22 posts on "Marco Cipriani"

June 23, 2025

Reserves and Where to Find Them

Banks use central bank reserves for a multitude of purposes including making payments, managing intraday liquidity outflows, and meeting regulatory and internal liquidity requirements. Data on aggregate reserves for the U.S. banking system are readily accessible, but information on the holdings of individual banks is confidential. This makes it difficult to investigate important questions like: “Which types of banks hold reserves?” “How concentrated are they?” and “Does the distribution change over time or in response to significant events?” In this post, we summarize how non-confidential data can be used to answer these questions by providing publicly available proxies for bank-level reserves.

April 23, 2025

Stablecoins and Crypto Shocks: An Update

Stablecoins are crypto assets whose value is pegged to that of a fiat currency, usually the U.S. dollar. In our first Liberty Street Economics post, we described the rapid growth of stablecoins, the different types of stablecoin arrangements, and the May 2022 run on TerraUSD, the fourth largest stablecoin at the time. In a subsequent post, we estimated the impact of large declines in the price of bitcoin on cumulative net flows into stablecoins and showed the existence of flight-to-safety dynamics similar to those observed in money market mutual funds during periods of stress. In this post, we document the growth of stablecoins since 2019, including the evolution of the reported collateral backing major stablecoins. Then, we estimate the impact on the stablecoin industry of large bitcoin price increases that occurred between 2021 and 2025.

December 20, 2024

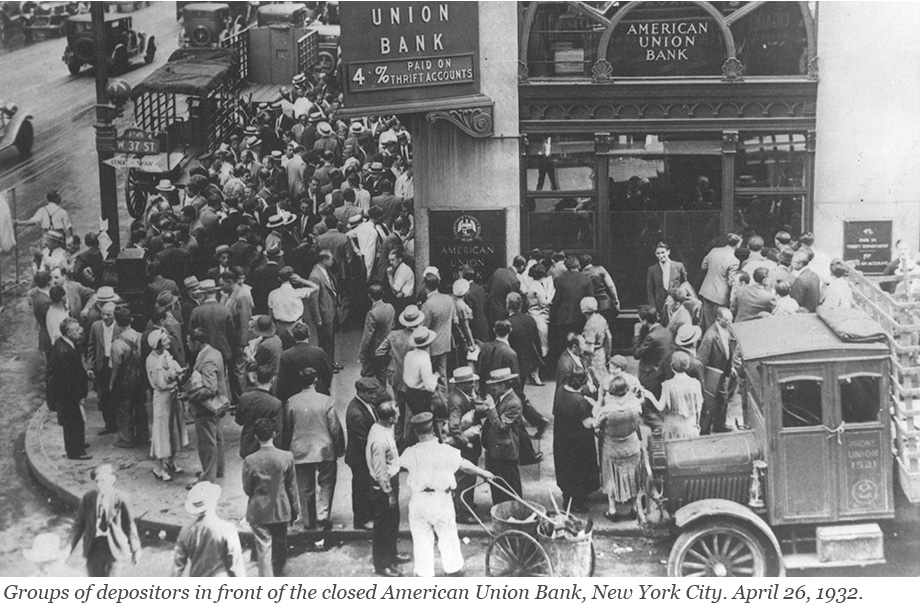

Anatomy of the Bank Runs in March 2023

Runs have plagued the banking system for centuries and returned to prominence with the bank failures in early 2023. In a traditional run—such as depicted in classic photos from the Great Depression—depositors line up in front of a bank to withdraw their cash. This is not how modern bank runs occur: today, depositors move money from a risky to a safe bank through electronic payment systems. In a recently published staff report, we use data on wholesale and retail payments to understand the bank run of March 2023. Which banks were run on? How were they different from other banks? And how did they respond to the run?

Posted at 6:30 am in Banks, Crisis, Financial Institutions, Lender of Last Resort, Panic | Permalink | Comments (1)

March 8, 2024

Stablecoins and Crypto Shocks

In a previous post, we described the rapid growth of the stablecoin market over the past few years and then discussed the TerraUSD stablecoin run of May 2022. The TerraUSD run, however, is not the only episode of instability experienced by a stablecoin. Other noteworthy incidents include the June 2021 run on IRON and, more recently, the de-pegging of USD Coin’s secondary market price from $1.00 to $0.88 upon the failure of Silicon Valley Bank in March 2023. In this post, based on our recent staff report, we consider the following questions: Do stablecoin investors react to broad-based shocks in the crypto asset industry? Do the investors run from the entire stablecoin industry, or do they engage in a flight to safer stablecoins? We conclude with some high-level discussion points on potential regulations of stablecoins.

December 19, 2023

Dropping Like a Stone: ON RRP Take‑up in the Second Half of 2023

Take-up at the Overnight Reverse Repo Facility (ON RRP) has halved over the past six months, declining by more than $1 trillion since June 2023. This steady decrease follows a rapid increase from close to zero in early 2021 to $2.2 trillion in December 2022, and a period of relatively stable balances during the first half of 2023. In this post, we interpret the recent drop in ON RRP take-up through the lens of the channels that we identify in our recent Staff Report as driving its initial increase.

August 14, 2023

The Federal Reserve’s Two Key Rates: Similar but Not the Same?

Since the global financial crisis, the Federal Reserve has relied on two main rates to implement monetary policy—the rate paid on reserve balances (IORB rate) and the rate offered at the overnight reverse repo facility (ON RRP rate). In this post, we explore how these tools steer the federal funds rate within the Federal Reserve’s target range and how effective they have been at supporting rate control.

August 10, 2023

The Evolution of Short‑Run r* after the Pandemic

This post discusses the evolution of the short-run natural rate of interest, or short-run r*, over the past year and a half according to the New York Fed DSGE model, and the implications of this evolution for inflation and output projections. We show that, from the model’s perspective, short-run r* has increased notably over the past year, to some extent outpacing the large increase in the policy rate. One implication of these findings is that the drag on the economy from recent monetary policy tightening may have been limited, rationalizing why economic conditions have remained relatively buoyant so far despite the elevated level of interest rates.

July 12, 2023

Runs on Stablecoins

Stablecoins are digital assets whose value is pegged to that of fiat currencies, usually the U.S. dollar, with a typical exchange rate of one dollar per unit. Their market capitalization has grown exponentially over the last couple of years, from $5 billion in 2019 to around $180 billion in 2022. Notwithstanding their name, however, stablecoins can be very unstable: between May 1 and May 16, 2022, there was a run on stablecoins, with their circulation decreasing by 15.58 billion and their market capitalization dropping by $25.63 billion (see charts below.) In this post, we describe the different types of stablecoins and how they keep their peg, compare them with money market funds—a similar but much older and more regulated financial product, and discuss the stablecoin run of May 2022.

May 18, 2023

Banks’ Balance‑Sheet Costs and ON RRP Investment

Daily investment at the Federal Reserve’s Overnight Reverse Repo (ON RRP) facility increased from a few billion dollars in March 2021 to more than $2.3 trillion in June 2022 and has stayed above $2 trillion since then. In this post, which is based on a recent staff report, we discuss two channels—a deposit channel and a wholesale short-term debt channel—through which banks’ balance-sheet costs have increased investment by money market mutual funds (MMFs) in the ON RRP facility.

April 14, 2023

Mitigating the Risk of Runs on Uninsured Deposits: the Minimum Balance at Risk

The incentives that drive bank runs have been well understood since the seminal work of Nobel laureates Douglas Diamond and Philip Dybvig (1983). When a bank is suspected to be insolvent, early withdrawers can get the full value of their deposits. If and when the bank runs out of funds, however, the bank cannot pay remaining depositors. As a result, all depositors have an incentive to run. The failures of Silicon Valley Bank and Signature Bank remind us that these incentives are still present for uninsured depositors, that is, those whose bank deposits are larger than deposit insurance limits. In this post, we discuss a policy proposal to reduce uninsured depositors’ incentives to run.

Posted at 7:00 am in Bank Capital, Crisis, Financial Intermediation, International Economics | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics