In May 2022, Sam Khater—chief economist for Freddie Mac—argued that a surge in first-time buyers had been an important driver of the housing market the previous year. In contrast, using data from the New York Fed Consumer Credit Panel, we find that the share of home purchases by first-time buyers fell in 2021. This suggests that other factors were important to the rapid increase in house prices in 2021.

First-time buyer (FTB) activity affects the net supply of owner-occupied homes on the market, as an FTB purchases a home but is not selling a home—in contrast to a repeat-buyer, who both purchases and sells a home. The official definition of an FTB is a household that takes out a mortgage to purchase a home and has not been a homeowner for the past three years. This overstates the actual FTB share (on average by around 15 percentage points since 2002) by including previous homeowners who had been renting for at least three years prior to their current home purchase. However, the official definition of an FTB is appropriate for examining renters transitioning to owning and their effect on net housing supply.

We use New York Fed Consumer Credit Panel (CCP) data to identify FTBs using the official definition. The CCP is constructed from a nationally representative random sample of anonymized Equifax credit report data covering 5 percent of household credit files. The data set enables users to follow a given household through time. For any household that is obtaining a mortgage, we can determine whether the household has had a mortgage over the past three years. Importantly, the CCP data do not reflect all-cash purchases. We assume that FTBs always finance home purchases with a mortgage.

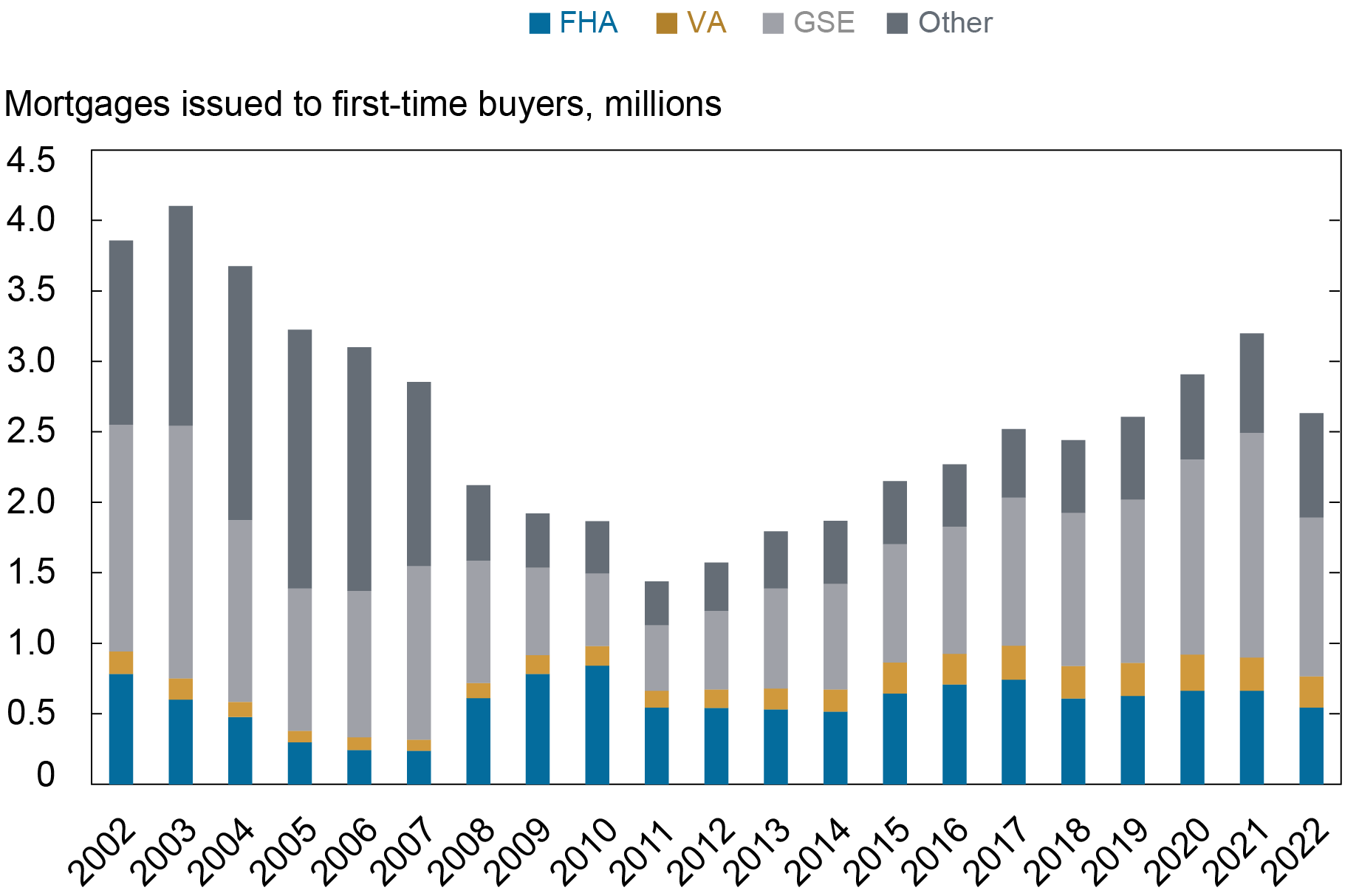

There was an increase in the volume of FTB mortgages between 2020 and 2021. As shown in the chart below, this increase was driven by FTBs taking out mortgages guaranteed by the GSEs.

Rise in 2021 FTB Purchases Concentrated in GSE Mortgages

Extrapolating the 2021 GSE FTB activity to the whole market would support Khater’s view of a significant rise in overall FTB activity. In aggregate, though, the rise in FTB activity in 2021 reflects a trend that began back in 2011. To better gauge the impact of FTBs we normalize the number of FTB mortgages by a measure of home sales.

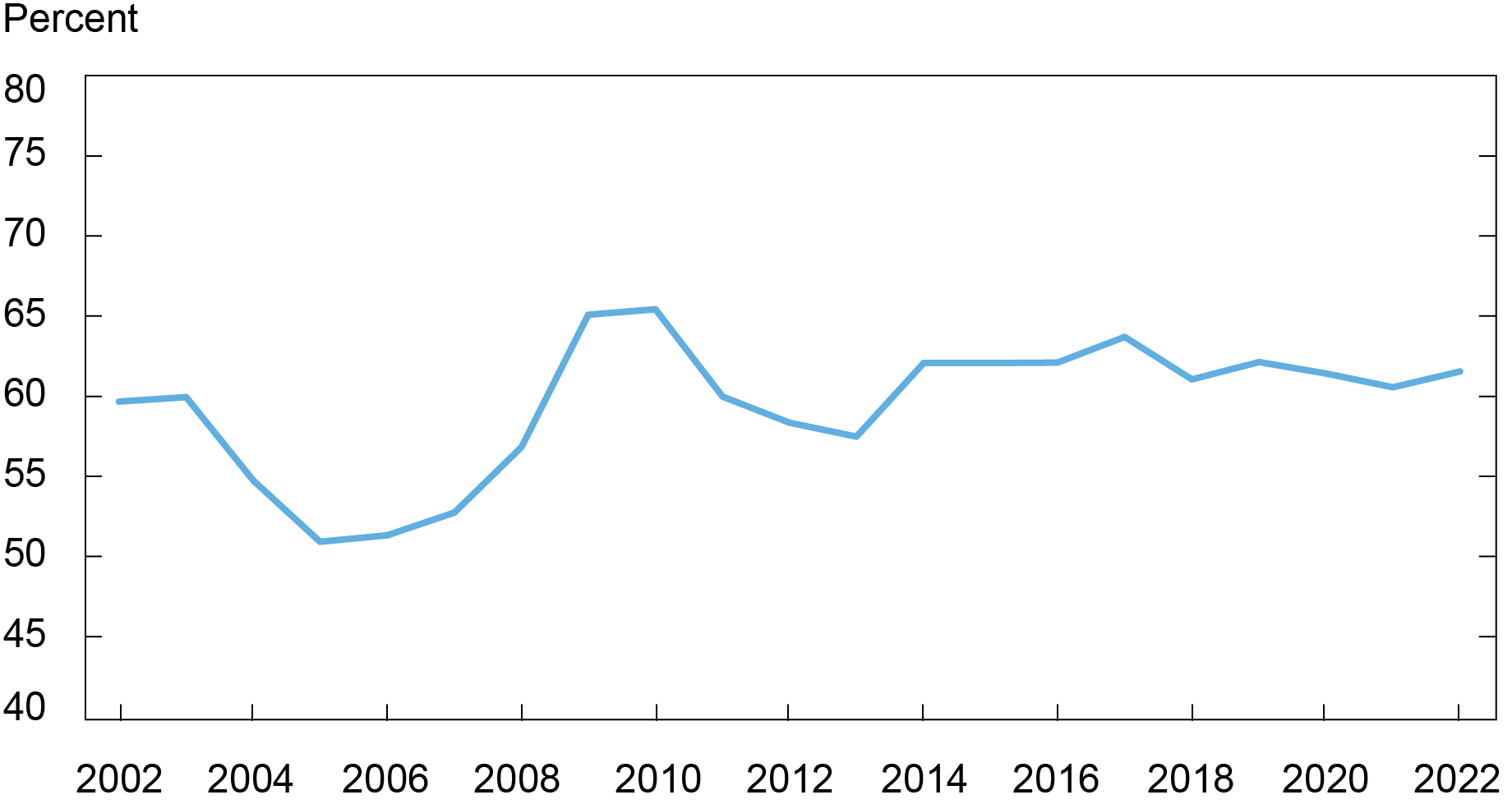

Our first measure of the FTB share uses homes purchased with a mortgage as the denominator. The FTB share is the number of mortgages taken out by FTBs each year divided by the total number of purchase mortgages taken out that year. The chart below shows the FTB share from 2002 through 2021.

FTB Share of Total Purchase Mortgages Over Time

The share of purchase mortgages by FTBs using the official definition has been relatively flat since 2014. There was a slight decrease in this share between 2020 and 2021 (from 61.4 percent to 60.6 percent). Given the behavior of this FTB share, it does not seem likely that FTBs were an important contributor to the rapid home price increases observed in 2021.

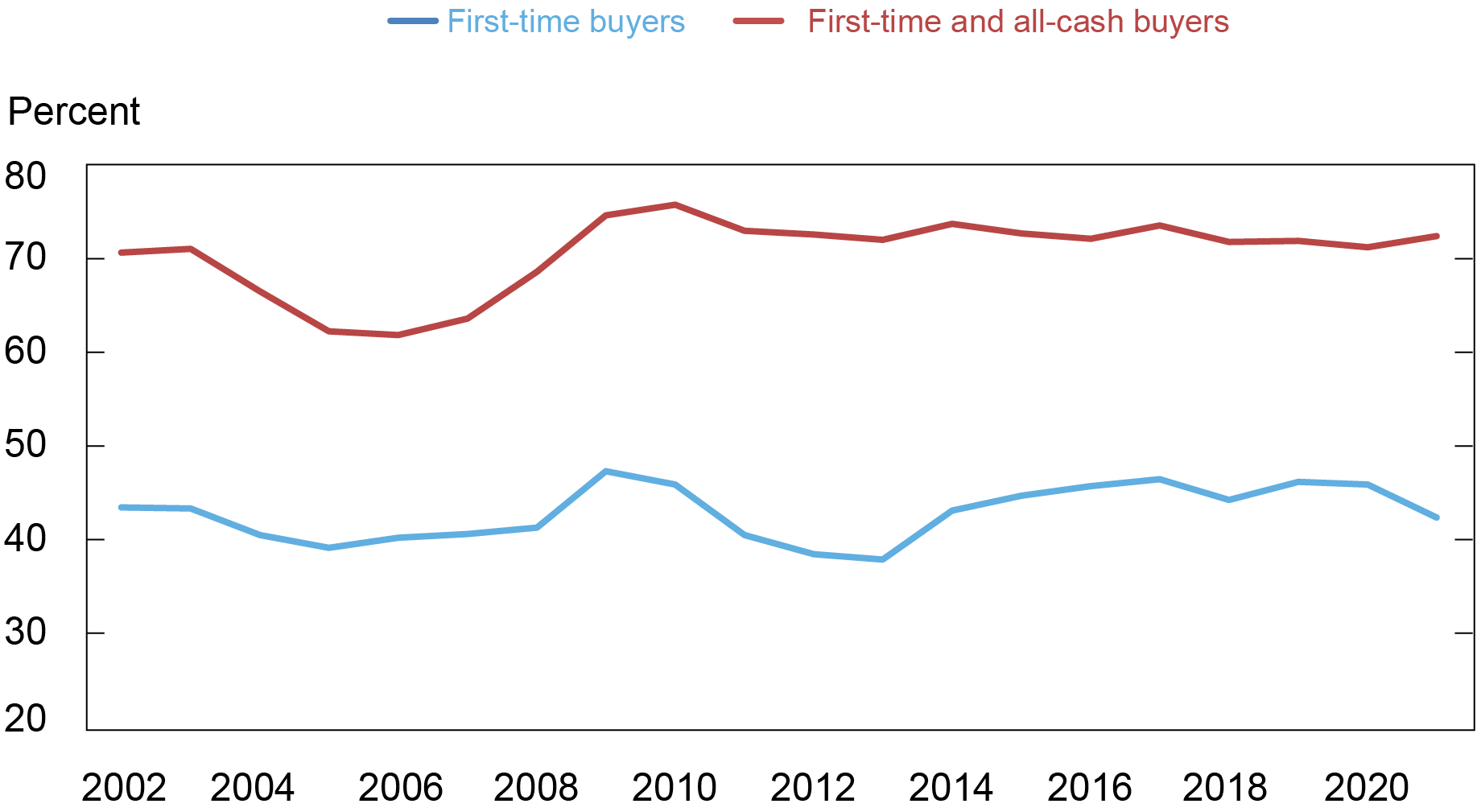

However, the impact of FTBs on the net supply of housing on the market and house prices will be more closely related to the FTB share relative to total home purchases—not just purchases financed using a mortgage. To recalculate our FTB share to reflect total purchases, we use data from Redfin on the fraction of home purchases by “all-cash buyers.” We continue our assumption that FTBs always finance their home purchase with a mortgage and add the assumption that cash buyers are not FTBs.

Data reported by Redfin indicate a 5-percentage point increase in all-cash purchases between 2020 and 2021. As a result, as shown in the chart below, the share of FTBs as a fraction of total home purchases declined from 45.9 percent in 2020 to 42.4 percent in 2021. This indicates that cash buyers were taking market share from FTBs.

First-Time Buyers and Cash Buyers as a Fraction of All Home Purchases

If we assume that most cash buyers intend to rent out the property, then cash buyers are like FTBs in that they typically purchase a property, but do not simultaneously sell a property. This suggests that we also consider the share of FTBs and all-cash buyers as a percentage of all home purchases.

Adding purchases by FTBs and all-cash buyers, we see that their combined share increases between 2020 to 2021—from 71.2 percent to 72.4 percent. However, the average value of this share over the past ten years is also 72.4 percent. This increase, by itself, is unlikely to have had a meaningful impact on “months’ supply” (the number of homes listed for sale divided by the average home sales per month) or house prices.

First-time buyers differ from repeat buyers in that they demand a house but do not supply a house. A rise in the FTB share, holding other things constant, will put downward pressure on the months’ supply of homes on the market and upward pressure on house prices. Our analysis shows that FTB purchases declined slightly in 2021 as a share of total mortgages, and declined more significantly as a share of total home purchases. In contrast, the combined shares of FTBs and all-cash buyers as a fraction of total home purchases increased only modestly. The rapid house price appreciation seen in 2021 likely reflects other factors, such as a change in the preference for owner-occupied housing due to the increase in work-from-home arrangements.

Donghoon Lee is an economic research advisor in Consumer Behavior Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Joseph S. Tracy is a non-resident senior scholar at the American Enterprise Institute.

How to cite this post:

Donghoon Lee and Joseph S. Tracy, “First‑Time Buyers Did Not Drive Strong House Price Appreciation in 2021,” Federal Reserve Bank of New York Liberty Street Economics, May 15, 2023, https://libertystreeteconomics.newyorkfed.org/2023/05/first-time-buyers-did-not-drive-strong-house-price-appreciation-in-2021/

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics