379 posts on "Liberty Street Economics"

July 17, 2026

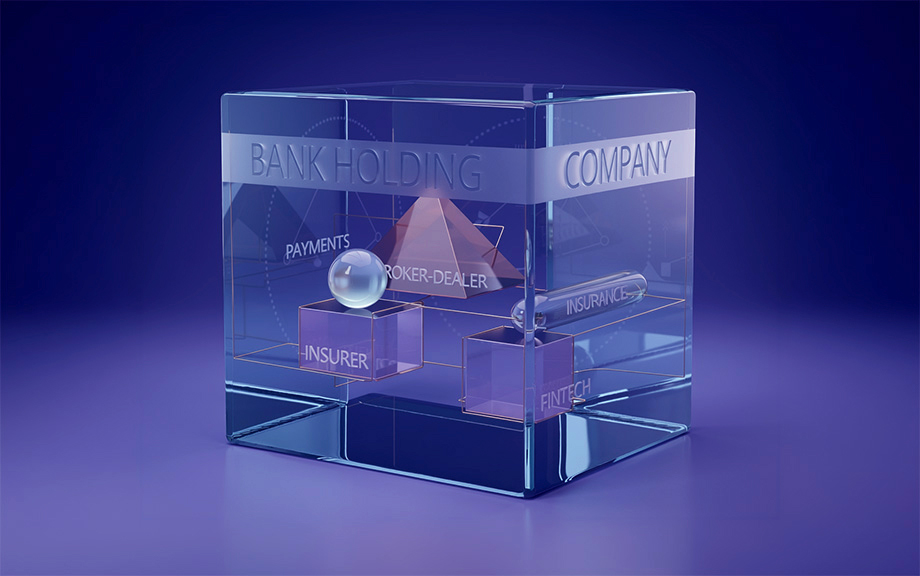

Nonbank Subsidiaries and the Hidden Fragility of Internal Capital Markets Reallocation

This post concludes a three-part series on how bank regulation interacts with the organizational structure of banking firms. The first post documented the equity-rich nonbank subsidiaries inside bank holding companies (BHCs); the second post showed that BHCs met Basel III by reallocating capital internally, moving equity from nonbank affiliates to bank subsidiaries rather than raising new external capital. Here we ask what that reallocation meant for financial stability. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 16, 2026

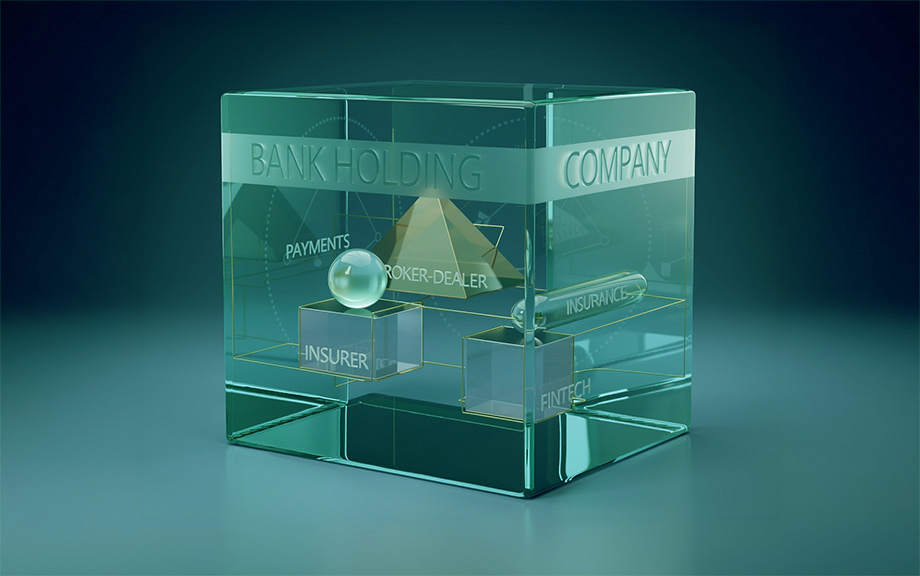

How Basel III Changes Where Capital Sits: Nonbank Subsidiaries as Equity Reservoirs

This post is the second in a three-part series on how bank regulation interacts with the organizational structure of banking firms. The first post documented that nonbank subsidiaries inside bank holding companies (BHCs) are large, equity-rich “reservoirs,” and that bank-level capital diverged sharply from consolidated capital after Basel III took effect in 2015. This post asks why, and traces the answer through the internal plumbing of the holding company. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 15, 2026

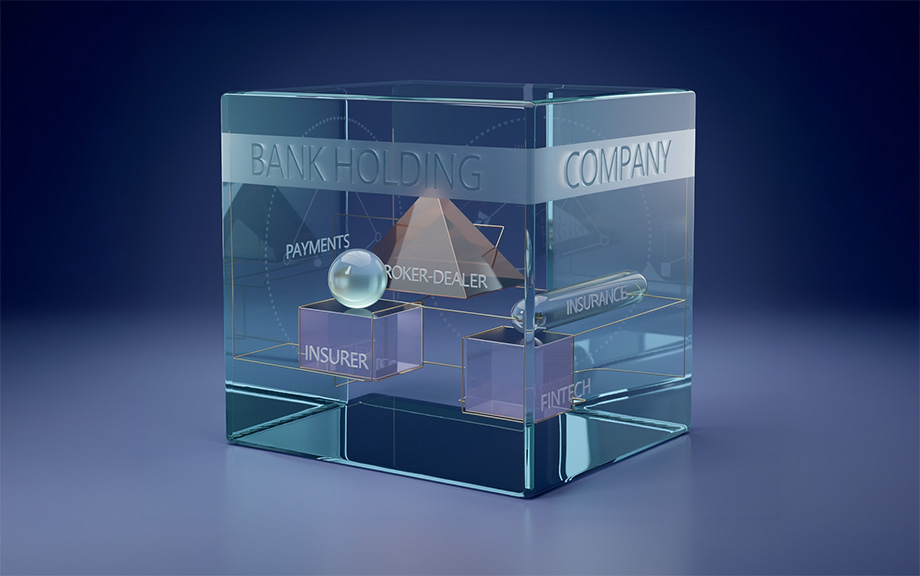

Capitalizing on Nonbanks: Regulatory Arbitrage Within Bank Holding Companies

This post is the first in a three-part series on how bank regulation interacts with the organizational structure of banking firms. The series draws on the authors’ recent Staff Report, “Regulatory Arbitrage Within the Firm.”

July 9, 2026

Effect of Tariffs on U.S. Small Businesses

How has the recent implementation of tariffs affected small businesses? Due to lack of data, little is known about this issue. In this Liberty Street Economics post, we use data from the 2025 edition of the Small Business Credit Survey (SBCS) to explore this question for businesses nationally and in the Second District (defined, for the purpose of this study, as New York, New Jersey, and Connecticut). We find that the majority of national firms in the goods and retail sectors reported experiencing financial challenges due to tariffs in 2025, with even larger shares of regional firms doing so. In response, about 80 percent of national and regional firms passed on at least some of the higher costs of imported inputs to customers, while about 60 percent absorbed some of the costs, as many firms did some of both. Firms that faced greater tariff challenges in 2025 were more pessimistic about employment and revenues in 2026.

July 8, 2026

More Tariff Pass‑Through Is in the Pipeline

The past year brought dramatic changes to U.S. trade policy, including sweeping new tariffs, as well as a Supreme Court decision that further reshaped the tariff landscape. Many businesses saw their costs increase significantly and faced complex decisions about whether to absorb the tariffs through lower profit margins, raise their prices to recover the higher costs, or some combination of the two. Last year, we found that most businesses had passed on at least some of these higher costs to their customers through higher prices. Now, over a year later, have businesses finished adjusting prices, or do further tariff-induced price increases lie ahead? Our latest regional business surveys reveal that nearly half of firms that have paid tariffs still plan additional price increases to offset these costs, with some expecting to raise prices six months or more in the future.

July 7, 2026

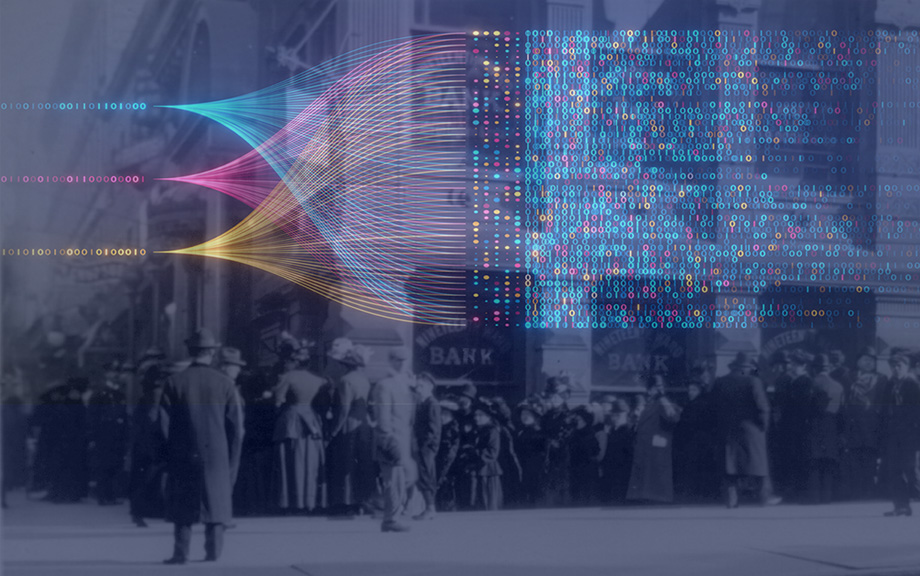

Using AI to Let History Speak About Bank Runs

Banking crises are commonly associated with bank runs and banking panics, yet our empirical understanding of bank runs is constrained by a lack of bank-level data. In a new paper, we use large language models (LLMs) to extract information on bank runs from millions of digitized historical newspaper pages, creating the most comprehensive database of bank runs in U.S. history. Every bank run episode that we identify is documented on a companion website where users can browse and examine individual episodes, and read the original newspaper articles. In this post, we describe how we built this dataset and discuss what its basic features reveal.

Posted at 10:00 am in Artificial Intelligence (AI), Banks, Crisis, Liquidity | Permalink | Comments (0)

July 1, 2026

The Disappearing Overnight Drift

In a 2021 Liberty Street Economics post, we documented the “overnight drift”—a large, persistent return to holding U.S. equity futures in the narrow window between 2:00 and 3:00 a.m. Eastern time, when European equity markets open. Five additional years of data later, that pattern appears to have faded: the 2:00–3:00 window that previously generated roughly 3.7 percent per annum has averaged close to zero since 2021. In this post, we revisit the overnight drift in light of the post-publication sample and use our inventory-risk framework to ask which of three observable channels—the dispersion of closing order imbalances, the level of return variance, or the risk-bearing capacity of liquidity providers—accounts for the change.

June 30, 2026

Liquidity Fades as Treasuries Age

More than $30 trillion U.S. Treasury debt is outstanding. Less than 4 percent of this amount, which is associated with the most recently issued Treasuries, called on-the-run securities, accounts for 65 percent of average daily trading volume. The remaining portion of the amount outstanding is accounted for by seasoned issues that have been replaced by newer benchmarks, which are referred to as off-the-run securities. In this post, we review the key results in our paper that uses transaction-level Treasury TRACE data to study how trading activity and liquidity evolve as securities move from on-the-run to off-the-run. We show three main patterns. First, off-the-run notes and bonds rely much more on dealer-to-customer intermediation than benchmark securities. Second, trading activity falls sharply and transaction costs increase as securities age. Third, securities that are cheapest to deliver into Treasury futures are an important exception: they trade more actively than other off-the-run bonds of similar age.

June 26, 2026

How Resilient Were Emerging Market Economies Through the 2022‑23 U.S. Monetary Tightening Cycle?

The cross-border spillover effects of shifts in U.S. monetary policy have long been a focus of academics and policymakers alike. A common finding in the literature is that changes in the stance of U.S. monetary policy have sizable effects on economic activity and financial markets in emerging market economies (EMEs). In this post, we analyze one specific aspect of these spillovers: how EMEs fared through the U.S. monetary policy tightening cycle of 2022-23 relative to the predictions of a model, which was calibrated to capture empirically relevant features of these economies based on historical data. We find that more vulnerable EMEs fared better in both financial market and growth outcomes than would be expected from our model, while the relatively less vulnerable fared a bit better than the model predictions for financial outcomes but substantially worse for growth outcomes.

June 24, 2026

The Post‑COVID Decline in the Labor Share

The labor share of income in the U.S. is currently at its lowest-ever level in the post-war period. The labor share measures the fraction of economic output paid to workers as wages and salaries. As such, it is a useful benchmark for wage growth: when the labor share falls, it means that productivity, prices, or both are growing faster than wages. After much-studied drops in the 2000s, the labor share fell sharply again after the COVID pandemic. In this post, we compare the dynamics of the labor share post-COVID to earlier periods to understand whether the recent decline represents the continuation of a trend or a new and distinct phenomenon. We find that both the cyclicality of the labor share and the contribution of reallocation to the labor share post-COVID are similar to earlier periods.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics