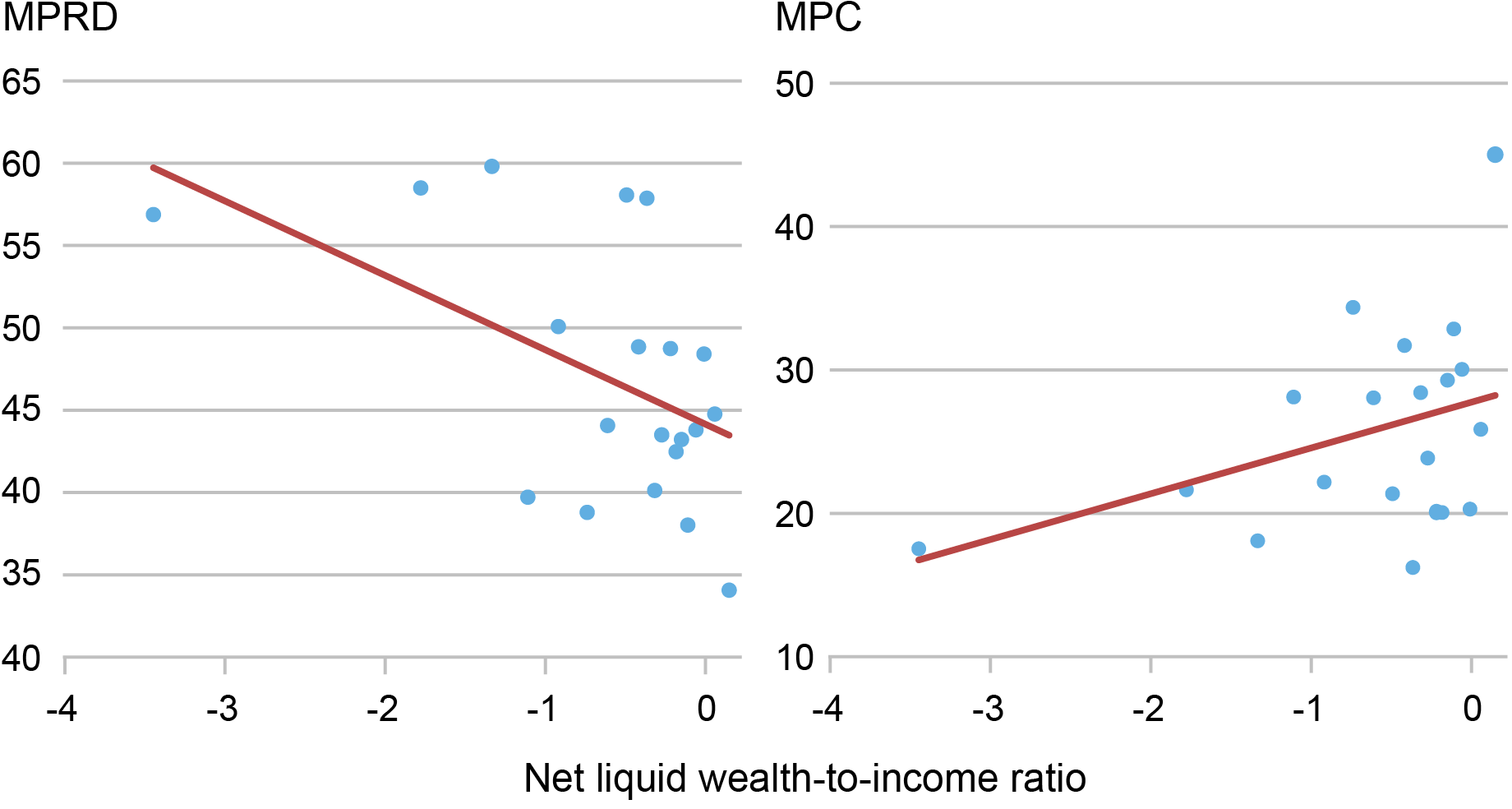

Using these responses, we define marginal propensity to consume (MPC) as the share of the stimulus payment a household spent, marginal propensity to save (MPS) as the share a household saved, and marginal propensity to repay debt (MPRD) as the share used to pay down their debt. With these measures we document three main facts. First, households used one third of their transfers to pay down debt. This is higher than the average marginal propensity to consume (MPC), which usually takes center stage. Other studies (see Coibion, Gorodnichenko, and Weber (2020) and Sahm, Shapiro, and Slemrod (2010)) have also found large MPRDs, suggesting that using fiscal transfers to pay down debt is not special to the COVID-19 pandemic. Second, households with low net liquid wealth-to-income ratios are more likely to pay down debt and more likely to adjust their net wealth positions. Third, and relatedly, households with lower net liquid wealth-to-income ratios have lower MPCs. We show these two latter facts in the chart below. Note that we define net liquid wealth as the sum of liquid assets minus non-housing debt. For income, we use annual household income.

MPRDs Decline While MPCs Increase with Net Liquid Wealth-to-Income Ratio

Source: Authors’ calculations using the June special module of the New York Fed’s Survey of Consumer Expectations.

Notes: slope= -4.507** (left panel), slope=3.186** (right panel); * p<0.1, ** p<0.05, *** p<0.01.

The MPRD and the Effects of Fiscal Transfers

The household behavior we document can be explained by a model that incorporates a simple observation: Borrowing interest rates increase with household debt. For example, borrowers with higher debts often have, other things equal, lower credit scores, leading to higher interest rates. This induces households to use at least part of their check to pay down debt, in order to reduce their debt service payments and, thus, sustain higher consumption in the future. In our working paper, we formally describe this mechanism in detail. In addition, we provide evidence for the quantitative shape of debt price schedules that are needed for the model to be consistent with our empirical findings. It turns out that the resulting borrowing interest rates are also consistent with what would arise from models with endogenous default and delinquency motives.

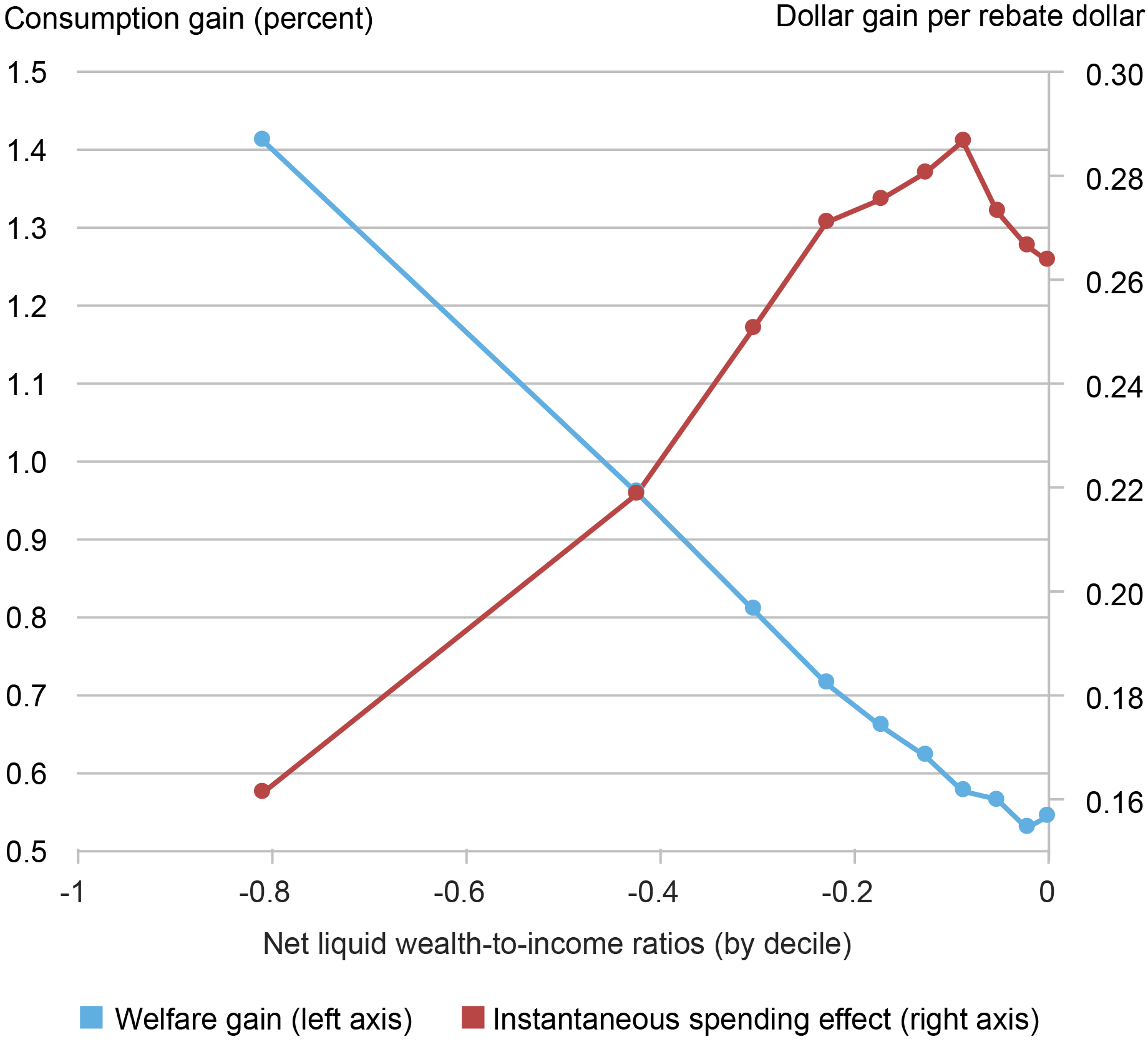

We find that accounting for debt-sensitive interest rates alters the effects of fiscal policy. We perform three exercises to show this. First, when interest rates are debt sensitive, stimulus and insurance motives move in opposite directions across households. Here, the insurance motive refers to households’ savings to protect their spending ability when income falls. We illustrate this in the chart below, which presents the two effects of a fiscal transfer across the net wealth-to-income distribution from our model.

Stimulus and Insurance Motives of Fiscal Policy Move in Opposite Directions across Households

Source: Authors’ calculations using model simulations.

In the chart, we group borrowers in the model by ten deciles of their net liquid wealth-to-income ratio on the horizontal axis. Therefore, each dot contains the same share of households. For each quantile, we compute the average share of each rebate dollar that households spend upon receiving the check, in red, and the lifetime welfare gain from receiving the transfer, in blue. The chart underscores a clear inverse relationship between these quantities: households that have the biggest consumption gain from the transfer today will have the lowest welfare gain over their lifetimes.

This result implies that policymakers may face a trade-off when designing fiscal policy, depending on whether they wish to maximize aggregate spending or aggregate welfare. This trade-off materializes also when comparing short-run and long-run fiscal multipliers: debt-sensitive interest rates lower upon-impact consumption responses of the poorest households, while making these consumption responses more persistent over time. Conversely, they increase MPCs of households with little debt, but make their spending responses less persistent.

In our second exercise, we examine how these two effects aggregate up in the economy and unfold over time. We show that, in the medium term, an increasing debt-price schedule amplifies the consumption effects of fiscal policy. For every dollar of fiscal transfer disbursed to households, a reduction in debt service payments leads to an 8 percentage point additional spending effect after seven years.

Finally, we compute the average welfare and consumption gains stemming from the Economic Impact Payments by allocating the payments in the model as they had been allocated in the CARES Act in 2020. In our calibrated model, welfare rises by 0.52 percent, while 21 cents per rebate dollar are spent within the first quarter, which is, all else equal, about 1.5 percent of nominal aggregate consumption at the time of the CARES Act.

In conclusion, we have provided new empirical evidence for an underappreciated fact: Most households, especially those with lowest net liquid wealth, use fiscal transfers to pay down debt. By doing so, indebted households face better interest rates and thus can consume more in the future. This underscores an additional insurance motive for what have often been too narrowly tagged “stimulus’’ checks. Stimulus and insurance motives, however, are not well aligned across households. As such, policymakers may maximize either immediate spending or longer–run welfare gains by targeting different sets of households.

Gizem Kosar is a research economist in Consumer Behavior Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Davide Melcangi is a research economist in Labor and Product Market Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Laura Pilossoph is an assistant professor of economics at Duke University.

David Wiczer is a research economist and associate adviser at the Federal Reserve Bank of Atlanta.

How to cite this post:

Gizem Koşar, Davide Melcangi, Laura Pilossoph, and David Wiczer, “Not Just “Stimulus” Checks: The Marginal Propensity to Repay Debt,” Federal Reserve Bank of New York Liberty Street Economics, June 27, 2023, https://libertystreeteconomics.newyorkfed.org/2023/06/not-just-stimulus-checks-the-marginal-propensity-to-repay-debt/

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics