55 posts on "Equitable Growth"

May 12, 2021

Credit Card Balance Declines Are Largest Among Older, Wealthier Borrowers

Total household debt rose by $85 billion in the first quarter of 2021, according to the latest Quarterly Report on Household Debt and Credit from the New York Fed’s Center for Microeconomic Data. Since the start of the pandemic, household debt balances have increased in every quarter but one—the second quarter of 2020, when lockdowns were in full effect. The Quarterly Report and this analysis are based on the New York Fed’s Consumer Credit Panel, which is based on Equifax credit data.

February 9, 2021

Black and White Differences in the Labor Market Recovery from COVID‑19

The ongoing COVID-19 pandemic and the various measures put in place to contain it caused a rapid deterioration in labor market conditions for many workers and plunged the nation into recession. The unemployment rate increased dramatically during the COVID recession, rising from 3.5 percent in February to 14.8 percent in April, accompanied by an almost three percentage point decline in labor force participation. While the subsequent labor market recovery in the aggregate has exceeded even some of the most optimistic scenarios put forth soon after this dramatic rise, this recovery has been markedly weaker for the Black population. In this post, we document several striking differences in labor market outcomes by race and use Current Population Survey (CPS) data to better understand them.

Posted at 11:00 am in Demographics, Equitable Growth, Human Capital, Inequality, Labor Market, Pandemic, Recession, Unemployment | Permalink

Understanding the Racial and Income Gap in Commuting for Work Following COVID‑19

The introduction of numerous social distancing policies across the United States, combined with voluntary pullbacks in activity as responses to the COVID-19 outbreak, resulted in differences emerging in the types of work that were done from home and those that were not. Workers at businesses more likely to require in-person work—for example, some, but not all, workers in healthcare, retail, agriculture and construction—continued to come in on a regular basis. In contrast, workers in many other businesses, such as IT and finance, were generally better able to switch to working from home rather than commuting daily to work. In this post, we aim to understand whether following the onset of the pandemic there was a wedge in the incidence of commuting for work across income and race. And how did this difference, if any, change as the economy slowly recovered? We take advantage of a unique data source, SafeGraph cell phone data, to identify workers who continued to commute to work in low income versus higher income and majority-minority (MM) versus other counties.

Posted at 11:00 am in Demographics, Equitable Growth, Human Capital, Inequality, Labor Market, Pandemic, Unemployment | Permalink

Some Workers Have Been Hit Much Harder than Others by the Pandemic

Abel and Deitz look at the outsized impact of the COVID-19 pandemic on some workers, particularly those who are in lower-wage jobs, without a college degree, female, minority, and younger.

Posted at 11:00 am in Demographics, Employment, Equitable Growth, Inequality, Labor Market, Pandemic, Unemployment | Permalink | Comments (1)

August 18, 2020

Debt Relief and the CARES Act: Which Borrowers Benefit the Most?

COVID-19 and associated social distancing measures have had major labor market ramifications, with massive job losses and furloughs. Millions of people have filed jobless claims since mid-March—6.9 million in the week of March 28 alone. These developments will surely lead to financial hardship for millions of Americans, especially those who hold outstanding debts while facing diminishing or disappearing wages. The CARES Act, passed by Congress on April 2, 2020, provided $2.2 trillion in disaster relief to combat the economic impacts of COVID-19. Among other measures, it included mortgage and student debt relief measures to alleviate the cash flow problems of borrowers. In this post, we examine who could benefit most (and by how much) from various debt relief provisions under the CARES Act.

Posted at 7:00 am in Equitable Growth, Household Finance, Housing, Inequality | Permalink | Comments (2)

July 8, 2020

Measuring Racial Disparities in Higher Education and Student Debt Outcomes

Across the United States, the cost of all types of higher education has been rising faster than overall inflation for more than two decades. Despite rising costs, aggregate undergraduate enrollment rose steadily between 2000 and 2010 before leveling off and dipping slightly to its current level. Rising college costs have steadily increased dependence on student debt for college financing, with many students and parents turning to federal and private loans to pay for higher education. An earlier post in this series reported that borrowers in majority Black areas have higher student loan balances and rates of default than those in both majority white and majority Hispanic areas. In this post, we study how differences in college attendance rates and in the types of colleges attended generate heterogeneity in loan experiences. Specifically, using nationwide data, we analyze heterogeneities in college-going and heterogeneities in student debt and default experiences by college type across individuals living in majority Black, majority Hispanic, and majority white zip codes.

Posted at 7:30 am in Education, Equitable Growth, Household Finance, Inequality, Student Loans | Permalink

Inequality in U.S. Homeownership Rates by Race and Ethnicity

Homeownership has historically been an important means for Americans to accumulate wealth—in fact, at more than $15 trillion, housing equity accounts for 16 percent of total U.S. household wealth. Consequently, the U.S. homeownership cycle has triggered large swings in Americans’ net worth over the past twenty-five years. However, the nature of those swings has varied significantly by race and ethnicity, with different demographic groups tracing distinct trajectories through the housing boom, the foreclosure crisis, and the subsequent recovery. Here, we look into the dynamics underlying these divergences and explore some potential explanations.

December 17, 2019

Growth Has Slowed across the Region

At today’s regional economic press briefing, we highlighted some recent softening in the tri-state regional economy (New York, Northern New Jersey, and Fairfield County, Connecticut)—a noteworthy contrast from our briefing a year ago, when economic growth and job creation were fairly brisk. We also showed that Puerto Rico and the U.S. Virgin Islands, which are part of the New York Fed’s district, both continue to face major challenges but have made significant economic progress following the catastrophic hurricanes of 2017.

October 9, 2019

Who Borrows for College—and Who Repays?

Student loans are increasingly a focus of discourse among politicians, policymakers, and the news media, resulting in a range of new ideas to address the swelling aggregate debt. Evaluating student loan policy proposals requires understanding the challenges faced by student borrowers. In this post, we explore the substantial variation in the experiences of borrowers and consider the distributional effects of various policy options.

October 7, 2019

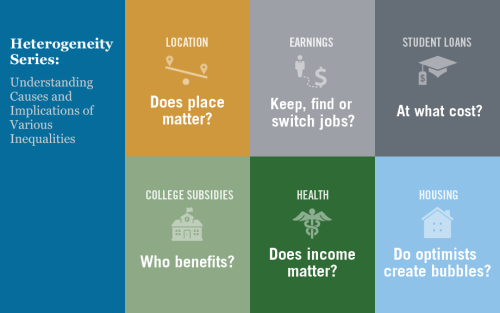

Introduction to Heterogeneity Series: Understanding Causes and Implications of Various Inequalities

Economic analysis is often geared toward understanding the average effects of a given policy or program. Likewise, economic policies frequently target the average person or firm. While averages are undoubtedly useful reference points for researchers and policymakers, they don’t tell the whole story: it is vital to understand how the effects of economic trends and government policies vary across geographic, demographic, and socioeconomic boundaries. It is also important to assess the underlying causes of the various inequalities we observe around us, be they related to income, health, or any other set of indicators. Starting today, we are running a series of six blog posts (apart from this introductory post), each of which focuses on an interesting case of heterogeneity in the United States today.

Posted at 7:00 am in Education, Equitable Growth, Household Finance, Inequality, Labor Market, Regional Analysis | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics