99 posts on "Inequality"

July 8, 2020

Do College Tuition Subsidies Boost Spending and Reduce Debt? Impacts by Income and Race

In an October post, we showed the effect of college tuition subsidies in the form of merit-based financial aid on educational and student debt outcomes, documenting a large decline in student debt for those eligible for merit aid. Additionally, we reported striking differences in these outcomes by demographics, as proxied by neighborhood race and income. In this follow-up post, we examine whether and how this effect passes through to other debt and consumption outcomes, namely those related to autos, homes, and credit cards. We find that access to merit aid leads to an immediate but temporary increase in eligible individuals’ consumption in these categories. The increase is followed by a decline in consumption and a reduction in total debt of these types in the longer term. Importantly, there are marked differences in these consumption and debt patterns across groups, as evident when we introduce proxies for demographic group using the income and racial composition of the students’ home neighborhoods of origin.

Measuring Racial Disparities in Higher Education and Student Debt Outcomes

Across the United States, the cost of all types of higher education has been rising faster than overall inflation for more than two decades. Despite rising costs, aggregate undergraduate enrollment rose steadily between 2000 and 2010 before leveling off and dipping slightly to its current level. Rising college costs have steadily increased dependence on student debt for college financing, with many students and parents turning to federal and private loans to pay for higher education. An earlier post in this series reported that borrowers in majority Black areas have higher student loan balances and rates of default than those in both majority white and majority Hispanic areas. In this post, we study how differences in college attendance rates and in the types of colleges attended generate heterogeneity in loan experiences. Specifically, using nationwide data, we analyze heterogeneities in college-going and heterogeneities in student debt and default experiences by college type across individuals living in majority Black, majority Hispanic, and majority white zip codes.

Posted at 7:30 am in Education, Equitable Growth, Household Finance, Inequality, Student Loans | Permalink

Who Has Been Evicted and Why?

More than two million American households are at risk of eviction every year. Evictions have been found to cause prolonged homelessness, worsened health conditions, and lack of credit access. During the COVID-19 outbreak, governments at all levels implemented eviction moratoriums to keep renters in their homes. As these moratoriums and enhanced income supports for unemployed workers come to an end, the possibility of a wave of evictions in the second half of the year is drawing increased attention. Despite the importance of evictions and related policies, very few economic studies have been done on this topic. With the exception of the Milwaukee Area Renters Study, evictions are rarely measured in economic surveys. To fill this gap, we conducted a novel national survey on evictions within the Housing Module of the Survey of Consumer Expectations (SCE) in 2019 and 2020. This post describes our findings.

Inequality in U.S. Homeownership Rates by Race and Ethnicity

Homeownership has historically been an important means for Americans to accumulate wealth—in fact, at more than $15 trillion, housing equity accounts for 16 percent of total U.S. household wealth. Consequently, the U.S. homeownership cycle has triggered large swings in Americans’ net worth over the past twenty-five years. However, the nature of those swings has varied significantly by race and ethnicity, with different demographic groups tracing distinct trajectories through the housing boom, the foreclosure crisis, and the subsequent recovery. Here, we look into the dynamics underlying these divergences and explore some potential explanations.

July 7, 2020

Introduction to Heterogeneity Series III: Credit Market Outcomes

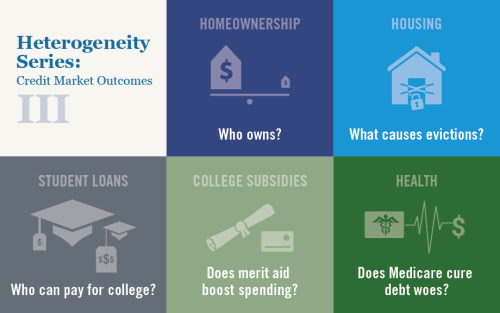

Following up series on heterogeneity and inequality broadly and in labor market outcomes specifically, we turn our focus to further documenting heterogeneity in credit market outcomes, looking at disparities in home ownership rates, varying exposure to evictions, differing gains from tuition support and Medicare programs, and more.

June 15, 2020

Distribution of COVID‑19 Incidence by Geography, Race, and Income

In this post, we study whether (and how) the spread of COVID-19 across the United States varied by geography, race, income, and population density. Were urban areas more affected by COVID-19 than rural areas? Did population density matter in the spread? Were certain races and income groups affected more by the spread of this deadly coronavirus? Our analysis uncovers stark demographic trends among places affected most severely by the pandemic thus far.

March 4, 2020

How Does Credit Access Affect Job‑Search Outcomes and Sorting?

The analysis considers how access to consumer credit influences the job search behavior of displaced workers.

Is the Tide Lifting All Boats? A Closer Look at the Earnings Growth Experiences of U.S. Workers

Although there is evidence that U.S. workers at the bottom of the earnings distribution may be catching up with those at the top, there are indications that returns to higher education may be increasing, with earnings growth for college graduates outpacing those with less education.

Women Have Been Hit Hard by the Loss of Routine Jobs, Too

Jaison Abel and Richard Deitz find that although both men and women have experienced a loss of routine jobs since 2000, the decline has been markedly steeper for women.

March 3, 2020

Introduction to Heterogeneity Series II: Labor Market Outcomes

Rajashri Chakrabarti introduces a new Liberty Street Economics series exploring dimensions of heterogeneity in the labor market experience of U.S. workers.

Posted at 7:00 am in Human Capital, Inequality, Labor Market, Regional Analysis, Unemployment | Permalink | Comments (2)

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics