The global corporate nonfinancial bond market is both a large investment asset class and a vital source of funding for nonfinancial firms. With $19 trillion outstanding at the end of 2024, a broad portfolio of corporate bonds would be expected to be well diversified. Yet, in 37 percent of months between 1998 and 2024, more than 80 percent of bonds in the ICE Global Bond Indices—a portfolio with over 10,000 constituents spanning diverse industries, credit ratings, and regions—moved in the same direction, suggesting a large degree of synchronization. In this post, we introduce the global credit factor, which proxies for the global price of risk in international corporate bond markets. The global credit factor creates a global credit cycle in bond risk premia and generates predictable comovement in bond prices.

Measuring the Global Credit Cycle

Is there a global credit cycle in global corporate bond returns? To answer that question, we construct a proxy for a global component of credit risk pricing, which we dub the global credit factor. Our approach, described in detail in our Staff Report, is motivated by the literature on intermediary asset pricing, which argues that risk prices reflect balance sheet constraints of financial intermediaries. Because the tightness of balance sheet constraints fluctuates over time, so do risk prices.

We implement this idea in our setting by estimating a nonlinear predictive relationship between returns on portfolios of corporate bonds and observable predictors. We sort bonds into portfolios by credit rating—AAA/AA, A, BBB, and high yield—so that the global credit factor uses information both from the overall time-series variation in returns and from the differential fluctuation in returns across bonds with different levels of credit risk. Focusing on the predictive relationship between predictors and returns allows us to estimate how risk attitudes translate into expected, rather than realized, returns; that is, into the price of credit risk.

The observable predictors proxy for the tightness of balance sheet constraints. In particular, we use the average default-risk-adjusted spread for U.S. bonds, also called the excess bond premium (EBP), and the Chicago Board Options Exchange’s CBOE Volatility Index, or VIX. While Gilchrist and Zakrajsek (2012) argue that the EBP is a quantitative proxy of the risk attitude of financial intermediaries in fixed income markets, the price of global credit risk is likely to also reflect the risk attitudes of a broader set of intermediaries. For this reason, we also allow the factor to depend on the VIX, a commonly used proxy for the tightness of constraints faced by a broader set of institutions.

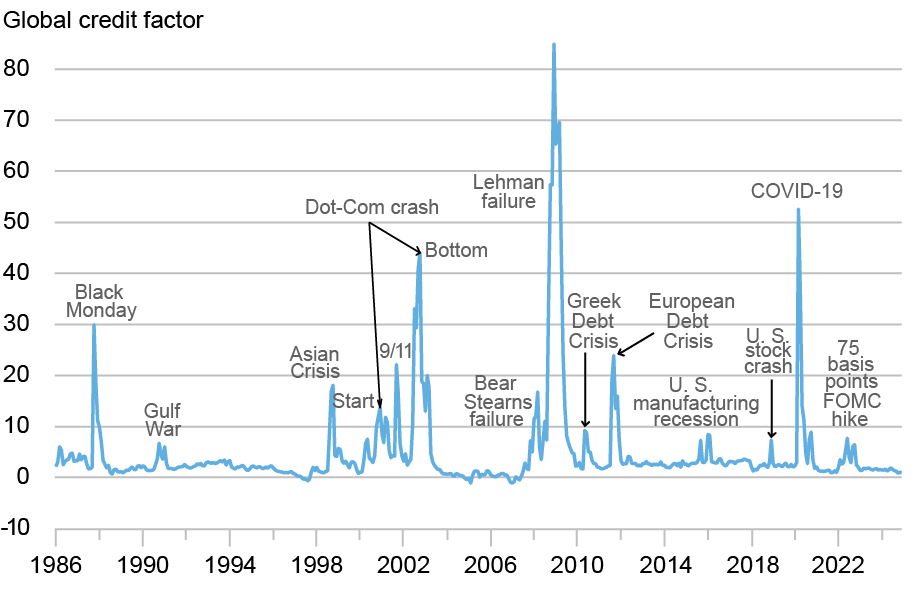

The next chart shows the time series of the estimated global credit factor, together with some of the largest events identified by peaks in the measure. The global credit factor tightens when both the EBP and the VIX are high, such as during the COVID-19 pandemic (March 2020) and in the aftermath of the Lehman Brothers liquidation (Fall 2008). The factor is instead historically low—attitudes towards global credit risk are particularly benign—in advance of large tightenings of the global credit factor, such as in the run-up to the Asian crisis and the global financial crisis.

The Global Credit Factor over Time

Note: The chart shows the time series of the global credit factor, together with some notable events in the time series.

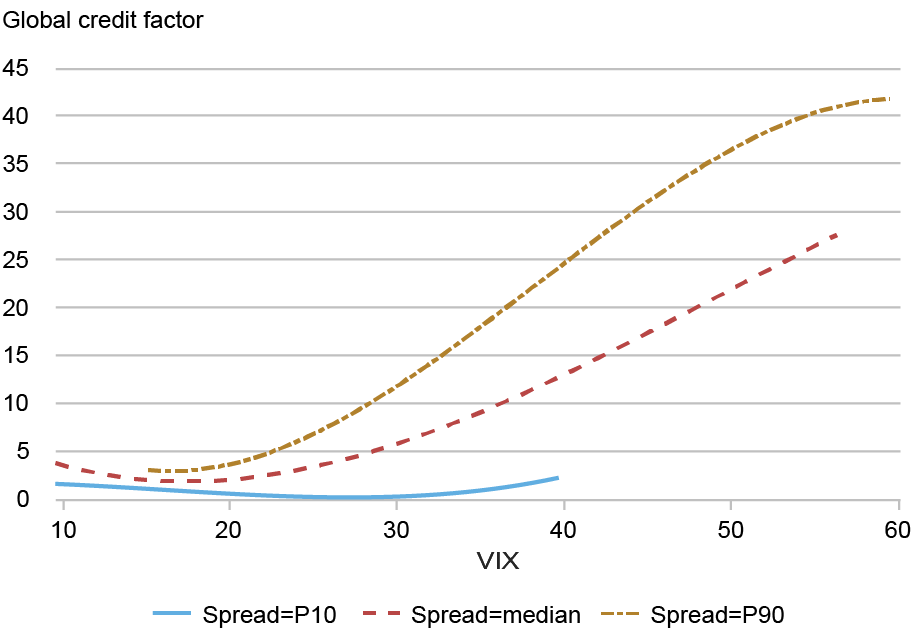

We examine the relationship between the global credit factor and the VIX, conditional on the level of credit spreads, in the next chart. The chart shows that the estimated relationship between the global price of credit risk and the VIX is highly nonlinear. For levels of the VIX below the historical median of 18, the global credit factor is to a large extent flat as a function of the VIX, regardless of the level of credit spreads. When the VIX is above the median, however, the slope of the global credit factor with respect to the VIX increases as the level of credit spreads increases. In other words, the factor is more sensitive to increases in the VIX at higher levels of credit spreads, highlighting the importance of interactions between credit spreads and volatility in determining the global price of credit risk.

A Nonlinear Relationship Between the Global Credit Factor and the VIX

Notes: The chart shows the relationship between the global credit factor and the VIX, conditional on three levels of the credit spread: the historical tenth percentile (EBP=-0.65), the historical median (EBP=-0.19), and the historical ninetieth percentile (EBP=0.51). EBP is excess bond premium.

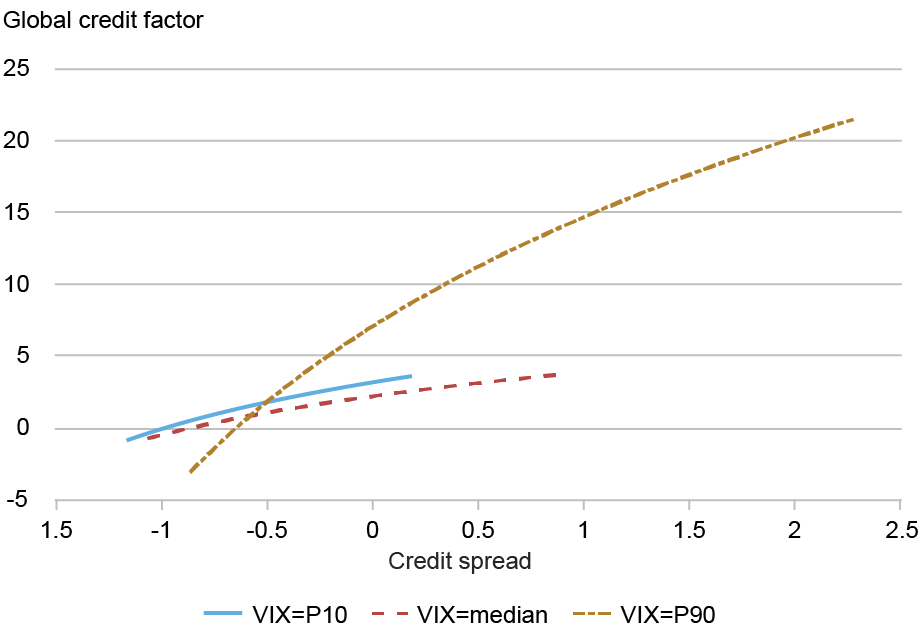

Considering the relationship between the global credit factor and the EBP, instead, a similar picture emerges. The sensitivity of the global credit factor to the EBP is similar for low and intermediate levels of the VIX. For high levels of the VIX, the factor is considerably more sensitive to changes in credit spreads.

A Nonlinear Relationship Between the Global Credit Factor and the EBP

Notes: The chart shows the relationship between the global credit factor and the excess bond premium (EBP), conditional on three levels of the VIX: the historical tenth percentile (VIX=12), the historical median (VIX=18), and the historical ninetieth percentile (VIX=29).

Is the Factor Truly Global?

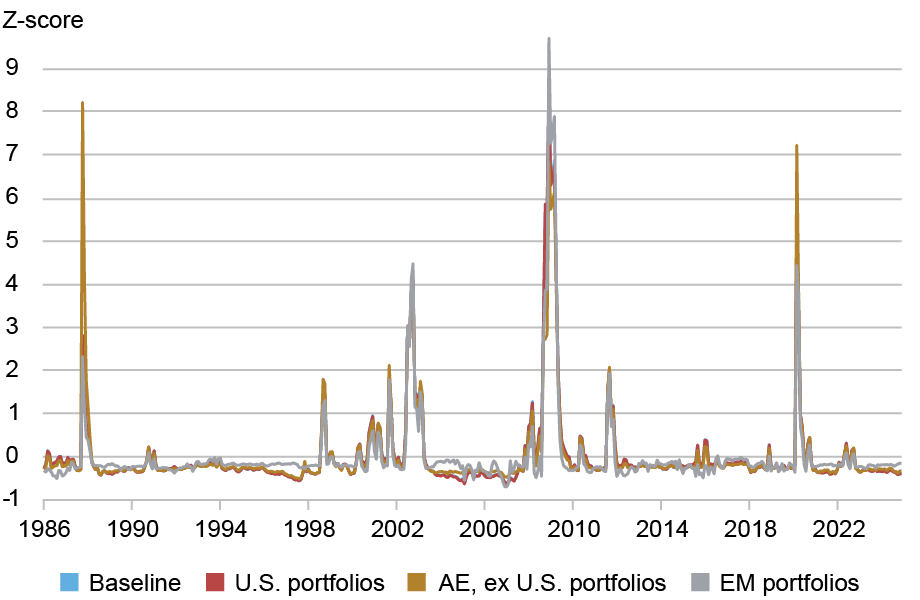

We construct the global credit factor to target returns on bonds of firms in advanced economies, using U.S.-based variables as predictors. Does the credit factor truly capture global conditions? To answer that question, we conduct two exercises. In the first exercise, we keep the same predictors—the U.S. EBP and the VIX—and examine how the estimate of the global credit factor changes as we change the set of target returns. The next chart shows that the estimated time series of global credit risk are similar regardless of whether we use the original advanced economy portfolios, portfolios of bonds of U.S. firms only, portfolios of bonds of firms in the rest of advanced economies, or, indeed, portfolios of bonds of firms in emerging markets. This finding is particularly remarkable since our data on returns on non-U.S. bonds only starts in 1998, so that the relationship between the factor and predictors is stable even outside of the data used for estimation.

Factors Constructed to Target Alternative Portfolios Are Similar to the Baseline

Notes: The chart shows the time series of the global credit factor, together with factors constructed to fit three alternative sets of portfolios: portfolios of U.S. corporate bonds only, portfolios of advanced economy (AE) bonds excluding the U.S., and portfolios of emerging market (EM) corporate bonds. All factors are rescaled to have a mean 0 and a standard deviation 1 for comparability.

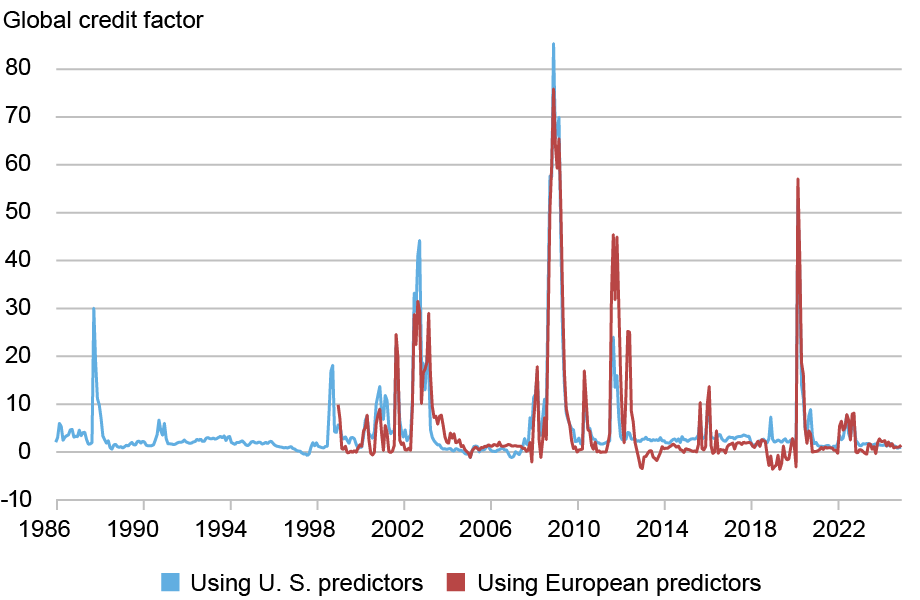

In the second exercise, we consider how the estimated global credit factor changes when we use European predictors instead of U.S.-based predictors. In particular, in the chart below, we use the Euro Stoxx 50 Volatility, or VSTOXX, instead of the VIX and the weighted average default adjusted spread across eight major European countries instead of the U.S. EBP. The chart below shows that the factor constructed using European predictors is similar to our global credit factor, albeit each factor reflects some local events. For the factor constructed using European predictors, the European debt crisis is a significantly larger event than for the baseline global credit factor. Similarly, the baseline credit factor tightens during the U.S. stock market crash in December 2018, while the credit factor built with European predictors identifies the same period as an episode of loose credit conditions. Thus, while the price of credit risk is indeed global, the locality of predictors used may influence individual observations.

Factors Constructed Using U.S. and European Predictors Are Similar

Notes: The chart shows the time series of the global credit factor, together with the global credit factor constructed using the Euro Stoxx 50 Volatility (VSTOXX) instead of the VIX, and the weighted average excess bond premium (EBP) across eight European countries instead of the U.S. EBP.

Wrapping Up

Global credit markets are deeply interconnected. In this blog post, we have argued that there is a common component to global corporate bond returns. In our Staff Report, we show that high levels of the factor predict high corporate bond returns and deteriorations in local credit conditions, and are associated with outflows from global bond funds. Taken together, our results are consistent with the factor proxying for a common, time-varying global price of credit risk.

Nina Boyarchenko is a financial research advisor in the Federal Reserve Bank of New York’s Research and Statistics Group.

Leonardo Elias is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Nina Boyarchenko and Leonardo Elias, “The Global Credit Cycle in Corporate Bond Returns,” Federal Reserve Bank of New York Liberty Street Economics, May 19, 2026, https://doi.org/10.59576/lse.20260519

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics