On October 10, 2025, the announcement of a potential additional 100 percent tariff on Chinese goods drove risk-off moves across equities, Treasuries, credit spreads, and digital assets. Digital asset prices fell sharply, trading volumes surged, and liquidity vanished from key exchanges. In this post, we show how the price shock in digital assets was transmitted and amplified through a class of instruments called synthetic stablecoins—crypto assets whose structural design turned an external shock into a self-reinforcing deleveraging spiral within the crypto ecosystem.

Synthetic Stablecoins and Perpetual Futures

Synthetic stablecoins differ fundamentally from fiat-asset-backed stablecoins like USD Coin (USDC), which are backed by reserves of dollar-equivalents such as Treasury bills, Treasury-backed reverse repurchase agreements, and bank deposits. Instead, synthetic stablecoins like Ethena (USDe) target their dollar peg through financial engineering: they combine a long position in cryptocurrency (typically ether staked in a staking pool like Lido) with an offsetting short position in perpetual futures contracts. Lido pools together ether deposits, earns yield for participating in Ethereum’s proof of stake protocol, and returns depositors a liquid token called staked ether (stETH) that can then be used again as collateral in other DeFi protocols such as Ethena. This structure creates a “synthetic” dollar position without requiring actual dollar reserves.

Perpetual futures are the backbone of synthetic stablecoins. They are contracts without an expiry date, designed to track the spot price of an asset through a recurring funding rate (that is, a basis payment between long and short positions that keeps prices aligned). When the perpetual future trades above spot, investors with long futures positions pay those with short futures positions; when it trades below spot, shorts pay longs. These funding flows create a bridge between leveraged traders and arbitrageurs, ensuring that derivatives stay close to their underlying assets. The mechanics of this trade are similar to those of the cash-futures basis trade in the Treasury relative value space.

Synthetic stablecoins rely on this structure to maintain their peg. Each minted coin represents a matched position: long staked ether (ETH) and short perpetual futures. The Ethena DeFi protocol earns the sum of staking rewards and any funding rate income from the short position. When funding rates remain positive and stable, this design delivers attractive returns with minimal price exposure, drawing new capital into the system. The key fragility, however, is that the hedge depends on continuous liquidity in derivatives markets and a consistently positive funding rate. If funding turns negative or margin costs rise, the synthetic dollar becomes expensive to maintain and redemptions begin.

Ethena’s Minting and Unwinding Mechanism

The stablecoin USDe, which is issued by Ethena, illustrates this mechanism in practice. New coins are minted when investors deposit ether or staked ether as collateral. Ethena’s programmatic smart contracts open a short position in ether perpetual futures, neutralizing price risk and locking in a yield given by the sum of the ether staking yield and the futures position’s funding rate. As long as that sum remains positive, issuance grows rapidly. Between early 2024 and mid‑2025, Ethena’s total supply expanded to nearly $15 billion, reflecting strong inflows of collateral and speculative demand for the high yields. By August 2025, Ethena had become the third-largest stablecoin by market capitalization (albeit a distant third after Tether’s USDT and Circle’s USDC).

When market conditions change, this process reverses. Falling funding rates in ether perpetual futures markets reduce income from short positions, while higher margin costs compress the yield advantage, making the positions unattractive. Even worse, funding rates could turn negative, with short futures holders having to pay long futures holders. Investors redeem USDe for the underlying ether, forcing Ethena’s smart contract to close its short futures position and release collateral. This closing sequence requires buying back futures and selling ether, putting pressure on both derivatives and spot markets. The result is a self-reinforcing unwind: lower prices reduce collateral values, which in turn trigger more redemptions.

A Simple Example

Consider an investor who wants to purchase $100,000 worth of synthetic stablecoins. They deposit $100,000 worth of staked ether as collateral, which earns a 3.5 percent annual staking yield. The protocol simultaneously opens a $100,000 short position in ether perpetual futures. If the funding rate is positive—say, 10 percent annualized—shorts receive payments from longs, generating additional yield. The investor’s total return would be approximately 13.5 percent (3.5 percent staking + 10 percent funding), while maintaining dollar-denominated exposure since the long ether and short futures positions offset each other.

But if the funding rate turns negative to –5 percent annualized, the dynamics reverse. The investor must pay 5 percent annually to maintain the short position while earning just 3.5 percent from staking—a net loss of 1.5 percent. This leads investors to close positions by buying back futures—and selling spot ether. As investors redeem en masse, these forced transactions amplify the original decline in rates.

Deleveraging and the October 10 Event

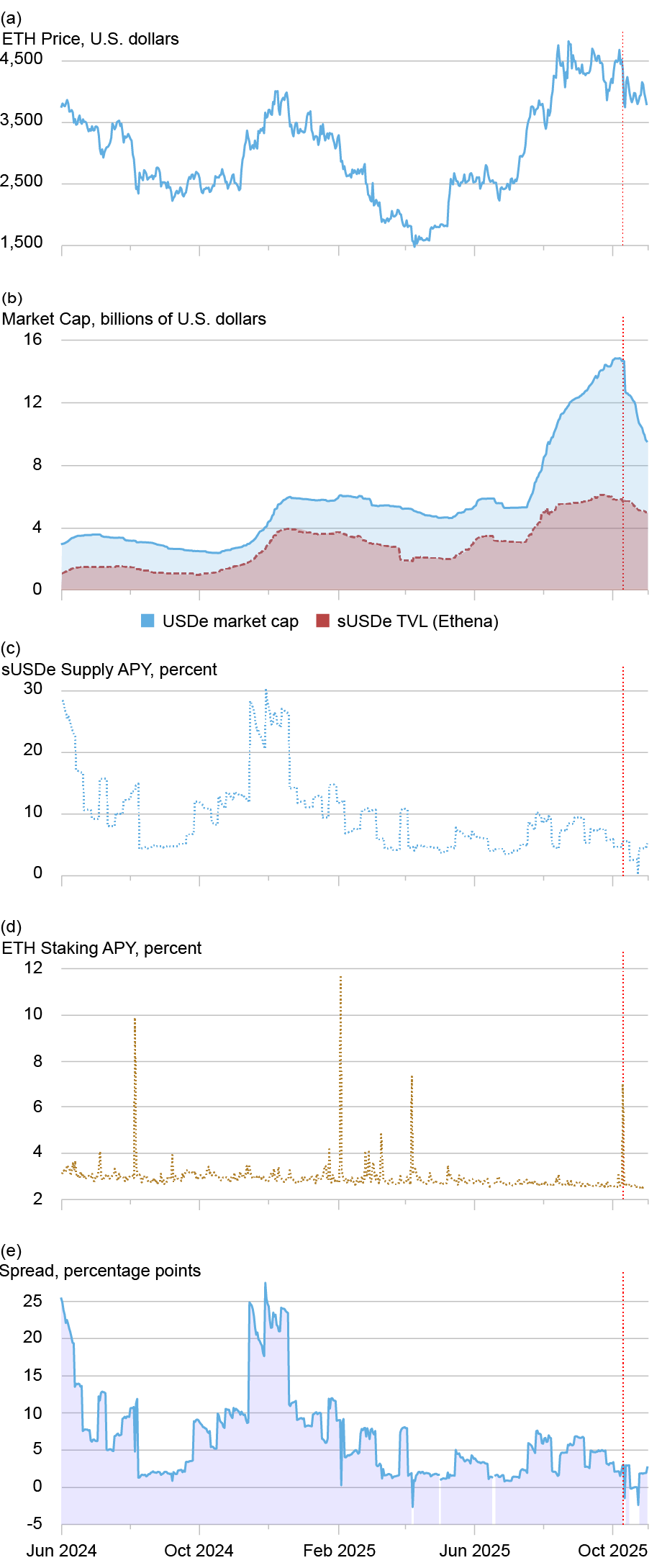

The dynamics of this deleveraging are visible in the chart below, which tracks the volume, yields, and spreads of USDe and its yield-paying analogue, staked USDe (sUSDe), between June 2024 and October 2025. The upper panels show the sharp expansion of USDe supply through the passage of the GENIUS Act in mid-2025, followed by a sudden contraction beginning in October. The lower panels plot the USDe yield and the ether staking yield. On October 10, the spread between them turned negative, meaning the cost of maintaining the short futures exceeded the return from staking. Once the yield turned negative, the incentive to hold USDe vanished, and investors began to unwind their positions.

USDe and Staked USDe Dynamics: Scale, Yields, and Spreads (June 2024 – October 2025)

Notes: Panel (a) shows the ether price; panel (b) the total market capitalization of Ethena (USDe) and the total staked value of Staked Ethena (sUSDe); panel (c) the sUSDe annual percentage yield (APY); panel (d) the ether staking yield; and panel (e) the yield spread between sUSDe and ETH staking. The vertical red line marks October 10, 2025, the date of the U.S. announcement of potential additional tariffs on Chinese goods.

The decline in market capitalization in panel b reflects this unwinding: collateral was released, futures short positions were closed, and liquidity drained from both markets. The system that had grown on the promise of a high carry became a forced seller, deepening the downturn. The episode underscores how delta-hedged stablecoins transmit funding shocks into the spot market for native cryptocurrencies such as ether. When the yield spread flips sign, redemptions accelerate, and leverage across the crypto ecosystem contracts as traders close leveraged ether positions and reduce exposure to derivatives. This closing of positions leads to lower ether prices and more closing of leveraged positions, an on-chain version of a margin spiral.

As a result of this unwinding, USDe’s market capitalization contracted by more than 13 percent following a sharp funding-rate reversal, as the spread between its yield and ether staking turned negative and investors raced for the exits. As redemptions flowed, the protocol closed its perpetual-futures shorts and released ether collateral, generating buy pressure in futures markets and sell pressure in spot markets almost simultaneously. The mechanics mirror traditional deleveraging spirals: leveraged positions unwind, forced sales hit the spot market, liquidity evaporates, and the original collateral asset value spirals downward.

The timing of these flows mattered. As liquidity thinned and funding rates worsened, the ability for arbitrageurs to convert USDe back into ETH or dollar equivalents slowed markedly. On the centralized exchange Binance, where USDe trading was thinner, prices briefly fell to US $0.65 despite on-chain peg integrity elsewhere. According to CoinDesk, this was because Binance’s price oracle referenced its own price feed, creating a procyclical effect that kept the price de-pegged for a few hours.

The combination of funding losses, collateral outflows, and liquidity strain pushed ether into a deeper decline. The result was a reinforcing loop: lower ether prices reduced the value of the posted collateral, triggering additional redemptions or liquidations, which in turn further depressed prices and funding rates. In short, the synthetic-dollar unwind became a transmission channel from the stablecoin system into crypto-asset prices.

Final Words

The deleveraging of USDe did not occur in isolation: it took place amid a broader funding squeeze and falling asset prices in native cryptocurrencies and other risky asset markets. But the magnitude of USDe’s declines and its design suggest it played a material role in amplifying the decline in ether prices.

Of note, the market-leading, asset-backed stablecoins of Tether’s USDT and Circle’s USDC did not de-anchor from their fiat dollar targets during the October 10 Ethena deleveraging episode. Circle’s USDC lost $280 million in market cap that day and Tether’s USDT gained a nearly equivalent $282 million, while both maintained their dollar targets.

These types of crises are increasingly relevant to policymakers, since stablecoins, tokenized money-market funds, stocks, and exchange-traded funds are creating growing links between traditional and blockchain-based financial markets. The total market capitalization of U.S. Bitcoin, Ether, and Solana ETFs is now around $95 billion. Tokenized Treasury funds bring short-term government debt directly onto public blockchains, allowing investors to move easily between DeFi and dollar assets. Major intermediaries continue to expand into this space. As the connections between crypto and the traditional financial system deepen, crises such as the one involving synthetic stablecoins have the potential to transmit volatility to traditional financial markets.

Pablo Azar is a financial research economist in the Federal Reserve Bank of New York’s Research and Statistics Group.

Jeff Garofano is a capital markets trading associate in the Federal Reserve Bank of New York’s Markets Group.

How to cite this post:

Pablo D. Azar and Jeff Garofano, “Synthetic Stablecoins and Financial Stability,” Federal Reserve Bank of New York Liberty Street Economics, June 23, 2026, https://doi.org/10.59576/lse.20260623

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics