In support of the National Flood Insurance Program (NFIP), the Federal Emergency Management Agency (FEMA) creates flood maps that indicate areas with high flood risk, where mortgage applicants must buy flood insurance. The effects of flood insurance mandates were discussed in detail in a prior blog series. In 2021 alone, more than $200 billion worth of mortgages were originated in areas covered by a flood map. However, these maps are discrete, whereas the underlying flood risk may be continuous, and they are sometimes outdated. As a result, official flood maps may not fully capture the true flood risk an area faces. In this post, we make use of unique property-level mortgage data and find that in 2021, mortgages worth over $600 billion were originated in areas with high flood risk but no flood map. We examine what types of lenders are aware of this “unmapped” flood risk and how they adjust their lending practices. We find that—on average—lenders are more reluctant to lend in these unmapped yet risky regions. Those that do, such as nonbanks, are more aggressive at securitizing and selling off risky loans.

A Property-Level Approach

Past work that has attempted to analyze the impact of flood risk on mortgage lending has suffered from a lack of either property-level flood risk data or property-level mortgage data. This deficiency has forced researchers to make assumptions about flood risk or mortgage lending over larger areas with multiple properties, ultimately preventing clean identification. In this analysis (and the associated paper), we overcome these issues by leveraging a unique data set that matches property-level mortgage records from 2018 to 2021 in the Home Mortgage Disclosure Act (HMDA) data with property-level flood risk data from CoreLogic and nationwide FEMA flood maps that we digitized for the exercises in the paper. The granularity allows us to study risk and lending in more detail than has previously been possible.

We consider a property to be missing a flood zone designation on a FEMA map (or to be “unmapped”) if it is at a higher risk than half of all properties with non-zero flood risk but it is not covered by a FEMA flood map (either a 100-year flood, 500-year flood, or floodway map). We consider a property “possibly unmapped” if it faces any non-zero flood risk without flood map coverage.

Many properties with flood risk are indeed covered by a flood map, including most of the properties with the highest possible risk. However, a substantial number of properties face flood risk but are not covered by a flood map. Of the properties in the top percentile of the flood risk distribution, a third (36 percent) are not covered by a flood map; in the top five percent of the flood risk distribution, half of all properties (48 percent) are not covered by a flood map; and in the top ten percent of the flood risk distribution, three-quarters (74 percent) are not covered by a flood map.

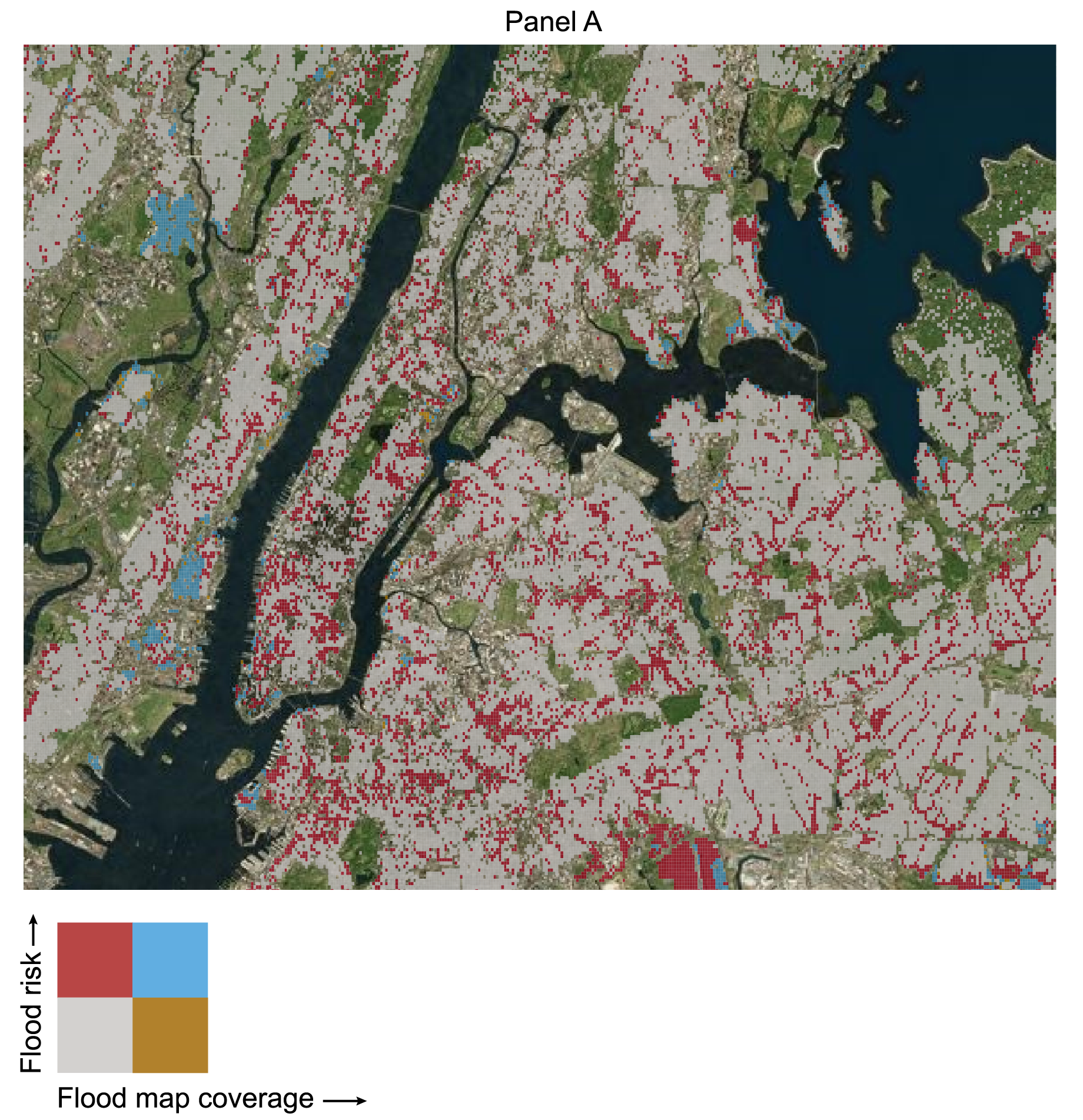

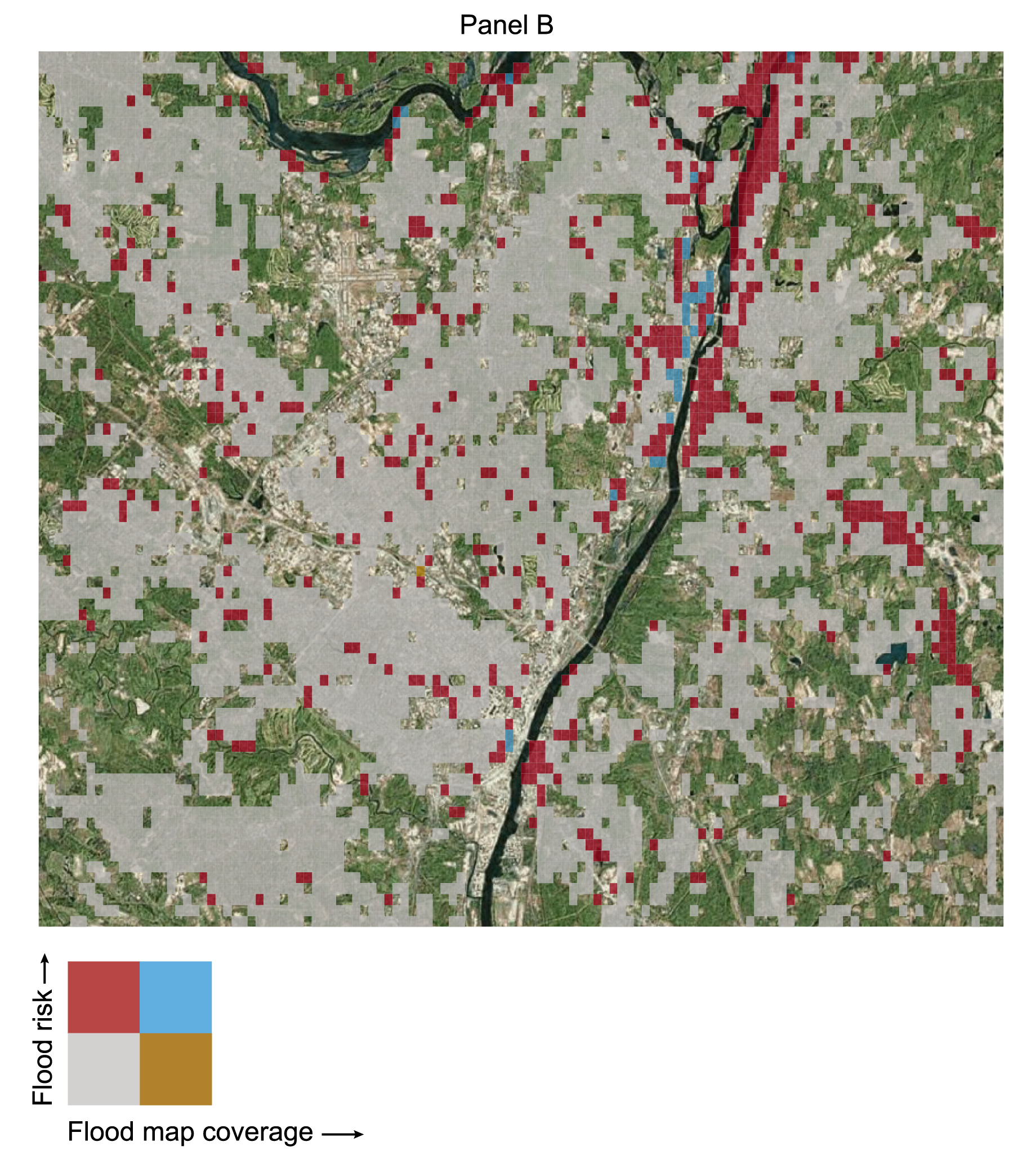

The maps below provide an example of these properties with unmapped flood risk in two areas within the Federal Reserve’s Second District. Panel A maps New York City and the surrounding metropolitan area, and Panel B maps a portion of the Hudson River as it passes through the cities of Albany and Troy, New York. For each map, we overlay a grid and color the cells according to flood map coverage and the average flood risk of properties in the cell. Unmapped areas, with flood risk but no flood map coverage, appear in red. Our analysis focuses on studying lending differences between those properties with high flood risk and no flood map (the red cells) and those properties with low flood risk and no flood map (the gray cells).

Unmapped Flood Risk in the Federal Reserve’s Second District

Sources: Authors’ calculations; FEMA; CoreLogic; Esri.

Notes: Panel A shows flood map coverage and flood risk in a 0.001⁰ × 0.001⁰ grid over New York City. Panel B shows flood map coverage and flood risk in a 0.0025⁰ × 0.0025⁰ grid over Albany and Troy, New York. Only grid cells that cover at least three properties in the data set used in the analysis are colored. The data set includes only residential properties. Gray regions have low flood risk and no flood map coverage. Red regions have flood risk but no flood map coverage. Blue regions are accurately mapped. In the analysis, mortgage origination for properties in gray regions are compared to properties in red regions.

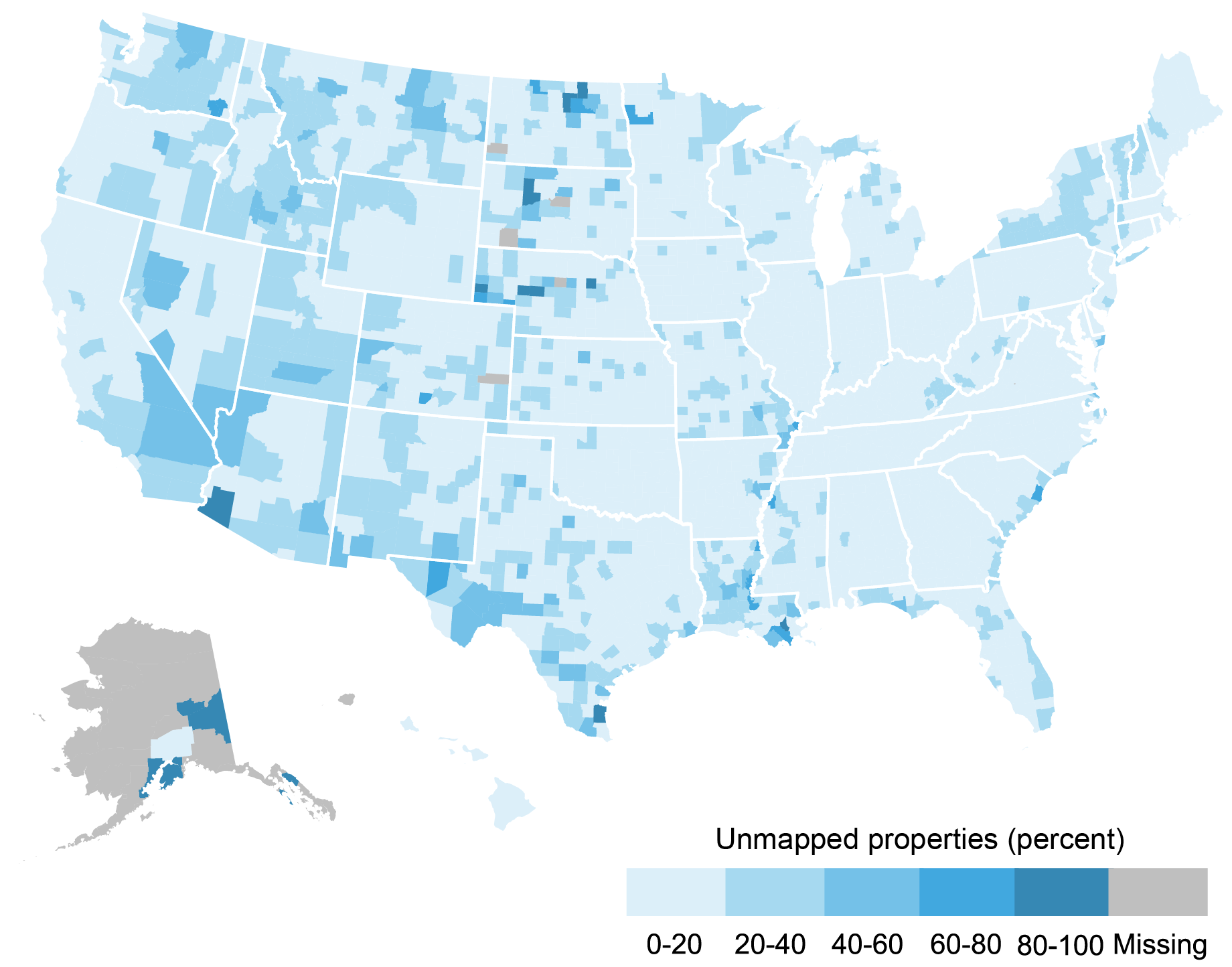

In the map below, we plot the distribution of unmapped properties across the U.S. at the county level. This shows the share of all properties in a county that we identify as having unmapped flood risk. As can be seen, unmapped properties can be found throughout the country—especially along coasts, major rivers, and meltwater runoff paths.

Unmapped Flood Risk Nationwide

Sources: Authors’ calculations; FEMA; CoreLogic.

Notes: The map shows, at the county level, the share of properties classified as having unmapped flood risk.

In our analyses, we study whether mortgage lenders are aware of unmapped flood risk at the property level and whether they respond to this risk accordingly. We restrict our mortgage-property sample to only those primary structures on a parcel we can accurately match to geocoded HMDA data, only mortgage applications made with the purpose of buying a home, and only loans within the local conforming loan limit. Further, we exclude properties covered by a FEMA flood map to focus on comparing similar properties, bought by similar applicants, within the same small census tract—differenced by whether the structure faces flood risk. Our remaining sample contains more than thirteen million mortgage applications.

Less Lending in Risky Areas

We first relate mortgage origination decisions to a host of applicant, bank, and region characteristics. Our variable of interest is whether the property itself is unmapped. We look at the broader “possibly unmapped” as well as the more certain “unmapped.” These categories are cumulative in that all “unmapped” properties are automatically “possibly unmapped” as well.

Effect of Unmapped Flood Risk on Mortgage Originations

Percentage point decrease in originations

Notes: The above figure shows the key coefficients of our regression analysis that relates loan and borrower characteristics to whether or not a loan is originated. It depicts the impact of households being fully or “possibly” un-mapped. The impacts of being un-mapped or possibly un-mapped are cumulative. As we go from specification 1 to specification 4, we include additional controls. Specification 1 includes basic lender controls and county characteristics; Specification 2 adds loan controls including loan size. Specification 3 includes all the above and adds county × time fixed effects, accounting for any time-varying trends at the county level. Finally, specification 4 includes census tract and lender controls. Specification 4 subsumes all lending responses that occur at the tract-level.

We can see from the chart that mortgages are less likely to be originated if the property faces unmapped risk. In fact, all else equal, an unmapped property is about 1 percentage point less likely to have a mortgage originated than properties not at risk (specifications 1 and 2). If we compare properties within a census tract as opposed to wider geographic areas, the effect is diminished (specification 4). It seems that while banks manage flood risk, some banks take a census tract-level—as opposed to a property-level—approach to flood risk management.

We can include interactions with bank-type or region-type dummies. First, we use local incomes as a measure to split our sample into three groups of census tracts (low, mid, and high income). We find that high-income tracts suffer a less severe reduction in lending. This likely reflects the fact that lenders expect wealthy borrowers to better (financially) weather a storm or a flooding disaster. The effects are much more pronounced in regions with lower income (approximately twice as large as the baseline effect). Second, we look at whether different types of entities are likely to lend despite the risk. We find that nonbanks and local banks are still originating loans even if properties face flood risk. Very large banks are less likely to lend.

It is possible that large banks have more sophisticated risk management approaches than smaller banks or nonbanks, which allows them to identify at-risk properties more accurately. Therefore, we additionally look at whether banks sold or securitized loans. We find that lenders are generally more likely to securitize or sell properties that face unmapped flood risk. While the average lender is 1 percentage point more likely to securitize properties with unmapped risk, there are significant differences between lender types. In general, small local banks are more than 2 percentage points more likely to sell or securitize a loan with unmapped flood risk. Given the generally high propensity of these lenders to securitize conforming properties, even a small increase represents significant additional effort on the part of lenders to move the loans off of their balance sheets.

Summing Up

We create a novel property-level flood risk and mortgage application data set to show that lenders are aware of flood risk outside of FEMA flood zones. Larger lenders significantly cut lending while smaller local banks and nonbank entities do not reduce lending but instead are more likely to securitize or sell loans and move them off of their balance sheets.

Kristian Blickle is a financial research economist in Climate Risk Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Evan Perry is a research analyst in the Federal Reserve Bank of New York’s Research and Statistics Group.

João A.C. Santos is the director of Financial Intermediation Policy Research in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Kristian Blickle, Evan Perry, and João A.C. Santos, “Flood Risk Outside Flood Zones — A Look at Mortgage Lending in Risky Areas,” Federal Reserve Bank of New York Liberty Street Economics, September 25, 2024, https://libertystreeteconomics.newyorkfed.org/2024/09/flood-risk-outside-flood-zones-a-look-at-mortgage-lending-in-risky-areas/

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics