The Federal Reserve (Fed) implements monetary policy in a regime of ample reserves, whereby short-term interest rates are controlled mainly through the setting of administered rates. To do so, the quantity of reserves in the banking system needs to be large enough that everyday changes in reserves do not cause large variations in the policy rate, the so-called federal funds rate. As the Fed shrinks its balance sheet following the plan laid out by the Federal Open Market Committee (FOMC) in 2022, how can it assess when to stop so that the supply of reserves remains ample? In the first post of a two-part series, based on the methodology developed in our recent Staff Report, we propose to assess the ampleness of reserves in real time by estimating the slope of the reserve demand curve.

Ample Reserves and the Slope of the Reserve Demand Curve

What does “ample reserves” mean? Based on this FOMC announcement from 2019, we can interpret the notion of ample reserves in terms of the elasticity of the federal (fed) funds rate to changes in the supply of reserves: reserves are ample when the supply of reserves is sufficiently large that the fed funds rate—the price at which banks are willing to trade reserves with one another—is not materially sensitive to everyday changes in aggregate reserves. In other words, in an ample reserve regime, the fed funds rate can respond to daily shocks, but the response must be small; or, to put it differently, the elasticity of the fed funds rate to reserve shocks must be small, so that active management of the supply of reserves by the Fed is not necessary.

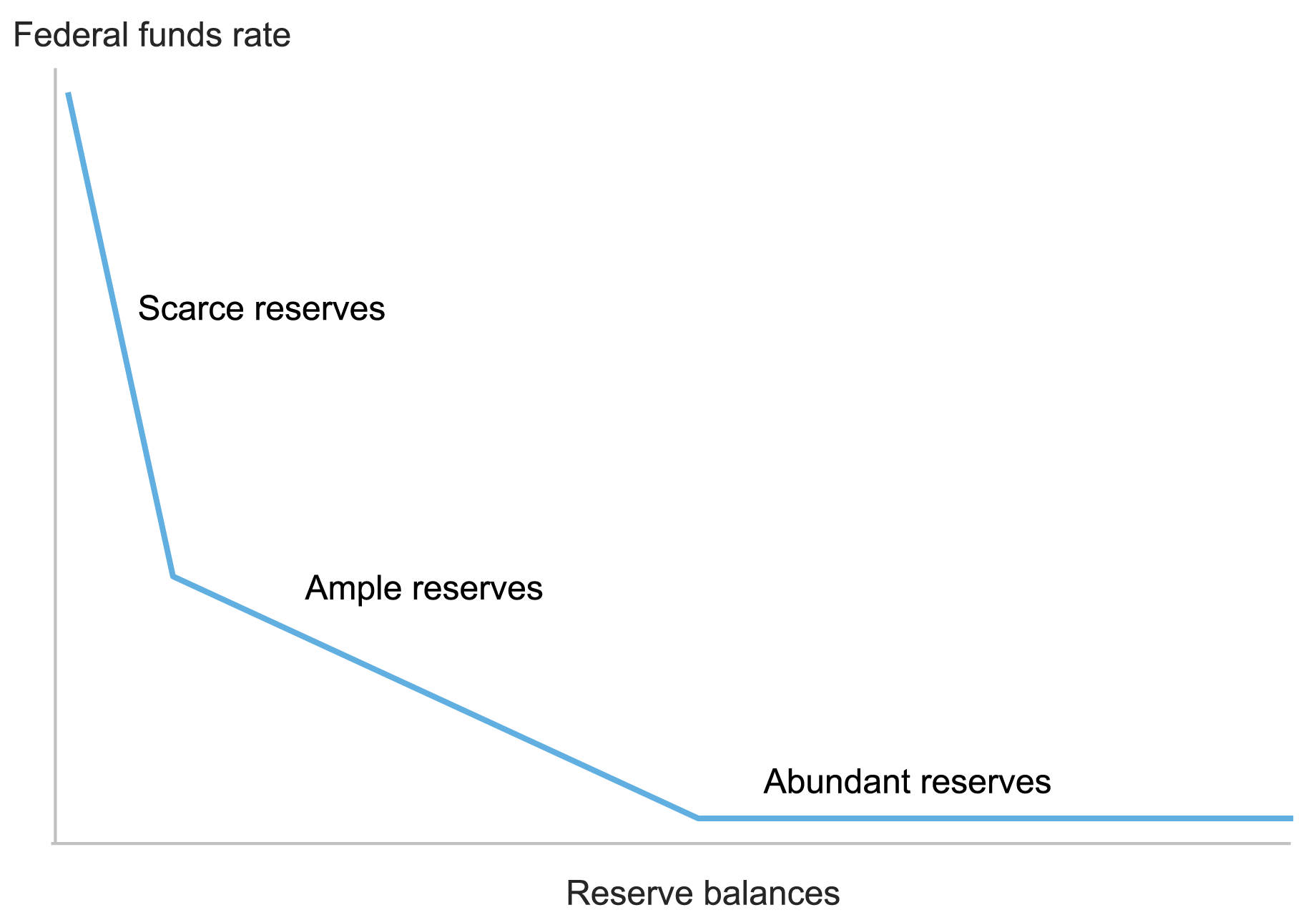

The question is then: what does the level of aggregate reserves have to do with the elasticity of the fed funds rate to reserve shocks? The answer is that this elasticity depends on the quantity of reserves in the banking system through the so-called reserve demand curve, which describes the relationship between the fed funds rate and aggregate reserves that stems from banks’ demand for reserves. The elasticity of the fed funds rate to reserve shocks, in fact, is simply the slope of this curve: it tells us by how much the fed funds rate changes in response to a small shift in reserve supply. The point here is that the slope of the reserve demand curve becomes steeper as reserves decline.

As the chart below shows, above a given reserve level, banks’ demand is “satiated:” in this region of abundant reserves, the slope of the reserve demand curve is zero, and the fed funds rate does not respond to changes in the supply of reserves. That is, above the satiation level, the curve is flat. Below this level, there is an increasingly negative relationship between price and quantity: as the supply of reserves declines, we first move into a region of ample reserves—where the demand curve is gently sloped, and the elasticity of the fed funds rate is negative but small—and then into a region of scarce reserves—where the curve is steeply sloped, and the elasticity is negative and large.

The Slope of the Reserve Demand Curve Reflects Reserve Ampleness by Measuring the Elasticity of the Fed Funds Rate to Reserve Shocks

Source: Authors’ rendering.

Maintaining Ample Reserves

One way to ensure that reserves remain ample is for the Fed to supply reserves close to the transition point between the flat and the gently sloped portions of the demand curve. Identifying the transition point from abundant to ample reserves, however, is challenging because banks’ demand for reserves fluctuates over time and, in turn, the supply of reserves may respond to sudden changes in banks’ demand.

As we explain in an earlier post and in more detail in our paper, we propose an econometric methodology that addresses these challenges. In a nutshell, we use the expansions and contractions of the Fed’s balance sheet over the past fifteen years to move along the demand curve and, every day, estimate its slope at the level of reserves attained on that day. One advantage of our approach is that it is model-free: we do not need to specify a model of the demand for reserves.

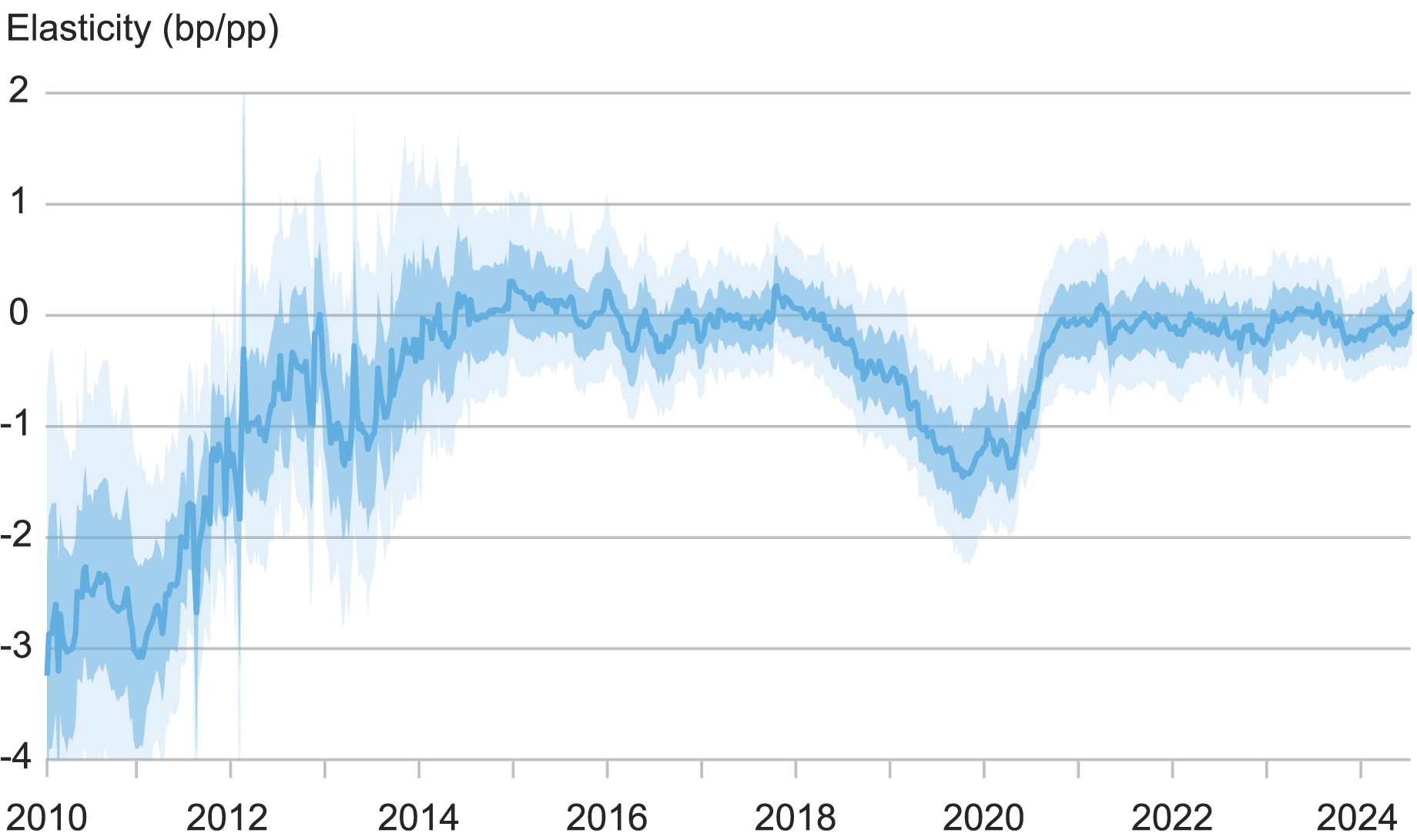

Another important advantage of our approach is that our time-varying methodology can be used in real time to monitor reserve ampleness. The chart below shows our “real-time” daily estimates of the slope of the reserve demand curve, from January 2010 to July 2024: these estimates are obtained using only information available as of each day, making them equivalent to real-time calculations.

The estimated slope was significantly negative in 2010-11 but trended toward zero as the Fed injected large amounts of reserves into the banking system in response to the Global Financial Crisis. During 2012-17 and from mid-2020 onward, as reserves exceeded 13 percent of bank assets, the estimated slope was again very close to zero, indicating an abundance of reserves. In 2018-19, however, the slope became increasingly negative, consistent with reserves first becoming ample and then approaching scarcity. In particular, our estimates reach a minimum in September 2019, consistent with the interpretation that the money-market stress that occurred at the time was, at least in part, related to reserve scarcity.

Our Daily Estimates of the Slope of the Reserve Demand Curve Track Reserve Ampleness in Real Time

Sources: Daily data on reserves and the fed funds rate are collected by the Federal Reserve Bank of New York; the daily interest rate on reserve balances is available from FRED (“IOER” and “IORB”).

Notes: Real-time daily estimates of the slope of the reserve demand curve covering January 2010-July 2024, from Afonso, Giannone, La Spada, and Williams (2022). The slope represents the elasticity of the fed funds rate to shocks in the supply of reserves: it shows by how many basis points the fed funds rate would change for an increase in aggregate reserves equal to 1 percent of banks’ total assets. The solid line represents the median estimate; the dark and light shaded areas represent the 68 percent and 95 percent confidence sets, respectively.

To construct an early-warning signal, one can look at when our real-time estimates of the slope become negative at a given confidence level. For example, our real-time estimates became statistically different from zero at the 95 percent level in early March 2019—six months in advance of the money-market stress of September 2019. To be even more conservative, one could use a lower confidence level: our estimates, for example, became negative at the 68 percent confidence level in August 2018, more than a full year ahead of September 2019.

Summing Up

Since the Global Financial Crisis, many central banks have decided to implement monetary policy by operating close to the satiation point of the reserve demand curve, where the slope is zero or mildly negative, and reserves transition from being abundant to ample. Assessing the ampleness of reserves in real time has therefore become a key objective across many jurisdictions. In today’s post, we discuss using real-time estimates of the slope of the reserve demand curve as an early indicator of reserve ampleness. In tomorrow’s post, we will propose a suite of indicators that, jointly with our measure of elasticity, can help policymakers achieve this challenging objective.

Gara Afonso is the head of Banking Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Domenico Giannone is an assistant director at the International Monetary Fund and an affiliate professor at the University of Washington.

Gabriele La Spada is a financial research advisor in Money and Payments Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

John C. Williams is the president and chief executive officer of the Federal Reserve Bank of New York.

How to cite this post:

Gara Afonso, Domenico Giannone, Gabriele La Spada, and John C. Williams , “When Are Central Bank Reserves Ample? ,” Federal Reserve Bank of New York Liberty Street Economics, August 13, 2024, https://libertystreeteconomics.newyorkfed.org/2024/08/when-are-central-bank-reserves-ample/

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics