4 posts on "shadow banks"

November 18, 2020

The Impact of Natural Disasters on the Corporate Loan Market

Natural disasters are usually associated with an increase in the demand for credit by both households and companies in the affected regions. However, if capacity constraints preclude banks from meeting the local increase in demand, the banks may reduce lending elsewhere, thus propagating the shock to unaffected areas. In this post, we analyze the corporate loan market and find that banks, particularly those with lower capital, reduce credit provisioning to distant regions unaffected by natural disasters. We also find that shadow banks only partially offset the reduction in bank credit, so borrowers in regions unaffected by natural disasters experience a decline in credit supply.

November 13, 2019

The Side Effects of Shadow Banking on Liquidity Provision

Over the past two decades, the growth of shadow banking has transformed the way the U.S. banking system funds corporations. In this post, we describe how this growth has affected both the term loan and credit line businesses, and how the changes have resulted in a reduction in the liquidity insurance provided to firms.

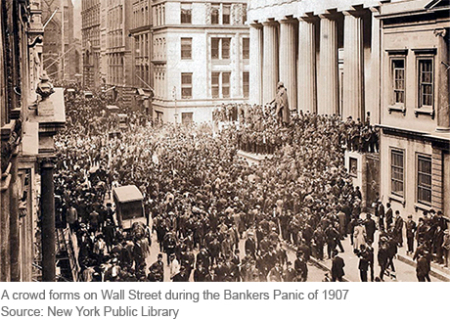

November 18, 2016

The Final Crisis Chronicle: The Panic of 1907 and the Birth of the Fed

The panic of 1907 was among the most severe we’ve covered in our series and also the most transformative, as it led to the creation of the Federal Reserve System. Also known as the “Knickerbocker Crisis,” the panic of 1907 shares features with the 2007-08 crisis, including “shadow banks” in the form high-flying, less-regulated trusts operating beyond the safety net of the time, and a pivotal “Lehman moment” when Knickerbocker Trust, the second-largest trust in the country, was allowed to fail after J.P. Morgan refused to save it.

Posted at 7:00 am in Crisis, Economic History, Financial Institutions, Financial Markets, Regulation, Treasury | Permalink

March 27, 2014

The Growth of Murky Finance

Building upon previous posts in this series that discussed individual banks, we examine the historical growth of the entire financial sector, relative to the rest of the economy.

Posted at 7:00 am in Economic History, Financial Institutions, Financial Markets, Regulation | Permalink | Comments (3)

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics