What is the effect of a hike in interest rates on the economy? Building on recent research, we argue in this post that the answer to this question very much depends on how vulnerable the financial system is. We measure financial vulnerability using a novel concept—the financial stability interest rate r** (or “r-double-star”)—and show that, empirically, the economy is more sensitive to shocks when the gap between r** and current real rates is small or negative.

Financial Constraints and the Response to Macroeconomic Shocks

What do financial vulnerability and macroeconomic fragility—that is, the sensitivity of the economy to shocks—have to do with one another? One of the key lessons from the macrofinance literature of the past twenty-five years—starting with the seminal works of Bernanke, Gertler, and Gilchrist and Kiyotaki and Moore, and the more recent contributions by He and Krishnamurthy and Brunnermeier and Sannikov, to name just a few—is that the two are very interrelated. This is because of what Ben Bernanke and coauthors have called the financial accelerator mechanism.

To understand the idea of the financial accelerator, consider the case in which intermediaries are constrained by the amount of leverage they can have, with leverage defined as the ratio of assets over equity. An adverse economic shock that brings about a decline in asset prices increases leverage because the value of equity falls proportionally more than the value of assets. The resulting increase in leverage prompts intermediaries to sell assets in order to lower their leverage and meet the constraint. In turn, such sales put more downward pressure on asset prices, further increasing leverage. These are the fire-sale dynamics that take place during crises. The real side of these financial developments is that intermediaries are less able to finance any new investment spending, causing a fall in both aggregate demand and asset prices—now you see why the word “accelerator” is used. If, however, the financial system is not vulnerable—for instance, if leverage is low—then this accelerator is less likely to be set in motion. A bad shock still has adverse consequences, but they are much more muted.

A New Measure of Financial System Vulnerability

How do we know how vulnerable the financial system is? If vulnerability were measured by a single variable—say, again, leverage—then policymakers and regulators would only have to keep an eye on that one variable to know how vulnerable it is. In practice, financial vulnerability is multifaceted, and hence hard to assess. The famous “stress tests” are one indirect way of assessing vulnerability: Subject the economy to a hypothetical large shock (akin to the financial crisis, for example) and ask yourself, can the financial system withstand it? The outcome of the stress test is binary: one if the financial system enters a crisis, and zero if it does not—where a crisis is defined as a state of the world where certain constraints become binding (for example, capital falls below a certain threshold).

The idea of r** is similar to that of stress tests, except that the size of the shock is not fixed. Rather, we ask the question: How large a shock to real interest rates can the financial system take before entering a crisis? Add this shock to the current level of real interest rates, and you have found r**. If the financial system is strong and robust (r** well above current real interest rates), then it may take a really large shock to cause a financial crisis. If the system is very fragile (r** not too far above current rates), then a small increase in rates may be enough. Summing up, the gap between r** and current real rates provides a summary statistic of financial vulnerabilities. A nice feature of this method of measuring vulnerabilities is that it relates very clearly to the key policy instrument of central banks, the interest rate.

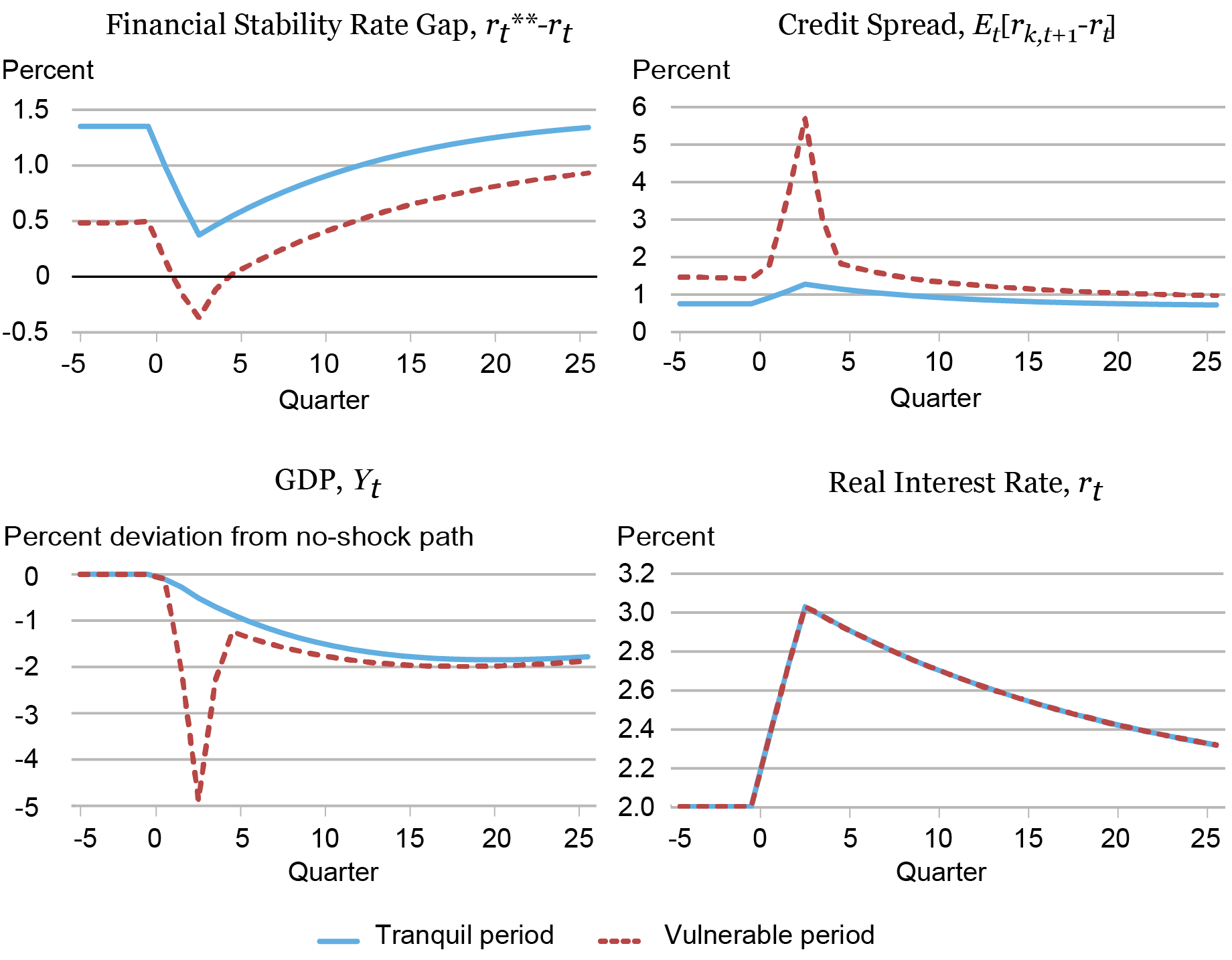

Financially Vulnerable and Nonvulnerable Periods

The chart below shows the responses of credit spreads and output to a one percentage point increase in real interest rates in our calibrated model. The blue solid lines display the responses when the economy is in a tranquil period (r** is almost 1.5 percentage points above r before the shock hits). The one percentage point shock is by construction not large enough to push the economy into the crisis region, with the r**–r gap staying positive throughout. As a consequence, the shock has only modest effects on output and spreads. The red dashed lines display the responses when the economy is much closer to the financially unstable region (r** is only 0.5 percentage points above r before the shock). In this case, the increase in interest rates is enough for the financial accelerator mechanism to kick in, and the response of both spreads and output to the shock is much larger.

The Effect of an Interest Rate Shock in Financially Vulnerable and Nonvulnerable Periods

The Sensitivity to Interest Rates

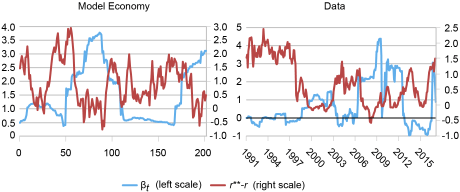

One key result is that financial conditions, here represented by spreads, will react more to an interest rate shock the more the r**–r gap is closer to zero or negative. The left-hand panel of the chart below plots the sensitivity of spreads to interest rate shocks (βt) in the model, computed with rolling regressions using model-generated time series. Not too surprisingly, this sensitivity is negatively correlated with the gap. This is also true in the data, as shown in the right-hand panel. In the data, movements in interest rates are endogenous—that is, interest rates react to economic and financial conditions. Therefore, we measure exogenous changes in rates as provided by Jarociński and Karadi. The estimated sensitivity quantitatively matches that in the model during periods of stress.

The Sensitivity of Credit Spreads to Interest Rate Shocks

Notes: r**-r is calculated using the real federal funds rate and the Gilchrist and Zakrajšek (2012) spread. The real federal funds rate is the effective rate minus twelve-month core inflation according to the price index for personal consumption expenditures.

These findings leave us with many questions. First and foremost, why does the financial system put itself in the position of being vulnerable to shocks? Our next post will address this issue.

Ozge Akinci is an economic research advisor in International Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Gianluca Benigno is a professor of economics at the University of Lausanne.

Marco Del Negro is an economic research advisor in Macroeconomic and Monetary Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Ethan Nourbash is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Albert Queralto is chief of the Global Modeling Studies Section in the Federal Reserve Board’s Division of International Finance.

How to cite this post:

Ozge Akinci, Gianluca Benigno, Marco Del Negro, Ethan Nourbash, and Albert Queralto, “Financial Vulnerability and Macroeconomic Fragility,” Federal Reserve Bank of New York Liberty Street Economics, May 22, 2023, https://libertystreeteconomics.newyorkfed.org/2023/05/financial-vulnerability-and-macroeconomic-fragility/

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics

I read this with interest! Missing of course is an analysis of where r and r** are estimated to be at this time!