7 posts from "November 2024"

November 25, 2024

Why Do Banks Fail? Bank Runs Versus Solvency

Evidence from a 160-year-long panel of U.S. banks suggests that the ultimate cause of bank failures and banking crises is almost always a deterioration of bank fundamentals that leads to insolvency. As described in our previous post, bank failures—including those that involve bank runs—are typically preceded by a slow deterioration of bank fundamentals and are hence remarkably predictable. In this final post of our three-part series, we relate the findings discussed previously to theories of bank failures, and we discuss the policy implications of our findings.

November 22, 2024

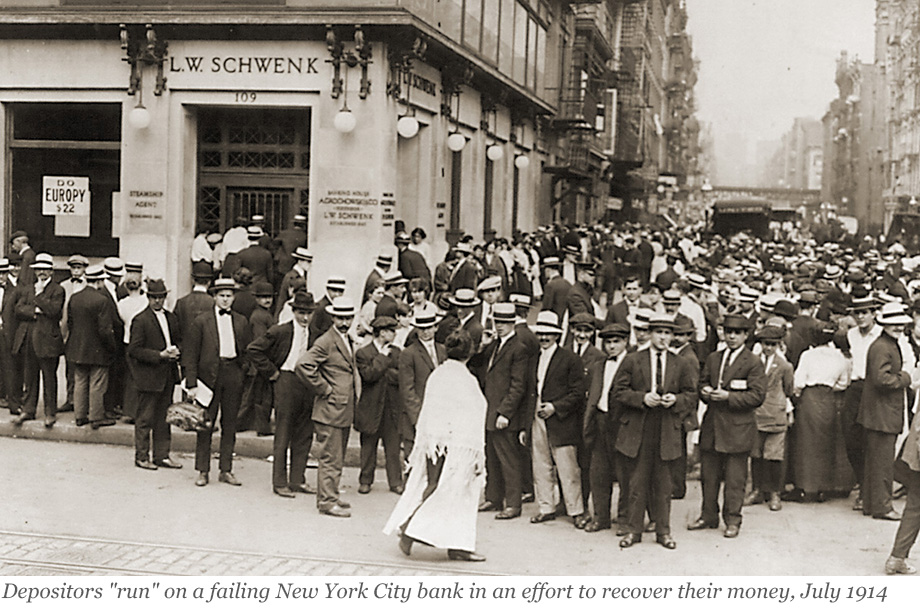

Why Do Banks Fail? The Predictability of Bank Failures

Can bank failures be predicted before they happen? In a previous post, we established three facts about failing banks that indicated that failing banks experience deteriorating fundamentals many years ahead of their failure and across a broad range of institutional settings. In this post, we document that bank failures are remarkably predictable based on simple accounting metrics from publicly available financial statements that measure a bank’s insolvency risk and funding vulnerabilities.

November 21, 2024

Why Do Banks Fail? Three Facts About Failing Banks

Why do banks fail? In a new working paper, we study more than 5,000 bank failures in the U.S. from 1865 to the present to understand whether failures are primarily caused by bank runs or by deteriorating solvency. In this first of three posts, we document that failing banks are characterized by rising asset losses, deteriorating solvency, and an increasing reliance on expensive noncore funding. Further, we find that problems in failing banks are often the consequence of rapid asset growth in the preceding decade.

November 15, 2024

To Whom It May Concern: Demographic Differences in Letters of Recommendation

Letters of recommendation from faculty advisors play a critical role in the job market for Ph.D. economists. At their best, they can convey important qualitative information about a candidate, including the candidate’s potential to generate impactful research. But at their worst, these letters offer a subjective view of the candidate that can be susceptible to conscious or unconscious bias. There may also be similarity or affinity bias, a particularly difficult issue for the economics profession, where most faculty members are white men. In this post, we draw on our recent working paper to describe how recommendation letters differ by the gender, race, or ethnicity of the job candidate and how these differences are related to early career outcomes.

November 14, 2024

Why Investment‑Led Growth Lowers Chinese Living Standards

Rapid GDP growth, due in part to high rates of investment and capital accumulation, has raised China out of poverty and into middle-income status. But progress in raising living standards has lagged, as a side-effect of policies favoring investment over consumption. At present, consumption per capita stands some 40 percent below what might be expected given China’s income level. We quantify China’s consumption prospects via the lens of the neoclassical growth model. We find that shifting the country’s production mix toward consumption would raise both current and future living standards, with the latter result owing to diminishing returns to capital accumulation. Chinese policy, however, appears to be moving in the opposite direction, to reemphasize investment-led growth.

November 13, 2024

Income Growth Outpaces Household Borrowing

U.S. household debt balances grew by $147 billion (0.8 percent) over the third quarter, according to the latest Quarterly Report on Household Debt and Credit from the New York Fed’s Center for Microeconomic Data. Balances on all loan products recorded moderate increases, led by mortgages (up $75 billion), credit cards (up $24 billion), and auto loans (up $18 billion). Meanwhile, delinquency rates have also risen over the past two years, returning to roughly pre-pandemic levels (and exceeding them in the case of credit cards and auto loans), though there are some signs of stabilization this quarter. Are rising aggregate debt burdens sustainable? Or is this expansion to be expected given increases in aggregate income and population size? In this post, we take a look at debt balances scaled by income, tracking the evolution of this ratio over the past twenty-five years.

November 12, 2024

Banking System Vulnerability: 2024 Update

After a period of relative stability, a series of bank failures in 2023 renewed questions about the fragility of the banking system. As in previous years, we provide in this post an update of four analytical models aimed at capturing different aspects of the vulnerability of the U.S. banking system using data through 2024:Q2 and discuss how these measures have changed since last year.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Liquidity | Permalink | Comments (4)

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics