178 posts on "Banks"

December 20, 2024

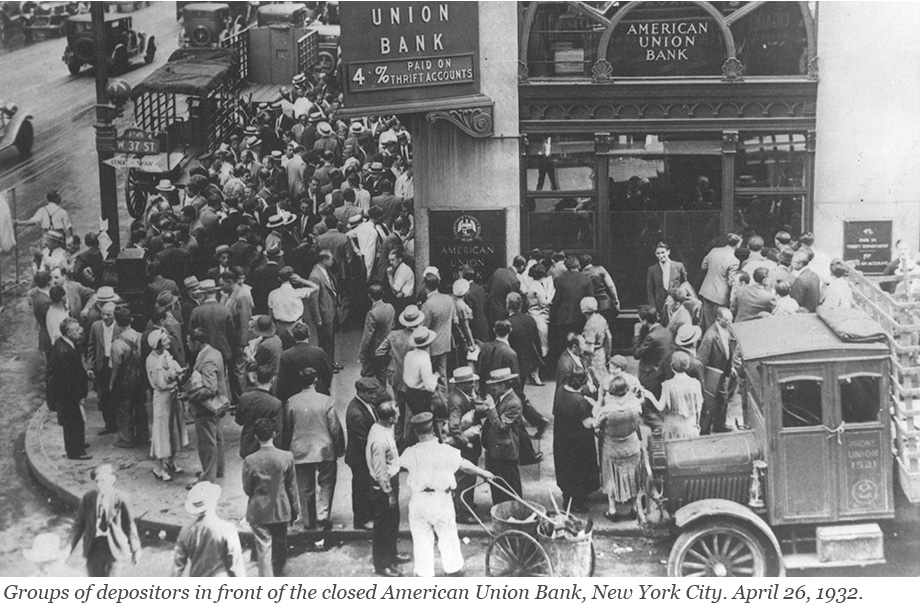

Anatomy of the Bank Runs in March 2023

Runs have plagued the banking system for centuries and returned to prominence with the bank failures in early 2023. In a traditional run—such as depicted in classic photos from the Great Depression—depositors line up in front of a bank to withdraw their cash. This is not how modern bank runs occur: today, depositors move money from a risky to a safe bank through electronic payment systems. In a recently published staff report, we use data on wholesale and retail payments to understand the bank run of March 2023. Which banks were run on? How were they different from other banks? And how did they respond to the run?

Posted at 6:30 am in Banks, Crisis, Financial Institutions, Lender of Last Resort, Panic | Permalink | Comments (1)

December 3, 2024

Documenting Lender Specialization

Robust banks are a cornerstone of a healthy financial system. To ensure their stability, it is desirable for banks to hold a diverse portfolio of loans originating from various borrowers and sectors so that idiosyncratic shocks to any one borrower or fluctuations in a particular sector would be unlikely to cause the entire bank to go under. With this long-held wisdom in mind, how diversified are banks in reality?

November 25, 2024

Why Do Banks Fail? Bank Runs Versus Solvency

Evidence from a 160-year-long panel of U.S. banks suggests that the ultimate cause of bank failures and banking crises is almost always a deterioration of bank fundamentals that leads to insolvency. As described in our previous post, bank failures—including those that involve bank runs—are typically preceded by a slow deterioration of bank fundamentals and are hence remarkably predictable. In this final post of our three-part series, we relate the findings discussed previously to theories of bank failures, and we discuss the policy implications of our findings.

November 22, 2024

Why Do Banks Fail? The Predictability of Bank Failures

Can bank failures be predicted before they happen? In a previous post, we established three facts about failing banks that indicated that failing banks experience deteriorating fundamentals many years ahead of their failure and across a broad range of institutional settings. In this post, we document that bank failures are remarkably predictable based on simple accounting metrics from publicly available financial statements that measure a bank’s insolvency risk and funding vulnerabilities.

November 21, 2024

Why Do Banks Fail? Three Facts About Failing Banks

Why do banks fail? In a new working paper, we study more than 5,000 bank failures in the U.S. from 1865 to the present to understand whether failures are primarily caused by bank runs or by deteriorating solvency. In this first of three posts, we document that failing banks are characterized by rising asset losses, deteriorating solvency, and an increasing reliance on expensive noncore funding. Further, we find that problems in failing banks are often the consequence of rapid asset growth in the preceding decade.

November 12, 2024

Banking System Vulnerability: 2024 Update

After a period of relative stability, a series of bank failures in 2023 renewed questions about the fragility of the banking system. As in previous years, we provide in this post an update of four analytical models aimed at capturing different aspects of the vulnerability of the U.S. banking system using data through 2024:Q2 and discuss how these measures have changed since last year.

Posted at 7:00 am in Bank Capital, Banks, Financial Institutions, Liquidity | Permalink | Comments (4)

September 25, 2024

Flood Risk Outside Flood Zones — A Look at Mortgage Lending in Risky Areas

In support of the National Flood Insurance Program (NFIP), the Federal Emergency Management Agency (FEMA) creates flood maps that indicate areas with high flood risk, where mortgage applicants must buy flood insurance. The effects of flood insurance mandates were discussed in detail in a prior blog series. In 2021 alone, more than $200 billion worth of mortgages were originated in areas covered by a flood map. However, these maps are discrete, whereas the underlying flood risk may be continuous, and they are sometimes outdated. As a result, official flood maps may not fully capture the true flood risk an area faces. In this post, we make use of unique property-level mortgage data and find that in 2021, mortgages worth over $600 billion were originated in areas with high flood risk but no flood map. We examine what types of lenders are aware of this “unmapped” flood risk and how they adjust their lending practices. We find that—on average—lenders are more reluctant to lend in these unmapped yet risky regions. Those that do, such as nonbanks, are more aggressive at securitizing and selling off risky loans.

August 12, 2024

Reallocating Liquidity to Resolve a Crisis

Shortly after the collapse of Silicon Valley Bank (SVB) in March 2023, a consortium of eleven large U.S. financial institutions deposited $30 billion into First Republic Bank to bolster its liquidity and assuage panic among uninsured depositors. In the end, however, First Republic Bank did not survive, raising the question of whether a reallocation of liquidity among financial institutions can ever reduce the need for central bank balance sheet expansion in the fight against bank runs. We explore this question in this post, based on a recent working paper.

June 20, 2024

The Growing Risk of Spillovers and Spillbacks in the Bank‑NBFI Nexus

Nonbank financial institutions (NBFIs) are growing, but banks support that growth via funding and liquidity insurance. The transformation of activities and risks from banks to a bank-NBFI nexus may have benefits in normal states of the world, as it may result in overall growth in (especially, credit) markets and widen access to a wide range of financial services, but the system may be disproportionately exposed to financial and economic instability when aggregate tail risk materializes. In this post, we consider the systemic implications of the observed build-up of bank-NBFI connections associated with the growth of NBFIs.

June 18, 2024

Banks and Nonbanks Are Not Separate, but Interwoven

In our previous post, we documented the significant growth of nonbank financial institutions (NBFIs) over the past decade, but also argued for and showed evidence of NBFIs’ dependence on banks for funding and liquidity support. In this post, we explain that the observed growth of NBFIs reflects banks optimally changing their business models in response to factors such as regulation, rather than banks stepping away from lending and risky activities and being substituted by NBFIs. The enduring bank-NBFI nexus is best understood as an ever-evolving transformation of risks that were hitherto with banks but are now being repackaged between banks and NBFIs.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics