The Tax Cuts and Jobs Act (TCJA) is expected to increase after-tax profits for most companies, primarily by lowering the top corporate statutory tax rate from 35 percent to 21 percent. At the same time, the TCJA provides less favorable treatment of net operating losses and limits the deductibility of net interest expense. We explain how the latter set of changes may heighten bank and corporate borrower cyclicality by making bank capital and default risk for highly levered corporations more sensitive to economic downturns.

Treatment of Net Operating Losses

Prior to the TCJA, companies were able to carry back net operating losses (NOLs) and receive refunds for taxes paid in the two years before the loss. Those “NOL carrybacks” contributed directly to net income and to regulatory capital for banks. NOLs could also be carried forward to offset 100 percent of taxable income for up to 20 years. The TCJA eliminates NOL carrybacks entirely and reduces carryforward utilization to only 80 percent of taxable income, although the latter will no longer expire after 20 years.

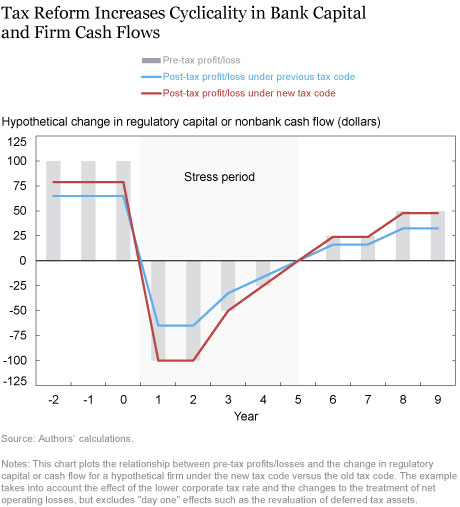

The chart below illustrates the cyclical effects of the new rules on a hypothetical firm with both positive and negative pre-tax income over time. Before, losses would be offset by refunds of taxes paid in the previous years (carrybacks). Now, pre-tax losses immediately result in lower cash flows for firms and lower capital for banks, as deferred tax assets are primarily excluded from common equity Tier 1 capital (see this supervisory guidance for details on the initial accounting effect of the tax law change). The chart illustrates this effect from the larger magnitude of the changes in bank capital under the new code (red line) relative to the old code (blue line). For nonbanks, companies with current losses that were previously profitable may be more likely to default without access to cash from tax refunds. Recoveries may also be slower following a recession, since only 80 percent of taxable income can be shielded with NOLs. However, if pre-tax income is not negative or if a recession is moderate, the impact of the new rules may be muted as the lower tax rate increases after-tax profits.

These concerns in the context of stress-tests were highlighted in a letter from the Federal Reserve’s Board of Governors describing changes to stress test modeling: “the elimination of NOL carrybacks will result in a larger decline in post-stress capital ratios for firms with taxes paid in the two years leading up to the stress test that then experience losses in the stress test…”

Deductibility of Net Interest Expense

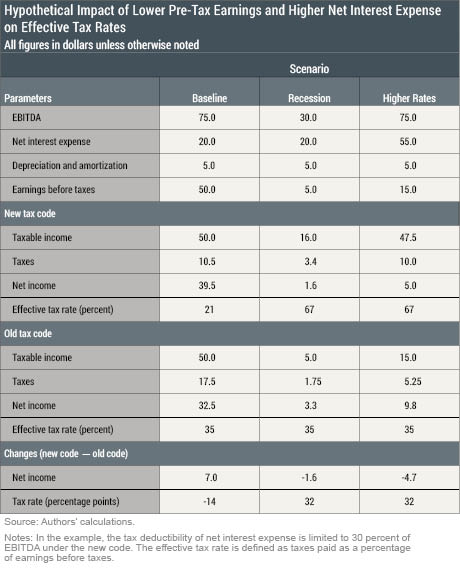

The TCJA also limits the tax deductibility of net interest expense. Through 2021, net interest expense is only deductible up to 30 percent of earnings before interest, taxes, depreciation and amortization (EBITDA). Starting in 2022, net interest expense is only deductible up to 30 percent of earnings before interest and taxes (EBIT). Mitigating these caps is the fact that interest expense above the cap can be carried forward indefinitely. In addition, the caps only apply to U.S. taxes. As a result, international firms may find ways to structure around the caps.

Relative to the old tax code, all else equal, the new limits increase effective tax rates and lower net income when either earnings fall or net interest expense increases. The table below illustrates this effect for a hypothetical firm. In the baseline scenario, net interest expense is below the limit and the effective tax rate under the new code is 21 percent. In the next column, titled “recession,” income falls by more than half and the cap binds, limiting the ability of net interest expense to shield income from taxes. Finally, in the column titled “higher rates,” higher net interest expense results in a higher tax rate. Note that this provision is unlikely to affect banks, as banks tend to earn net interest income rather than pay net interest expense.

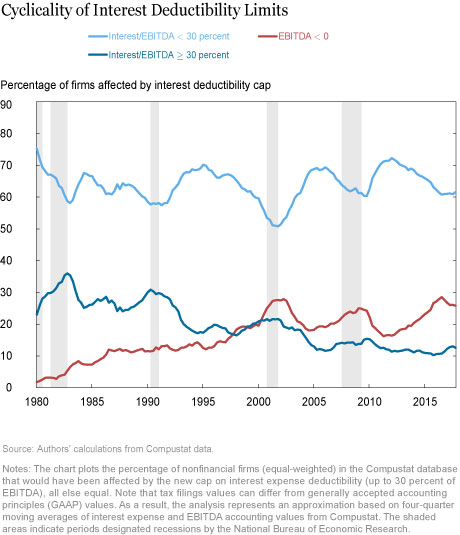

The aggregate, cyclical impact of these limits depends on a number of factors, including the prevalence of highly levered firms, the cyclicality of earnings, the percentage of debt that is fixed versus floating rate, as well as the response of firm leverage to the change in the tax code. At the end of 2017, the fraction of public, nonfinancial firms with interest expense above the EBITDA and EBIT caps and positive earnings was only 12 and 19 percent, respectively, on an equal-weighted basis and 4 and 12 percent, respectively, on a market value-weighted basis, suggesting the impact is relatively small. That said, the caps may become more binding over the business cycle if interest rates increase or if earnings decline in a recession, as shown below. The following chart plots the equal-weighted percentage of nonfinancial firms in the Compustat database affected by the cap on interest expense deductibility from September 1980 to December 2017 to highlight how the share of affected companies changes over the business cycle (the light blue and dark blue lines). However, companies that have negative pre-tax earnings (firms with negative EBITDA) are not affected by the cap because they have no income to shelter from taxes (the red line).

This figure pertains only to public firms, but private companies also rely on leverage, particularly firms acquired in leveraged buyouts. For example, in the high yield bond universe, the EBITDA cap affects most issuers rated BB and below, and the vast majority of CCC-C rated issues.

Market Reaction to the TCJA

Equity markets appear to be pricing in some of these changes. In the chart below, we investigate the reaction of different portfolios of stocks to the TCJA. To the extent that tax reform has a positive (negative) impact on corporate earnings for firms with high tax rates (interest expense ratios), one might expect those firms to outperform (underperform) around the time of the announcement and passage of the bill.

The chart below explores this hypothesis. The red line plots the cumulative excess return of a portfolio that buys stocks with high interest expense ratios and sells stocks with low interest expense ratios. Consistent with the hypothesis, high interest expense firms underperform around the announcement and passage of the bill.

This reaction suggests either that investors expect lower cash flows due to lower deductions or that investors are requiring a higher discount rate as a result of heightened systematic risk for high interest expense firms relative to low interest expense firms. In comparison, the light blue line plots the performance of a portfolio that buys stocks with high tax rates and sells stocks with low tax rates. The outperformance of this portfolio relative to the market suggests that high tax rate firms will differentially benefit from the TCJA relative to low tax rate firms. Taken together, the results highlight how equity investors are responding to the different effects of tax reform on corporate earnings.

Long- and Short-Run Effects

In the short run, if corporate leverage does not change, the new tax code will tend to make bank capital and nonbank defaults more cyclical, particularly in a severe downturn. In the long-run, the increased cyclicality could be mitigated by deleveraging if firms respond to the lower corporate tax rate, new limits on net interest expense deductibility, and heightened cyclicality of after-tax cash flows, which potentially increase the probability of distress. If firms trade off the marginal costs and benefits of debt as in corporate finance theory, optimal leverage for nonbanks should fall under the new tax law. Empirically, the importance of tax changes for aggregate leverage appears to be somewhat limited. Graham, Leary, and Roberts (2015), for example, find a slow response of leverage to tax changes (see Graham (2003) for survey evidence). As of the first quarter of 2018, there is limited evidence of deleveraging, with most corporate financial policies appearing to favor returning cash to shareholders in the form of stock buybacks and dividend payouts.

Disclaimer

The views expressed in this post are those of the authors and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the authors.

Diego Aragon is a capital policy manager in the Federal Reserve Bank of New York’s Supervision Group.

Anna Kovner is a vice president in the Bank’s Research and Statistics Group.

Anna Kovner is a vice president in the Bank’s Research and Statistics Group.

Vanesa Sanchez is a capital policy associate in the Bank’s Supervision Group.

Peter Van Tassel is an economist in the Bank’s Research and Statistics Group.

Peter Van Tassel is an economist in the Bank’s Research and Statistics Group.

How to cite this blog post:

How to cite this blog post:

Diego Aragon, Anna Kovner, Vanesa Sanchez, and Peter Van Tassel, “Tax Reform’s Impact on Bank and Corporate Cyclicality,” Federal Reserve Bank of New York Liberty Street Economics (blog), July 16, 2018, //libertystreeteconomics.newyorkfed.org/2018/06/tax-reforms-impact-on-bank-and-corporate-cyclicality.html.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics

Interesting, so that would seem to imply that there is a growing number of smaller public firms that have negative ebitda. alternatively, that smaller firms losing money have become even smaller as large firms have gotten bigger? Also do you think the growing percentage of public firms that have become passthrough entities rather than c-type corporates?

Alan: Thank you for your interest in the blog post and comment. The trend has been driven by healthcare and in recent years by energy and technology (using the Fama and French 12 industry portfolios to define industries where technology refers to business equipment). However, we see less of a trend and a smaller percentage of negative EBITDA firms on a value-weighted basis. We also don’t see changes in the percentage of public firms with negative EBITDA as related to the tax law changes.

Liked the piece. I thought the cyclicality of interest deductibility graph was interesting, particularly the growing share of nonfin firms with negative ebitda. The falling percent of firms with interest/ebida >30 can at least partly explained by the decline of interest rates over the time period along with falling leverage–as predicted by MMM. So, what do you think explains the rising trend of negative ebitda firms?