In the aftermath of the COVID-19 pandemic, inflation rose almost simultaneously in most economies around the world. After peaking in mid-2022, inflation then went into decline—a fall that was just as universal as the initial rise. In this post, we explore the interrelation of inflation dynamics across OECD countries by constructing a measure of the persistence of global inflation. We then study the extent to which the persistence of global inflation reflects broad-based swings, as opposed to idiosyncratic country-level movements. Our main finding is that the spike and subsequent moderation in global inflation in the post-pandemic period were driven by persistent movements. When we look at measures of inflation that include food and energy prices, most of the persistence appears to be broad-based, suggesting that international oil and commodity prices played an important role in global inflation dynamics. Excluding food and energy prices in the analysis still shows a broad-based persistence, although with a substantial increase in the role of country-specific factors.

A Measure of Global Inflation Persistence

Our objective is to estimate the persistence and dynamics of inflation across countries in the post-pandemic global economy. We begin by describing the data and methods we use.

Our analysis is based on monthly inflation data covering 1980-2023 for sixteen OECD countries: Austria, Belgium, Canada, Denmark, France, Germany, Ireland, Italy, Japan, the Netherlands, Norway, Spain, Sweden, Switzerland, the United Kingdom, and the United States. From the OECD Main Economic Indicators database, we obtain time series for each country’s consumer price index (CPI), data that are consistent over time and comparable across countries. We compute monthly annualized inflation rates for each country based on total CPI and on the CPI excluding the food and energy categories. We refer to these as headline and core CPI inflation, respectively, noting that different countries may define the “core” aggregate in slightly different ways. We apply a homogeneous definition across countries because our goal is to characterize the evolution of inflation using internationally comparable measures.

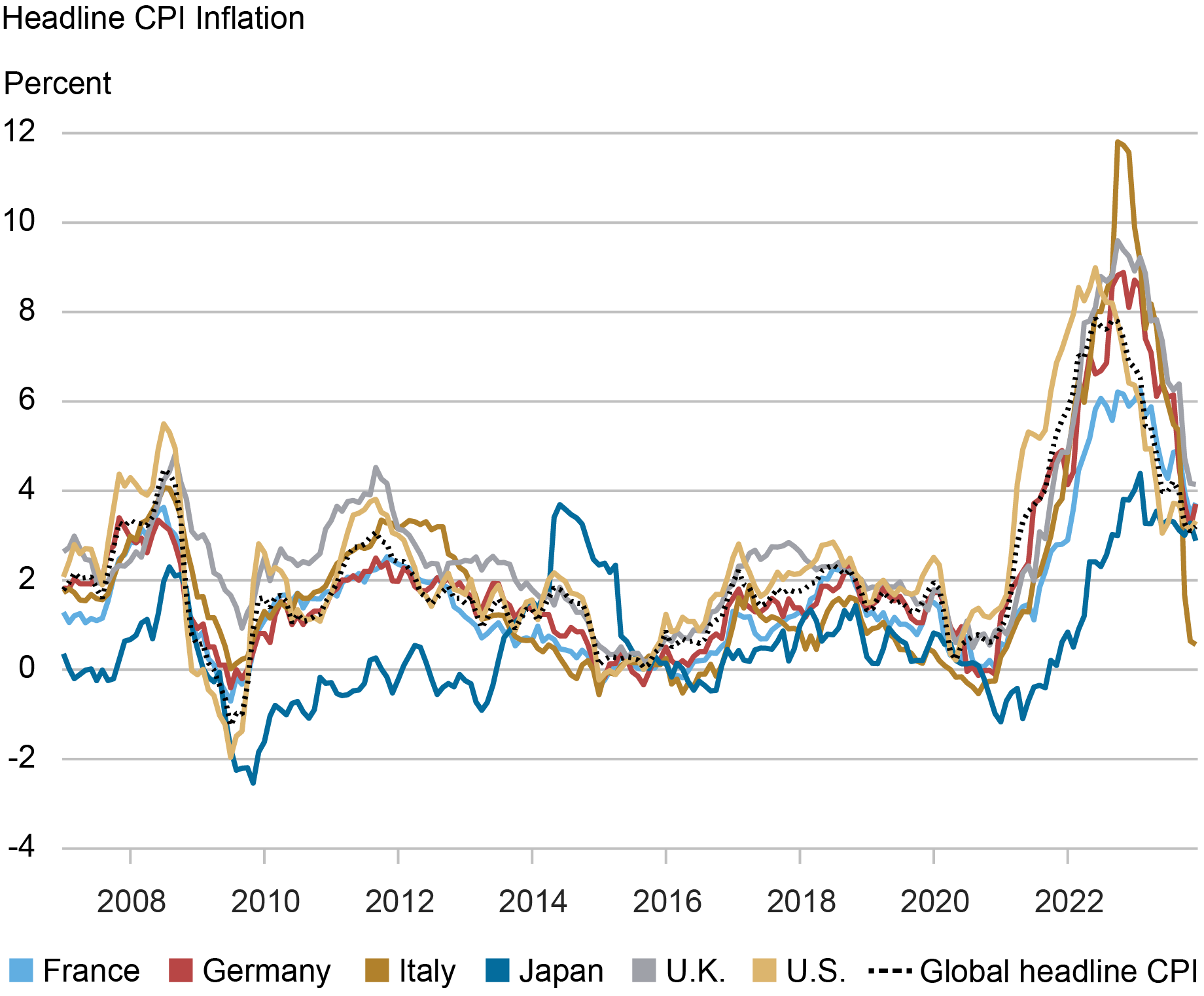

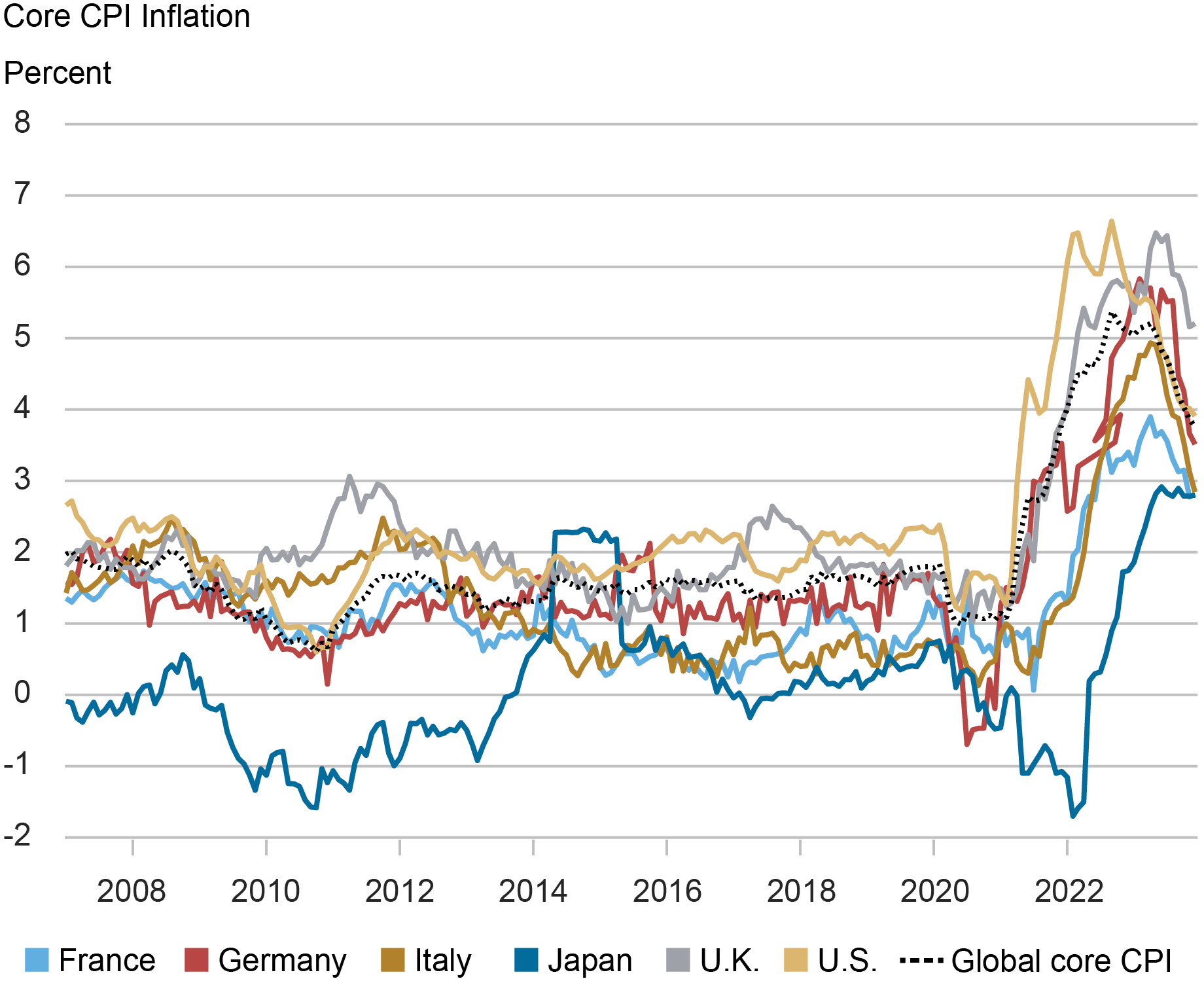

To construct a global inflation measure, we follow the OECD practice of aggregating national inflation rates using weights based on their share of private final consumption expenditures across households and non-profit institutions in purchasing power parity terms. We call this measure ”global,” even though it refers only to a subset of OECD economies. The following two charts display the recent evolution of the twelve-month rate of headline and core CPI inflation for the global measure and for a subset of countries. It is clear in the figures that, although the level of inflation may differ across countries (for example, it tends to be lower in Japan than in the U.K.), cyclical movements are often synchronized.

Headline CPI Inflation Co-Moves Strongly across OECD Economies

Source: OECD Main Economic Indicators database.

Core CPI Inflation Co-Moves Strongly across OECD Economies

Source: OECD Main Economic Indicators database.

The natural question is how much of the cyclical movements in inflation experienced by different economies are persistent. To answer this question, we apply a methodology that has been used successfully to study the persistence of inflation across sectors of the same economy (see, for example, here for our own application to the US economy). To be more specific, our method models the monthly inflation rate of each country as the sum of a persistent and a transitory component. Both persistent and transitory components are further decomposed into common and country-specific subcomponents. We define global trend inflation to be the aggregate of the persistent components (both common and country-specific) of the different countries, each weighted by the share we discussed above. This framework has two advantages. On the one hand, it allows us to filter out transitory variations in inflation which often reflect measurement error and outliers. On the other, it allows us to determine whether movements in the global trend come from shocks that affect individual countries (e.g., domestic policy or demand changes) or all countries at the same time (e.g., changes in the international price of oil or other commodities, or the global spillover of policy changes in large economies).

How Much of Current Global Inflation Is Persistent?

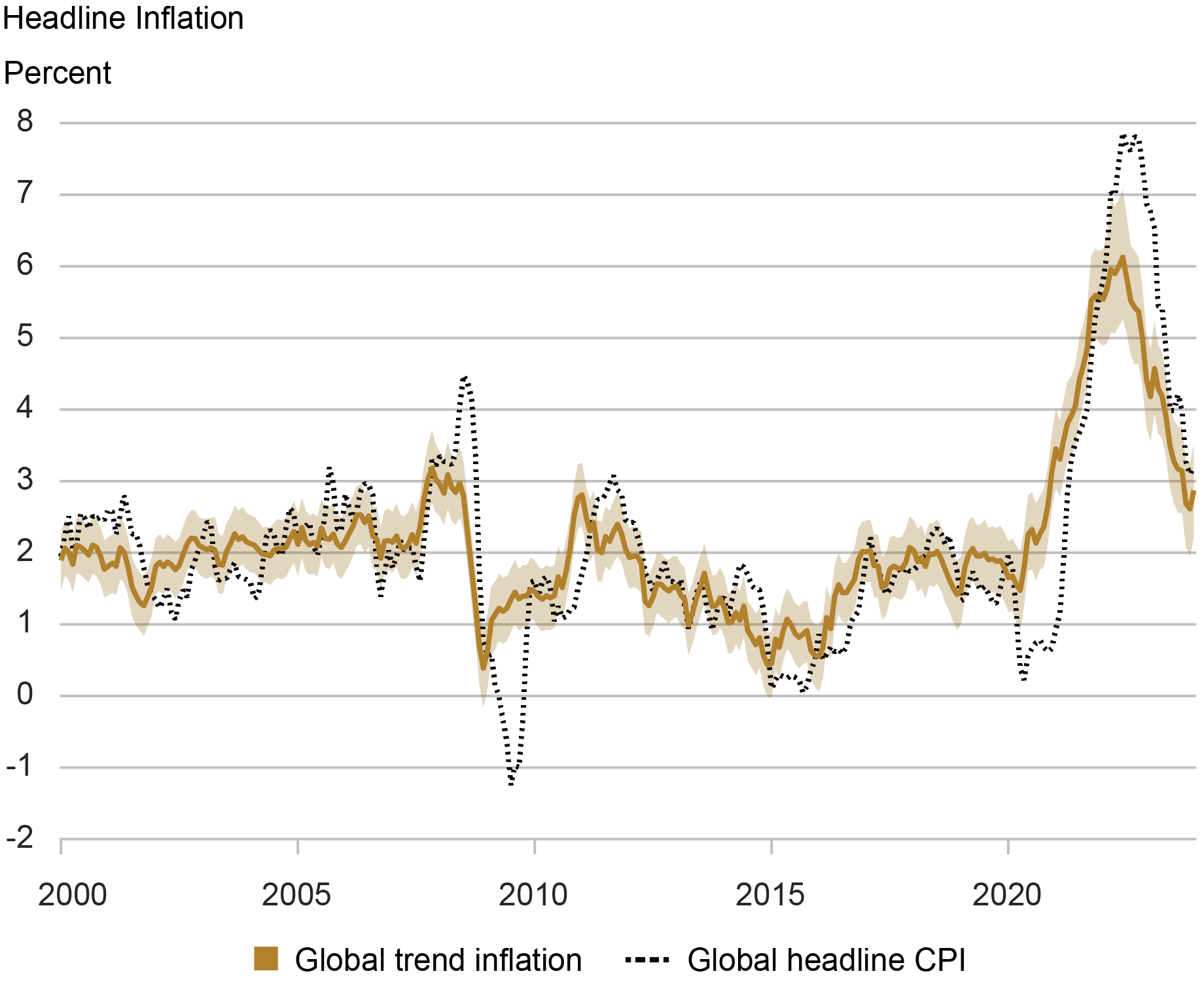

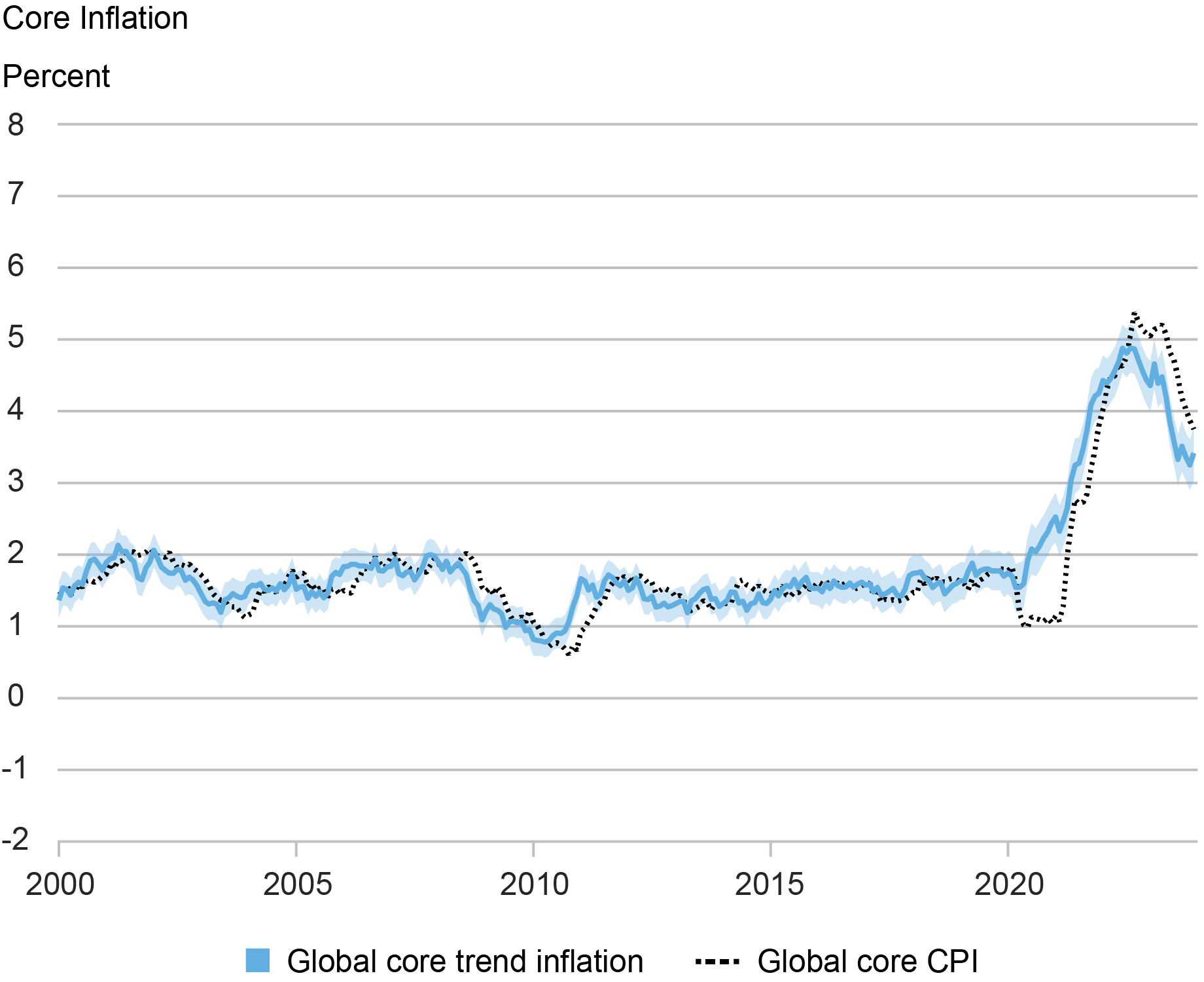

The following two charts present estimates for the global trends in headline and core CPI inflation (solid lines), together with their reported twelve-month inflation rates (dotted lines) for reference. Shaded areas represent 68 percent probability bands for the trend estimates. We highlight two features. First, the global trend measures do not display some of the extreme swings that we see in the twelve-month rates (see, for instance, the Great Recession and the COVID-19 pandemic periods in the chart for headline CPI). This is because our method removes part of the transitory shocks that drive those movements. As a result, the level of the peaks and troughs in the global trend is usually different from the twelve-month rate counterparts.

Global Trend Inflation in Headline and Core CPI Has Moderated since Mid-2022

Sources: OECD Main Economic Indicators database; authors’ estimates.

Sources: OECD Main Economic Indicators database; authors’ estimates.

The second feature to highlight is that the trend estimates often move ahead of the global inflation measures. This is explained by the fact that our model targets the trend in monthly rates, not in 12-month rates, which results in a less backward-looking and timelier measure. Moreover, the recent evolution (by which the trend lies below the twelve-month rate) suggests that there is scope for further disinflation in the short term in both the headline and core CPI measures.

One difference between headline and core CPI is that the trend is generally closer to observed inflation for the latter. This is not surprising, considering the higher sensitivity of headline inflation to food and energy prices which tend to be volatile. Another difference is the relative importance of common versus country-specific components which we analyze next.

How Much of Current Inflation Persistence Is Broad-Based?

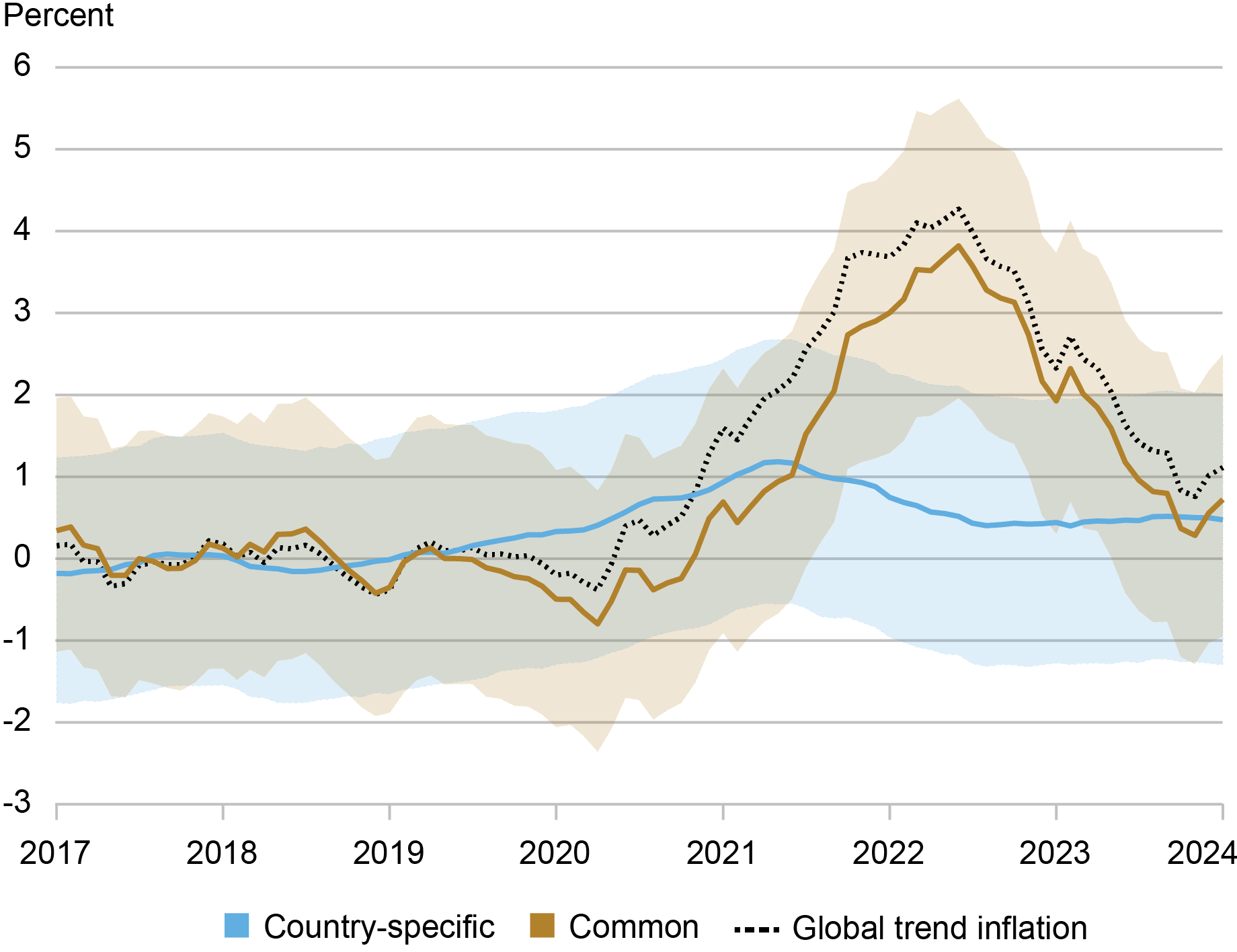

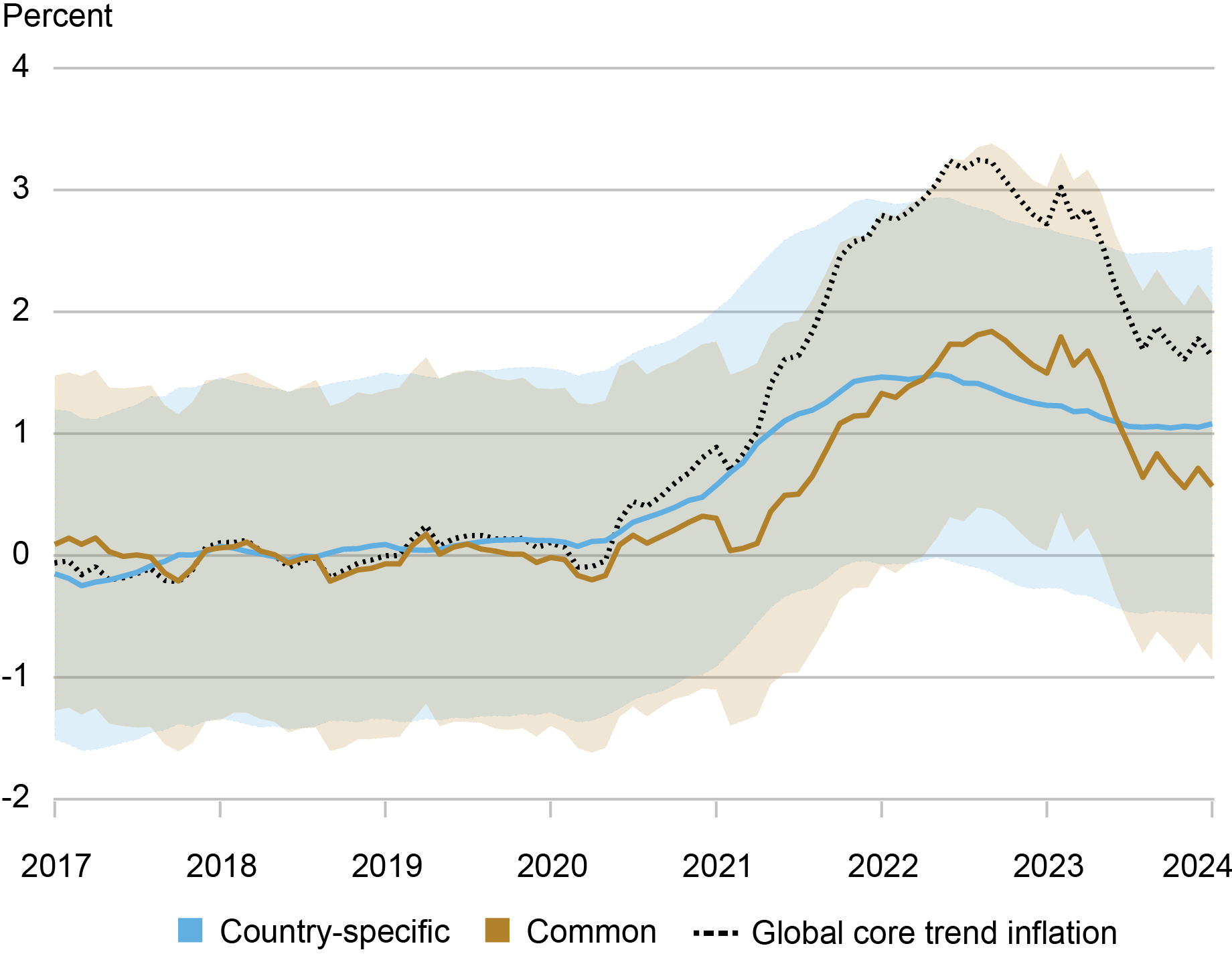

To quantify the importance of broad-based versus country-specific shocks in explaining the dynamics of the global trend we first normalize the total, common and country-specific trend components by subtracting their average level for the period January-2017 to December-2019. This is equivalent to measuring the cumulative change in the global trend since the pre-pandemic period. We next ask what fraction of the cumulative change in the global inflation trend is attributed to each component. The decomposition of the global trend between common and country-specific components for both headline and core CPI is shown in the next two charts.

Post-Pandemic Movements in Headline CPI Global Trend Were Mostly Broad-Based

Sources: OECD Main Economic Indicators database; authors’ estimates.

Note: All trends are normalized by subtracting their average level between Jan-2017 and Dec-2019; shaded areas around the country-specific and common areas represent 68 percent probability bands.

Country-Specific Factors Contributed Significantly to the Core CPI Global Trend

Sources: OECD Main Economic Indicators database; authors’ estimates.

Note: All trends are normalized by subtracting their average level between Jan-2017 and Dec-2019; shaded areas around the country-specific and common areas represent 68 percent probability bands.

For headline CPI, the change in the trend between the beginning of the COVID-19 pandemic and its peak in mid-2022 (roughly a 4-percentage point increase) is almost entirely accounted for by the common component (approximately 90% of the increase). The same can be said of the moderation that took place between mid-2022 and end of 2023.

Turning to core CPI, the picture is quite different. First, rather than a fast decline after mid-2022, the trend in global core CPI inflation experienced a plateau that extended until early 2023. Second, the increase in the trend between the beginning of the pandemic and this plateau amounted to slightly above 3 percentage points, less than its headline counterpart. Finally, the composition is very different, with country-specific and common persistence accounting each for about half of the cumulative change. Interestingly, the moderation observed since the peak has been driven mostly by the common component, which suggests that there remain domestic factors inducing persistence in inflation.

Conclusion

To summarize, the spike and subsequent moderation in global inflation that took place in the aftermath of the COVID-19 pandemic reflect a mix of international and domestic factors. When we estimate inflation persistence using measures that include food and energy prices, most of the change in global inflation persistence is broad-based. By contrast, when we use core measures, about half of the increase (but less than half of the decrease since the peak) originates in domestic, country-specific movements. This suggests that both large movements in the international price of oil and other commodities, as well as domestic policy and demand factors, played an important role in the recent inflationary episode.

Analyzing more disaggregated data by country and sector and quantifying the role of specific international and domestic factors (supply chains, monetary and fiscal policies, etc.) is an interesting avenue for future research.

Martín Almuzara is a research economist in Macroeconomic and Monetary Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Babur Kocaoglu is a research analyst in Macroeconomic and Monetary Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

Argia Sbordone is the head of Macroeconomic and Monetary Studies in the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Martín Almuzara, Babur Kocaoglu, and Argia Sbordone, “Is the Recent Inflationary Spike a Global Phenomenon? ,” Federal Reserve Bank of New York Liberty Street Economics, May 16, 2024, https://libertystreeteconomics.newyorkfed.org/2024/05/is-the-recent-inflationary-spike-a-global-phenomenon/

BibTeX: View |

Disclaimer

The views expressed in this post are those of the author(s) and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics