This post provides an update on two earlier blog posts (here and here) in which we discuss how consumers’ views about future inflation have evolved in a continually changing economic environment. Using data from the New York Fed’s Survey of Consumer Expectations (SCE), we show that while short-term inflation expectations have continued to trend upward, medium-term inflation expectations appear to have reached a plateau over the past few months, and longer-term inflation expectations have remained remarkably stable. Not surprisingly given recent movements in consumer prices, we find that most respondents agree that inflation will remain high over the next year. In contrast, and somewhat surprisingly, there is a divergence in consumers’ medium-term inflation expectations, in the sense that we observe a simultaneous increase in both the share of respondents who expect high inflation and the share of respondents who expect low inflation (and even deflation) three years from now. Finally, we show that individual consumers have become more uncertain about what inflation will be in the near future. However, in contrast to the pre-pandemic period, they tend to express less uncertainty about inflation further in the future.

The SCE is a monthly, internet-based survey produced by the Federal Reserve Bank of New York since June 2013. It is a twelve-month rotating panel (respondents are asked to take the survey for twelve consecutive months) of roughly 1,300 nationally representative U.S. household heads. Since the inception of the SCE, we have been eliciting consumers’ inflation expectations at the short- and medium-term horizons on a monthly basis. The short-term horizon corresponds to the year-ahead (with the survey question phrased as “over the next 12 months”), while the medium-term horizon corresponds to the three-year-ahead one-year rate of inflation (“0ver the 12-month period between M+24 and M+36,” where M is the month in which the respondent takes the survey). So, for instance, a respondent taking the survey in April 2022 is asked about inflation “over the 12-month period between April 2024 and April 2025.” Recently, we have on occasion elicited longer-term inflation expectations, by asking respondents to report their expected five-year-ahead one-year rate of inflation (“over the 12-month period between M+48 and M+60”). For each horizon, SCE respondents are asked to report their density forecasts by stating the percent chance that the rate of inflation will fall within pre-specified bins. These density forecasts are used to calculate the two measures that we focus on in this blog: the individual inflation expectation (the mean of a respondent’s density forecast), and the individual inflation uncertainty (measured as the interquartile range of a respondent’s density forecast).

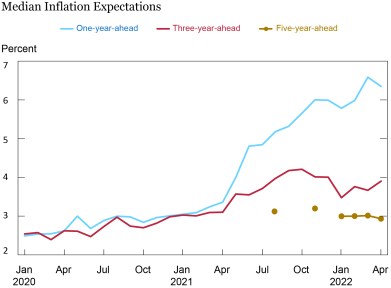

The Median Consumer Expects Inflation to Fade over the Next Few Years

SCE respondents think the current high inflation environment will not fade over the next twelve months, but that it will taper off in the next three years and not persist beyond that. The chart below shows the monthly median individual inflation expectation at each horizon since January 2020. As can be seen here, inflation expectations in January 2020 were similar to the average readings during 2018-19 and are therefore representative of the period directly before the COVID-19 pandemic. Short- and medium-term inflation expectations increased slightly and at a similar pace during the first year of the COVID-19 pandemic. In the spring of 2021, as readings of actual inflation started to surge, short-term and, to a lesser extent, medium-term inflation expectations started to increase at a faster rate, reaching levels not seen previously in the nearly ten years since the inception of the SCE. Note that, unlike one-year-ahead inflation expectations which are still on an increasing trajectory, three-year-ahead inflation expectations have leveled off in recent months and even started decreasing slightly after reaching a peak of 4.2 percent in September and October 2021. Looking now at the few data points we have for the longer horizon, five-year-ahead inflation expectations have been remarkably stable in recent months and substantially lower than short- and medium-term inflation expectations.

Inflation Expectations at the Longer Horizon Are Stable and Much Lower

Consumers’ Medium-Term Inflation Expectations Have Become More Divergent

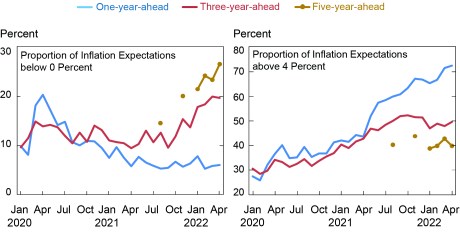

At the onset of the COVID-19 pandemic, respondents disagreed about what impact the pandemic would have on short-term inflation, but most of them now believe inflation will be high over the next year. The chart below shows the distribution of individual inflation expectations across respondents in a given month. The left panel shows the share of respondents with low inflation expectations in a given month (that is, with an individual inflation expectation below 0 percent, which corresponds to deflation). The right panel shows the share of respondents with high inflation expectations (that is, with an individual inflation expectation above 4 percent). Starting with the short-term horizon, the chart shows that at the onset of the COVID-19 pandemic in the spring of 2020, there was a sharp increase in the share of respondents who expected deflation (left panel) and, simultaneously, an increase in the share of respondents who expected high inflation (right panel). Hence, consumers’ short-term inflation expectations became more divergent at the onset of the pandemic, with some consumers expecting COVID-19 to be an inflationary supply shock over the subsequent twelve months, and other consumers expecting COVID-19 to be a large deflationary demand shock. Starting in the second half of 2020, the share of respondents with low short-term expectations declined, while the share of the respondents with high short-term expectations continued to increase, consistent with the overall increase in short-term inflation expectations discussed in the previous paragraph.

The divergence in inflation beliefs we observed for short-term expectations at the onset of the pandemic has shifted to medium-term expectations during the past eight months. The chart below shows little change in the share of respondents with extreme (high or low) medium-term inflation beliefs at the onset of the pandemic. This suggests that consumers initially thought the pandemic would not have a strong persistent effect on inflation. After the fall of 2020, the share of respondents who expect high inflation in the medium-term started to increase steadily (see right panel). However, the rate of increase over the past year was slower than at the short-term horizon. Furthermore, after reaching a plateau last fall, the share of respondents who expect high inflation has declined slightly in the past few months. Perhaps more surprisingly, the left panel of the chart below shows that the share of respondents who expect deflation in the medium-term started to increase sharply in the fall of last year, moving from about 10 percent in August 2020 to nearly 20 percent in March and April 2022.

Although we caution against drawing strong conclusions from only a few data points, it seems that the distribution of longer-term inflation expectations has shifted to the left (toward lower inflation outcomes) in recent months. The chart below indicates that the recent increase in the share of respondents with low inflation expectations is similar at the medium- and longer-term horizons. In contrast, the share of respondents who expect high inflation five years from now is substantially lower than at the short- and medium-term horizons and it has remained mostly stable over the past eight months.

The Distribution of Longer-Term Inflation Expectations Has Shifted toward Lower Inflation Outcomes

Note: An inflation expectation below 0 percent (as in the left panel) corresponds to deflation.

Individual Consumers Have Become More Uncertain about Future Inflation

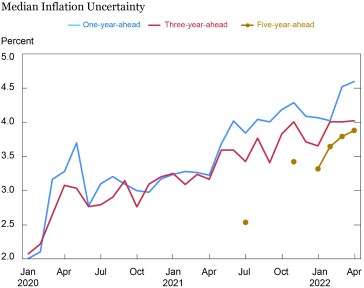

Finally, we find that consumers have become more uncertain about future inflation, especially at shorter horizons. The final chart shows the median of individual inflation uncertainty across respondents in a given month. As can be seen in this staff study, inflation uncertainty exhibited two main patterns prior to the pandemic. First, inflation uncertainty at both the short- and medium-term horizons had been declining slowly and steadily since the start of the SCE in 2013. Second, SCE respondents almost always expressed more uncertainty for three-year-ahead inflation than for one-year-ahead inflation, perhaps reflecting the fact that predicting inflation further into the future tends to be more difficult. The chart below shows a complete reversal of these two trends after the World Health Organization declared COVID-19 to be a pandemic in March 2020: inflation uncertainty at both horizons has since increased steadily to record levels, and short-term inflation uncertainty has generally been higher than medium-term inflation uncertainty. The few observations we have for longer-term inflation uncertainty seem to confirm these trends. Indeed, five-year-ahead inflation uncertainty has increased over the past eight months, but has remained substantially lower than at the one- and three-year horizons.

Inflation Uncertainty Is Lower at a Longer-Term Horizon

Note: The SCE measures individual inflation uncertainty as the interquartile range of a respondent’s inflation density forecast.

To conclude, the results presented in this blog post provide fresh evidence that consumers still do not expect the current spell of high inflation to persist long into the future. While median one-year-ahead inflation expectations have continued to rise over the past six months, three-year-ahead expectations have declined slightly, and five-year-ahead inflation expectations have remained remarkably stable and at a level well below recent inflation readings. However, there is now a divergence in consumers’ medium-term inflation expectations: a larger share of consumers expects high inflation three years from now, while simultaneously a growing share of consumers expects low inflation and even deflation. Finally, we have shown that consumers have become increasingly uncertain about future inflation, especially at shorter horizons. We are now conducting new research aimed at better understanding the factors driving these changes in consumer beliefs.

Olivier Armantier is head of Consumer Behavior Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Fatima Boumahdi is a senior research analyst in the Bank’s Research and Statistics Group.

Gizem Kosar is a research economist in Consumer Behavior Studies in the Bank’s Research and Statistics Group.

Jason Somerville is a research economist in Consumer Behavior Studies in the Bank’s Research and Statistics Group.

Giorgio Topa is an economic research advisor in Labor and Product Market Studies in the Bank’s Research and Statistics Group

Wilbert van der Klaauw is an economic research advisor on Household and Public Policy in the Bank’s Research and Statistics Group.

John C. Williams is the president and chief executive officer of the Bank.

Disclaimer

The views expressed in this post are those of the authors and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the authors.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics