7 posts on "Discount Window"

January 17, 2025

Discount Window Stigma After the Global Financial Crisis

The rapidity of deposit outflows during the March 2023 banking run highlights the important role that the Federal Reserve’s discount window should play in strengthening financial stability. A lack of borrowing, however, has plagued the discount window for decades, likely due to banks’ concerns about stigma—that is, their unwillingness to borrow at the discount window because it may be viewed as a sign of financial weakness in the eyes of regulators and market participants. The discount window has been reformed several times to alleviate this problem. Although the presence of stigma during the great financial crisis has been documented empirically, we do not know whether stigma has remained since then. In this post, based on a recent Staff Report, we fill this gap by using transaction-level data from the federal funds market to examine whether the discount window remains stigmatized today.

Posted at 7:00 am in Central Bank | Permalink

December 20, 2024

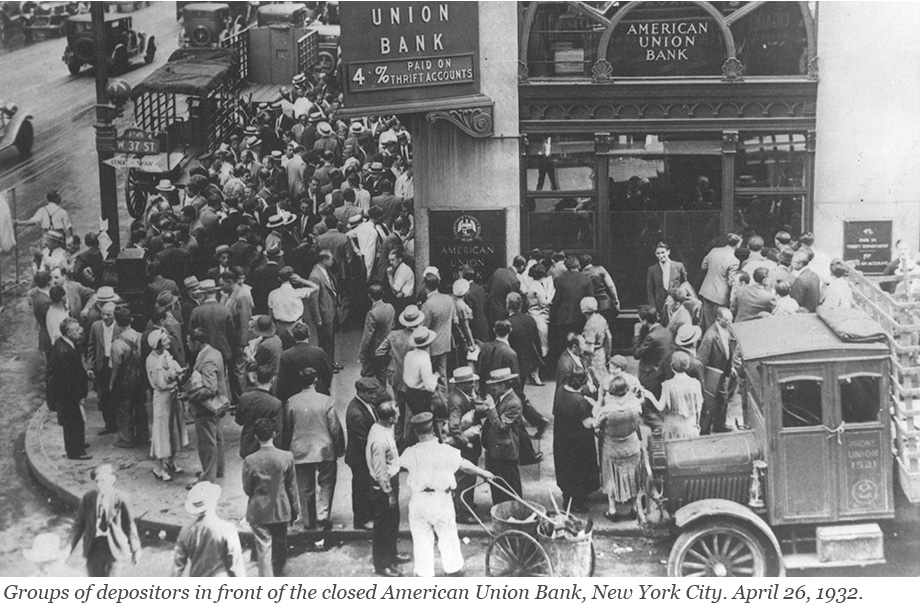

Anatomy of the Bank Runs in March 2023

Runs have plagued the banking system for centuries and returned to prominence with the bank failures in early 2023. In a traditional run—such as depicted in classic photos from the Great Depression—depositors line up in front of a bank to withdraw their cash. This is not how modern bank runs occur: today, depositors move money from a risky to a safe bank through electronic payment systems. In a recently published staff report, we use data on wholesale and retail payments to understand the bank run of March 2023. Which banks were run on? How were they different from other banks? And how did they respond to the run?

Posted at 6:30 am in Banks, Crisis, Financial Institutions, Lender of Last Resort, Panic | Permalink | Comments (1)

May 31, 2024

Can Discount Window Stigma Be Cured?

One of the core responsibilities of central banks is to act as “lender of last resort” to the financial system. In the U.S., the Federal Reserve has been operating as a lender of last resort through its “discount window” (DW) for more than a century. Historically, however, the DW has been plagued by stigma—banks’ reluctance to use the DW, even for benign reasons, out of concerns that it could be interpreted as a sign of financial weakness. In this post, we report on new research showing that once a DW facility is stigmatized, removing that stigma is difficult.

January 17, 2023

The Recent Rise in Discount Window Borrowing

The Federal Reserve’s primary credit program—offered through its “discount window” (DW)—provides temporary short-term funding to fundamentally sound banks. Historically, loan activity has been low during normal times due to a variety of factors, including the DW’s status as a back-up source of liquidity with a relatively punitive interest rate, the stigma attached to DW borrowing from the central bank, and, since 2008, elevated levels of reserves in the banking system. However, beginning in 2022, DW borrowing under the primary credit program increased notably in comparison to past years. In this post, we examine the factors that may have contributed to this recent trend.

January 13, 2014

Discount Window Stigma

One of the main missions of central banks is to act as a lender of last resort to the banking system.

Posted at 7:00 am in Financial Institutions | Permalink

August 31, 2011

Is There Stigma to Discount Window Borrowing?

The Federal Reserve employs the discount window (DW) to provide funding to fundamentally solvent but illiquid banks (see the March 30 post “Why Do Central Banks Have Discount Windows?”). Historically, however, there has been a low level of DW use by banks, even when they are faced with severe liquidity shortages, raising the possibility of a stigma attached to DW borrowing. If DW stigma exists, it is likely to inhibit the Fed’s ability to act as lender of last resort and prod banks to turn to more expensive sources of financing when they can least afford it. In this post, we provide evidence that during the recent financial crisis banks were willing to pay higher interest rates in order to avoid going to the DW, a pattern of behavior consistent with stigma.

March 30, 2011

Why Do Central Banks Have Discount Windows?

Though not literally a window any longer, the “discount window” refers to the facilities that central banks, acting as lender of last resort, use to provide liquidity to commercial banks. While the need for a discount window and lender of last resort has been debated, the basic rationale for their existence is that circumstances can arise, such as bank runs and panics, when even fundamentally sound banks cannot raise liquidity on short notice. Massive discount window borrowing in the immediate aftermath of the September 11 terrorist attack on the United States clearly illustrates the importance of a discount window even in a modern economy. In this post, we discuss the classical rationale for the discount window, some debate surrounding it, and the challenges that the “stigma” associated with borrowing at the discount window poses for the effectiveness of the discount window.

Posted at 10:03 am in Banks, Central Bank, Financial Institutions, Lender of Last Resort | Permalink

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics