260 posts on "Financial Institutions"

December 22, 2025

A New Public Data Source: Call Reports from 1959 to 2025

Call Reports are regulatory filings in which commercial banks report their assets, liabilities, income, and other information. They are one of the most-used data sources in banking and finance. In this post, we describe a new dataset made available on the Federal Reserve Bank of New York’s website that contains time-consistent balance sheets and income statements for commercial banks in the United States from 1959 to 2025.

December 17, 2025

Letters of Recommendation in the PhD Job Market: Lessons from Specialized Banks

Banks must extract useful signals of a potential borrower’s quality from a large set of possibly informative characteristics when making lending decisions. A model that speaks to how banks specialize in lending to an industry in order to better extract signals from data can potentially be applied to a number of real-world scenarios. In this post, we apply lessons from such a model to a topic of timely relevance in economics: job market recommendation letters. Institutions looking to hire new economists must evaluate PhD applicants based on limited and often noisy signals of future performance, including letters of recommendation from these applicants’ advisors or co-authors. Using insights from our model, we argue that the value of these letters depends on who reads them.

November 18, 2025

Banks Develop a Nonbank Footprint to Better Manage Liquidity Needs

In a previous post, we documented how, over the past five decades, the typical U.S. bank has evolved from an entity mainly focused on deposit taking and loan making to a more diversified conglomerate also incorporating a variety of nonbank activities. In this post, we show that an important driver of the evolution of this new organizational form is the desire of banks to efficiently manage liquidity needs.

November 4, 2025

Banking System Vulnerability: 2025 Update

As in previous years, we provide in this post an update on the vulnerability of the U.S. banking system based on four analytical models that capture different aspects of this vulnerability. We use data through 2025:Q2 for our analysis, and also discuss how the vulnerability measures have changed since our last update one year ago.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Liquidity, Systemic Risk | Permalink

September 22, 2025

Financial Intermediaries and Pressures on International Capital Flows

Global factors, like monetary policy rates from advanced economies and risk conditions, drive fluctuations in volumes of international capital flows and put pressure on exchange rates. The components of international capital flows that are described as global liquidity—consisting of cross-border bank lending and financing of issuance of international debt securities—have sensitivities to risk conditions that have evolved considerably over time. This risk sensitivity has been driven, in part, by the composition and business models of the financial institutions involved in funding. In this post, we ask whether these same features have led to changes in the pressures on currency values as risk conditions evolve. Using the Goldberg and Krogstrup (2023) Exchange Market Pressure (EMP) country indices, we show that the features of financial institutions in the source countries for international capital do influence how destination countries experience currency pressures when risk conditions change. Better shock-absorbing capacity in financial institutions moderates the pressures toward depreciation of currencies during adverse global risk events.

Posted at 7:00 am in Bank Capital, Exchange Rates, Financial Institutions, International Economics, Systemic Risk | Permalink

July 10, 2025

The Rise in Deposit Flightiness and Its Implications for Financial Stability

Deposits are often perceived as a stable funding source for banks. However, the risk of deposits rapidly leaving banks—known as deposit flightiness—has come under increased scrutiny following the failures of Silicon Valley Bank and other regional banks in March 2023. In a new paper, we show that deposit flightiness is not constant over time. In particular, flightiness reached historic highs after expansions in bank reserves associated with rounds of quantitative easing (QE). We argue that this elevated deposit flightiness may amplify the banking sector’s response to subsequent monetary policy rate hikes, highlighting a link between the Federal Reserve’s balance sheet and conventional monetary policy.

July 8, 2025

The Fed’s Treasury Purchase Prices During the Pandemic

In March 2020, the Federal Reserve commenced purchases of U.S. Treasury securities to address the market disruptions caused by the pandemic. This post assesses the execution quality of those purchases by comparing the Fed’s purchase prices to contemporaneous market prices. Although past work has considered this question in the context of earlier asset purchases, the market dysfunction spurred by the pandemic means that execution quality at that time may have differed. Indeed, we find that the Fed’s execution quality was unusually good in 2020 in that the Fed bought Treasuries at prices appreciably lower than prevailing market offer prices.

December 20, 2024

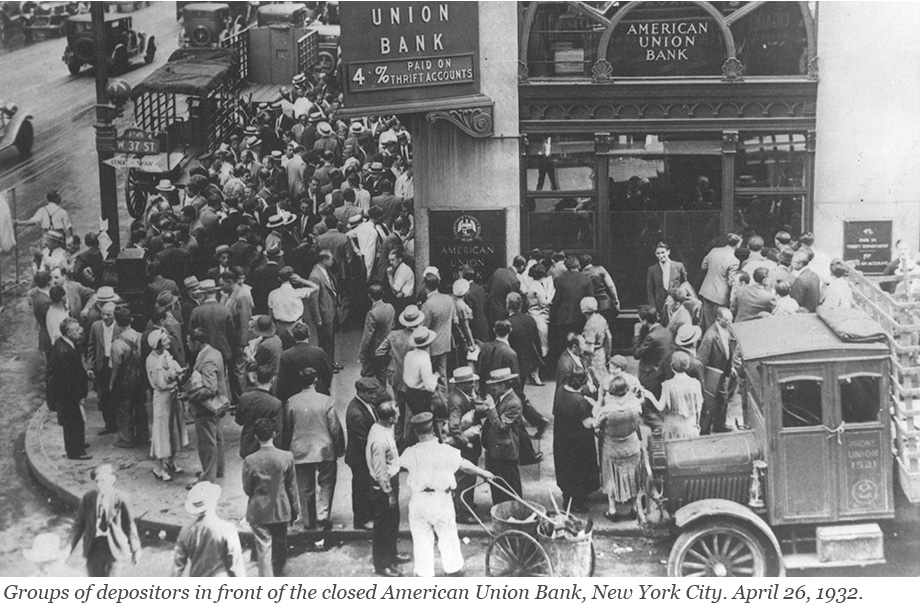

Anatomy of the Bank Runs in March 2023

Runs have plagued the banking system for centuries and returned to prominence with the bank failures in early 2023. In a traditional run—such as depicted in classic photos from the Great Depression—depositors line up in front of a bank to withdraw their cash. This is not how modern bank runs occur: today, depositors move money from a risky to a safe bank through electronic payment systems. In a recently published staff report, we use data on wholesale and retail payments to understand the bank run of March 2023. Which banks were run on? How were they different from other banks? And how did they respond to the run?

Posted at 6:30 am in Banks, Crisis, Financial Institutions, Lender of Last Resort, Panic | Permalink | Comments (1)

December 3, 2024

Documenting Lender Specialization

Robust banks are a cornerstone of a healthy financial system. To ensure their stability, it is desirable for banks to hold a diverse portfolio of loans originating from various borrowers and sectors so that idiosyncratic shocks to any one borrower or fluctuations in a particular sector would be unlikely to cause the entire bank to go under. With this long-held wisdom in mind, how diversified are banks in reality?

November 25, 2024

Why Do Banks Fail? Bank Runs Versus Solvency

Evidence from a 160-year-long panel of U.S. banks suggests that the ultimate cause of bank failures and banking crises is almost always a deterioration of bank fundamentals that leads to insolvency. As described in our previous post, bank failures—including those that involve bank runs—are typically preceded by a slow deterioration of bank fundamentals and are hence remarkably predictable. In this final post of our three-part series, we relate the findings discussed previously to theories of bank failures, and we discuss the policy implications of our findings.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics