10 posts on "Thomas Eisenbach"

November 4, 2025

Banking System Vulnerability: 2025 Update

As in previous years, we provide in this post an update on the vulnerability of the U.S. banking system based on four analytical models that capture different aspects of this vulnerability. We use data through 2025:Q2 for our analysis, and also discuss how the vulnerability measures have changed since our last update one year ago.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Liquidity, Systemic Risk | Permalink

April 23, 2025

Stablecoins and Crypto Shocks: An Update

Stablecoins are crypto assets whose value is pegged to that of a fiat currency, usually the U.S. dollar. In our first Liberty Street Economics post, we described the rapid growth of stablecoins, the different types of stablecoin arrangements, and the May 2022 run on TerraUSD, the fourth largest stablecoin at the time. In a subsequent post, we estimated the impact of large declines in the price of bitcoin on cumulative net flows into stablecoins and showed the existence of flight-to-safety dynamics similar to those observed in money market mutual funds during periods of stress. In this post, we document the growth of stablecoins since 2019, including the evolution of the reported collateral backing major stablecoins. Then, we estimate the impact on the stablecoin industry of large bitcoin price increases that occurred between 2021 and 2025.

December 20, 2024

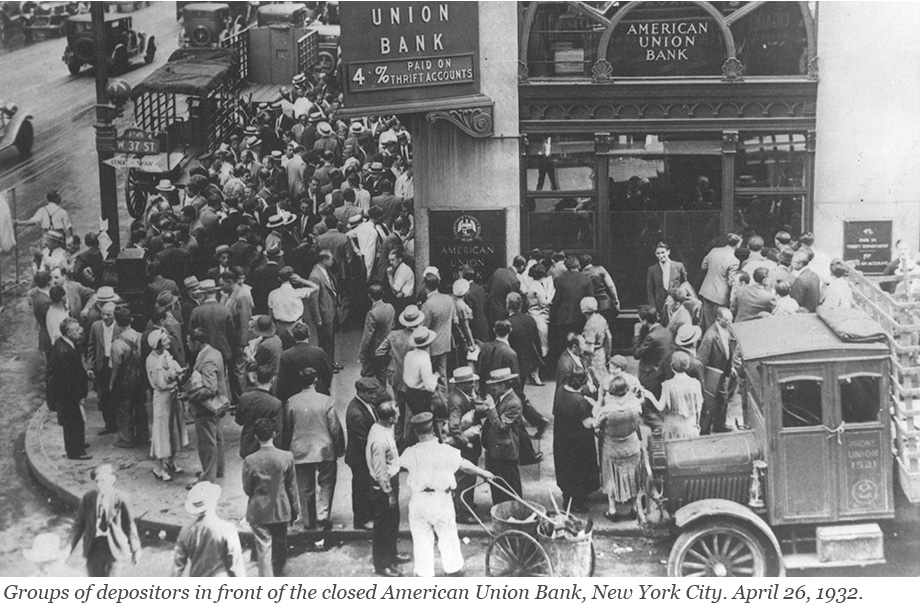

Anatomy of the Bank Runs in March 2023

Runs have plagued the banking system for centuries and returned to prominence with the bank failures in early 2023. In a traditional run—such as depicted in classic photos from the Great Depression—depositors line up in front of a bank to withdraw their cash. This is not how modern bank runs occur: today, depositors move money from a risky to a safe bank through electronic payment systems. In a recently published staff report, we use data on wholesale and retail payments to understand the bank run of March 2023. Which banks were run on? How were they different from other banks? And how did they respond to the run?

Posted at 6:30 am in Banks, Crisis, Financial Institutions, Lender of Last Resort, Panic | Permalink | Comments (1)

March 8, 2024

Stablecoins and Crypto Shocks

In a previous post, we described the rapid growth of the stablecoin market over the past few years and then discussed the TerraUSD stablecoin run of May 2022. The TerraUSD run, however, is not the only episode of instability experienced by a stablecoin. Other noteworthy incidents include the June 2021 run on IRON and, more recently, the de-pegging of USD Coin’s secondary market price from $1.00 to $0.88 upon the failure of Silicon Valley Bank in March 2023. In this post, based on our recent staff report, we consider the following questions: Do stablecoin investors react to broad-based shocks in the crypto asset industry? Do the investors run from the entire stablecoin industry, or do they engage in a flight to safer stablecoins? We conclude with some high-level discussion points on potential regulations of stablecoins.

November 14, 2022

Banking System Vulnerability: 2022 Update

To assess the vulnerability of the U.S. financial system, it is important to monitor leverage and funding risks—both individually and in tandem. In this post, we provide an update of four analytical models aimed at capturing different aspects of banking system vulnerability with data through 2022:Q2, assessing how these vulnerabilities have changed since last year. The four models were introduced in a Liberty Street Economics post in 2018 and have been updated annually since then.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Liquidity, Systemic Risk | Permalink

September 8, 2022

How Can Safe Asset Markets Be Fragile?

The market for U.S. Treasury securities experienced extreme stress in March 2020, when prices dropped precipitously (yields spiked) over a period of about two weeks. This was highly unusual, as Treasury prices typically increase during times of stress. Using a theoretical model, we show that markets for safe assets can be fragile due to strategic interactions among investors who hold Treasury securities for their liquidity characteristics. Worried about having to sell at potentially worse prices in the future, such investors may sell preemptively, leading to self-fulfilling “market runs” that are similar to traditional bank runs in some respects.

November 15, 2021

Banking System Vulnerability through the COVID‑19 Pandemic

More than a year into the COVID-19 pandemic, the U.S. banking system has remained stable and seems to have weathered the crisis well, in part because of effects of the policy actions undertaken during the early stages of the pandemic. In this post, we provide an update of four analytical models that aim to capture different aspects of banking system vulnerability and discuss their perspective on the COVID pandemic. The four models, introduced in a Liberty Street Economics post in November 2018 and updated annually since then, monitor vulnerabilities of U.S. banking firms and the way in which these vulnerabilities interact to amplify negative shocks.

November 10, 2021

How Does Market Power Affect Fire‑Sale Externalities?

An important role of capital and liquidity regulations for financial institutions is to counteract inefficiencies associated with “fire-sale externalities,” such as the tendency of institutions to lever up and hold illiquid assets to the extent that their collective actions increase financial vulnerabilities. However, theoretical models that study such externalities commonly assume perfect competition among financial institutions, in spite of high (and increasing) financial sector concentration. In this post, which is based on our forthcoming article, we consider instead how the effects of fire-sale externalities change when financial institutions have market power.

December 18, 2019

Banking System Vulnerability: Annual Update

A key part of understanding the stability of the U.S. financial system is to monitor leverage and funding risks in the financial sector and the way in which these vulnerabilities interact to amplify negative shocks. In this post, we provide an update of four analytical models, introduced in a Liberty Street Economics post last year, that aim to capture different aspects of banking system vulnerability.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Financial Intermediation, Liquidity, Systemic Risk | Permalink

November 4, 2019

Since the Financial Crisis, Aggregate Payments Have Co‑moved with Aggregate Reserves. Why?

Thomas Eisenbach, Kyra Frye, and Helene Hall take a look at what is driving the strong co-movement between aggregate payments sent over Fedwire and total aggregate reserves following the financial crisis.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics