In a recent research paper we argue that interest rates have very different consequences for current versus future financial stability. In the short run, lower real rates mean higher asset prices and hence higher net worth for financial institutions. In the long run, lower real rates lead intermediaries to shift their portfolios toward risky assets, making them more vulnerable over time. In this post, we use a model to highlight the challenging trade-offs faced by policymakers in setting interest rates.

A Macrofinance Model

We build a macrofinance model with two states of the world, tranquil periods and periods of financial turmoil where intermediaries’ lending is constrained. In the model, this occasionally binding constraint is due to so-called agency frictions, following the seminal work of Gertler and Kiyotaki: bankers may simply walk away with your money if you lend them too much, which places a limit on their leverage. Recent events in the crypto world indicate that even this literal interpretation of the constraint may not be too farfetched. More broadly, stepping aside from the model, these agency frictions capture the fact that our financial system is, to say the least, imperfect: when given too much of a free rein, financial actors could do stuff one would not necessarily want them to do with the money they are given. To this leverage constraint, we add the twist that the more the intermediaries invest in risky assets, the less trustworthy they become.

The Short- and Medium-Run Impact of Lower Interest Rates

Now let’s talk about interest rates. Imagine a world where real rates fall for a prolonged period of time. In the short run, this is great news for financial intermediaries as the assets in their portfolio are worth more, which boosts their net worth and reduces their leverage. As a result, intermediaries are ready to lend. Where do they invest their money? Not into safe assets; their real return has just fallen. But the real return of riskier stuff is higher and intermediaries, with their healthy balance sheets, have an incentive for reach-for-yield behavior. Over time, this risky lending makes them more vulnerable, and a few years down the road, if some bad economic shock hits, they run the risk of going broke.

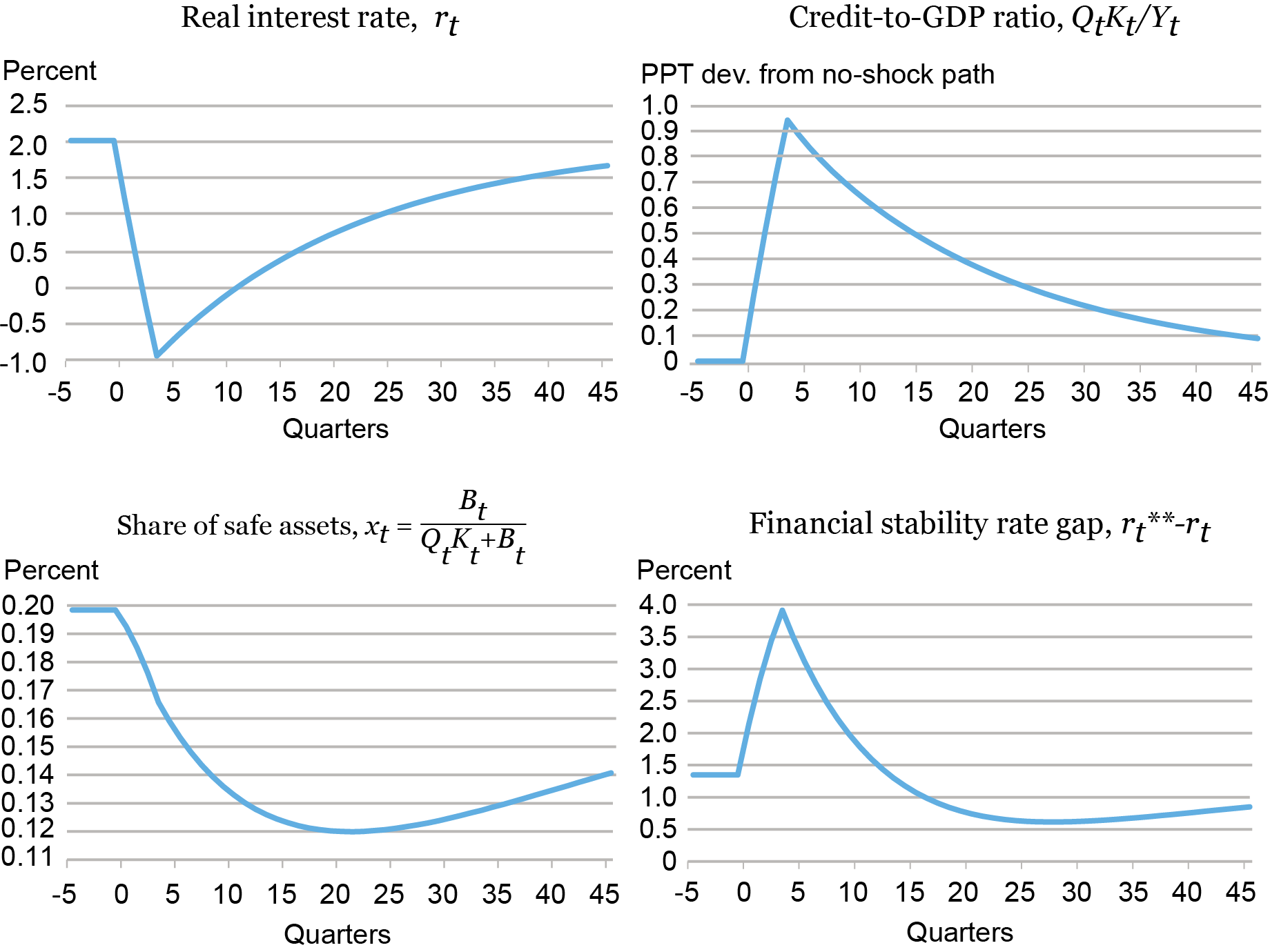

The simulated model responses shown in the panel chart below spell out the intermediaries’ response to the persistent interest rate shock. The upper-left panel shows the trajectory of interest rates. The upper-right panel shows credit to the economy over GDP. This ratio increases steadily as intermediaries invest in capital. One consequence of this increase is that the intermediaries’ portfolios shift more and more toward risky assets, as shown in the bottom left panel which plots the ratio of safe assets in the intermediaries’ portfolios. Such a shift in portfolio composition leaves the financial system more fragile. The r**-r gap, which measures the degree of financial vulnerability in the economy (as we discussed in a companion post) first widens on impact as the intermediaries’ net worth is boosted by the valuation effects (lower right panel). But then it drops steadily as a consequence of the reach for yield and ends up lower than where it started, thereby (in a richer model where the real rate is affected by policy) reducing the policy space—a phenomenon that Brunnermeier calls “financial dominance.”

Persistently Low Interest Rates May Give Rise to Higher Financial Fragility in the Future

We should mention that the finding that persistently lower interest rates may increase the fragility of the financial system is not unique to our paper. Coimbra and Rey, Adrian and Duarte, and Boissay et al. all have similar results within related frameworks. What is perhaps slightly different in our approach, which is based on a standard macrofinance model, is that it features both the positive short-run and the negative long-run effects of the interest rate reduction, thereby highlighting a potentially important intertemporal trade-off for policymakers.

Interest Rates and “Growth-at-Risk”

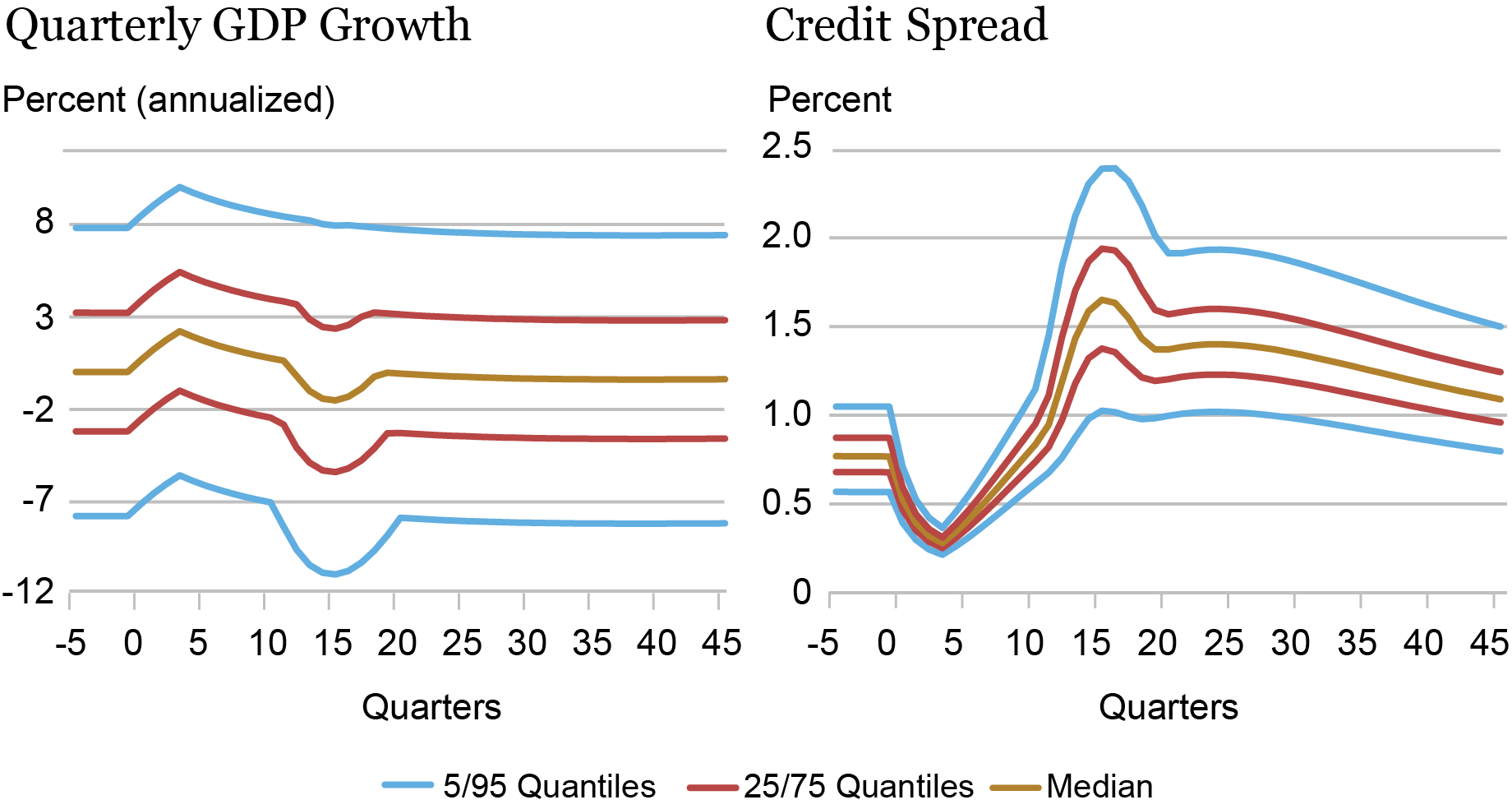

We have seen that persistently lower interest rates may leave the financial system more fragile in the medium run. What about the real economy? The chart below addresses this question. It shows the distribution of possible economic outcomes for two variables—GDP growth (left panel) and credit spreads (right panel)—as the economy evolves following the persistent decline in interest rates (specifically, the chart displays the evolution of the 5th, 25th, 50th, 75th, and 95th quantiles). The reason we focus on the distribution is to highlight the fact that the higher financial vulnerability leaves the economy at greater mercy of luck. If no bad shocks occur, then the economic consequences are minor. But if the economy is hit by such shocks, the effects can be dire.

Growth-at-Risk in the Model

The chart shows that, on impact, the cut in interest rates boosts the economy and its effects are symmetric across the distribution. This is not surprising in light of the dynamics discussed so far. The higher net worth of intermediaries leads to a compression of credit spreads, and the increase of credit to the economy boosts investment, and GDP growth with it. What happens over the next three years is very asymmetric across the distribution. The upper quantiles are barely affected. But the lower quantiles show that the chances of a severe dip in output and a spike in spreads—in other words, of a financial crisis—have increased. As we discussed in a companion post, a more financially vulnerable economy is also more fragile with respect to bad economic shocks.

Caveats

We conclude by stressing what the reader should not take away from our research. The reader should not come to the conclusion that low interest rates are bad for financial stability and should be avoided. First of all, we are in the presence of an intertemporal trade-off between the short- and medium-run effects, as shown above. Even if financial stability were the only objective, policymakers may want to cut rates to avoid entering a financial crisis if for whatever reason, at that point in time, the system is very vulnerable. You may retort that they may want to cut rates only for a short while, so they get the benefit but not the cost—but bear in mind that temporary cuts would not have much of an effect on asset prices either. In other words, there may not be a magic bullet.

Second, macroeconomic stability is also a policymakers’ concern—in fact, in the case of the U.S., it is in the central bank’s mandate: “full employment and price stability.’’ Much literature (Holston, Laubach, and Williams and Del Negro, Giannone, Giannoni, and Tambalotti, among many others) has shown that the low real interest rates in the pre-COVID years were due to macro and financial factors that are arguably outside the policymakers’ influence, such as low growth, demographics, or the presence of a convenience yield for Treasuries. Of course, policymakers could have chosen to disregard those factors and keep interest rates elevated, but this would likely come at a very steep cost. For example, the recovery from the Great Recession was long and painful even with very low rates. In sum, policymakers face unavoidable trade-offs for which they have to balance. What that is in the context of our model, let alone reality, is not obvious and remains a question motivating future research.

Ozge Akinci is an economic research advisor in International Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Gianluca Benigno is a professor of economics at the University of Lausanne.

Marco Del Negro is an economic research advisor in Macroeconomic and Monetary Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Ethan Nourbash is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

Albert Queralto is chief of the Global Modeling Studies Section in the Federal Reserve Board’s Division of International Finance.

How to cite this post:

Ozge Akinci, Gianluca Benigno, Marco Del Negro, Ethan Nourbash, and Albert Queralto, “Financial Stability and Interest Rates,” Federal Reserve Bank of New York Liberty Street Economics, May 23, 2023, https://libertystreeteconomics.newyorkfed.org/2023/05/financial-stability-and-interest-rates/

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics