260 posts on "Financial Institutions"

June 1, 2017

Just Released: Bank Loan Performance Under the Magnifying Glass

The New York Fed’s recently released Quarterly Trends for Consolidated U.S. Banking Organizations (QT report) confirms that bank loan portfolios look a lot healthier than they did just a few years ago, reflecting the sustained economic recovery from the Great Recession. In this post, we sharpen the focus to look at bank loan performance in more detail, using more disaggregated charts added to the QT report this quarter.

May 24, 2017

Dealer Balance Sheets and Corporate Bond Liquidity Provision

Regulatory reforms since the financial crisis have sought to make the financial system safer and severe financial crises less likely.

March 29, 2017

QE Frictions: Could Banks Have Favored Refinancing over New Purchase Borrowing?

Quantitative easing (QE)—the Fed Reserve’s effort to provide policy accommodation lowering long-term interest rates at a time when the federal funds rate as near its lower bound—has generated a great deal of research, both about its impact and about the frictions that might limit that impact.

March 20, 2017

Money Market Funds and the New SEC Regulation

On October 14, 2016, amendments to Securities and Exchange Commission (SEC) rule 2a-7, which governs money market mutual funds (MMFs), went into effect. The changes are designed to reduce MMFs’ susceptibility to destabilizing runs and contain two principal requirements.

February 27, 2017

China’s Continuing Credit Boom

Debt in China has increased dramatically in recent years, accounting for roughly one-half of all new credit created globally since 2005.

February 22, 2017

Getting More from the Senior Loan Officer Opinion Survey?

Every quarter, senior loan officers at selected large banks around the United States are asked by Fed economists how their standards for approving business loans changed compared with the quarter before. Of all the questions in the Senior Loan Officer Opinion Survey (SLOOS), responses to that question about standards usually attract the most attention from the financial press and researchers. Relatively ignored by comparison are loan officers’ reports on how they changed interest spreads, collateral requirements, and other terms on loans they are willing to approve. Lenders can clearly expand or contract credit by altering those terms even without changing their standards for approving loans, so we investigate whether the reports on loan terms collected in the SLOOS are also informative.

February 13, 2017

How Resilient Is the U.S. Housing Market Now?

Housing is by far the most important asset for most households, and, not coincidentally, housing debt dwarfs other household liabilities. The relationship between housing debt and housing values figures significantly in financial and macroeconomic stability, as events during the housing bust of 2006-12 clearly demonstrated. This week, Liberty Street Economics presents five posts touching on various aspects of housing, from the changing relationship between mortgage debt and housing equity to the future of homeownership. In today’s post, we provide estimates of housing equity and explore how vulnerable households are to declines in house prices, using methods introduced in our paper “Tracking and Stress Testing U.S. Household Leverage.”

Posted at 7:00 am in Financial Institutions, Household Finance, Macroeconomics | Permalink | Comments (1)

December 19, 2016

Investigating the Proposed Overnight Treasury GC Repo Benchmark Rates

In its recent “Statement Regarding the Publication of Overnight Treasury GC Repo Rates,” the Federal Reserve Bank of New York, in cooperation with the U.S. Treasury Department’s Office of Financial Research, announced the potential publication of three overnight Treasury general collateral (GC) repurchase (repo) benchmark rates.

December 5, 2016

Are All CLOs Equal?

Stavros Peristiani and João A.C. Santos Asset securitization is an important source of corporate funding in capital markets. Collateralized loan obligations (CLOs) are securitization structures that allow syndicated bank lenders and bond underwriters to repackage business loans and sell them to investors as securities. CLOs are actively overseen by a collateral manager that has the […]

Posted at 7:00 am in Financial Institutions, Financial Markets, Regulation | Permalink | Comments (3)

November 18, 2016

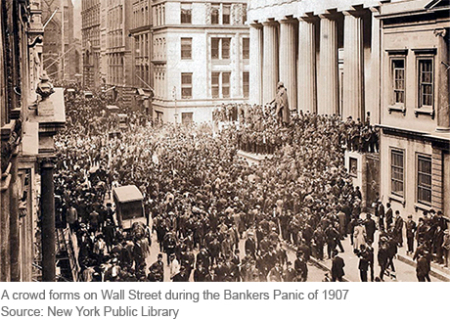

The Final Crisis Chronicle: The Panic of 1907 and the Birth of the Fed

The panic of 1907 was among the most severe we’ve covered in our series and also the most transformative, as it led to the creation of the Federal Reserve System. Also known as the “Knickerbocker Crisis,” the panic of 1907 shares features with the 2007-08 crisis, including “shadow banks” in the form high-flying, less-regulated trusts operating beyond the safety net of the time, and a pivotal “Lehman moment” when Knickerbocker Trust, the second-largest trust in the country, was allowed to fail after J.P. Morgan refused to save it.

Posted at 7:00 am in Crisis, Economic History, Financial Institutions, Financial Markets, Regulation, Treasury | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics