305 posts on "Financial Markets"

June 19, 2017

Introducing the Revised Broad Treasuries Financing Rate

The Federal Reserve Bank of New York in cooperation with the Office of Financial Research is proposing to publish three new overnight Treasury repurchase (repo) benchmark rates. Recently, the Federal Reserve decided to modify the construction of the broadest proposed benchmark rate (the other two proposed rates are expected to remain unchanged; see the Bank’s announcement on May 24). In this post, we describe the changes to this rate in further detail. We compare this revised rate to the originally proposed benchmark rate and show that, in the post-liftoff period, it trades higher, on average.

May 24, 2017

Dealer Balance Sheets and Corporate Bond Liquidity Provision

Regulatory reforms since the financial crisis have sought to make the financial system safer and severe financial crises less likely.

May 12, 2017

At the N.Y. Fed: The Evolution of OTC Derivatives Markets

The 2007-09 financial crisis illustrated the fragility of over-the-counter (OTC) derivatives markets and the contagion generated through bilateral derivatives exposures.

January 18, 2017

Advent of Trade Reporting for U.S. Treasury Securities

Greater transparency is coming to the U.S. Treasury securities market. Members of the Financial Industry Regulatory Authority (FINRA) will be required to report their trades in Treasuries using FINRA’s Trade Reporting and Compliance Engine (TRACE) starting July 10, 2017. Although initial collection efforts are focused on providing such data to the official sector, the public will likely have access in the future. In this post, I discuss the motivation for such reporting, how it came to be decided on, and the evidence from the corporate bond market on how public access to such data affects trading costs.

Posted at 7:00 am in Financial Markets | Permalink

January 11, 2017

Credit Market Arbitrage and Regulatory Leverage

In a companion post, we examined the recent trends in arbitraged-based measures of liquidity in the cash bond and credit default swap (CDS) markets.

January 9, 2017

Trends in Arbitrage‑Based Measures of Bond Liquidity

Corporate bonds are an important source of funding for public corporations in the United States.

December 20, 2016

At the N.Y. Fed: Capital Flows, Policy Dilemmas, and the Future of Global Financial Integration

The New York Fed recently hosted the third bi-annual Global Research Forum on International Macroeconomics and Finance, an event organized in conjunction with the European Central Bank (ECB) and the Federal Reserve Board. Bringing together a diverse group of academics, policymakers, and market participants, the two-day conference (November 17-18) was aimed at promoting discussion of frontier research on empirical and theoretical issues in international finance, banking, and open-economy macroeconomics. Understanding the drivers and implications of international capital flows was a major area of focus, along with the policy challenges posed by global financial integration.

Posted at 7:00 am in Financial Markets, International Economics, Macroeconomics, Monetary Policy | Permalink

December 5, 2016

Are All CLOs Equal?

Stavros Peristiani and João A.C. Santos Asset securitization is an important source of corporate funding in capital markets. Collateralized loan obligations (CLOs) are securitization structures that allow syndicated bank lenders and bond underwriters to repackage business loans and sell them to investors as securities. CLOs are actively overseen by a collateral manager that has the […]

Posted at 7:00 am in Financial Institutions, Financial Markets, Regulation | Permalink | Comments (3)

December 2, 2016

At the N.Y. Fed: Second Annual Conference on the Evolving Structure of the U.S. Treasury Market

The New York Fed recently hosted a second conference on the evolving structure of the Treasury market, co-sponsored with the U.S. Department of the Treasury, the Federal Reserve Board, the U.S. Securities and Exchange Commission (SEC), and the U.S. Commodity Futures Trading Commission (CFTC). The conference reviewed developments in the Treasury market since the Joint Staff Report on the “flash rally” of October 15, 2014, and the preceding year’s conference on the evolving structure of the Treasury market, including advances related to transaction data reporting and official perspectives on rules and regulations.

November 18, 2016

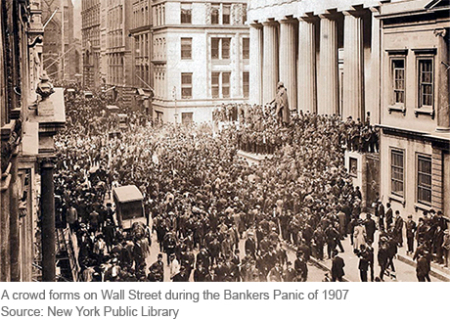

The Final Crisis Chronicle: The Panic of 1907 and the Birth of the Fed

The panic of 1907 was among the most severe we’ve covered in our series and also the most transformative, as it led to the creation of the Federal Reserve System. Also known as the “Knickerbocker Crisis,” the panic of 1907 shares features with the 2007-08 crisis, including “shadow banks” in the form high-flying, less-regulated trusts operating beyond the safety net of the time, and a pivotal “Lehman moment” when Knickerbocker Trust, the second-largest trust in the country, was allowed to fail after J.P. Morgan refused to save it.

Posted at 7:00 am in Crisis, Economic History, Financial Institutions, Financial Markets, Regulation, Treasury | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics