354 posts on "Liberty Street Economics"

December 20, 2024

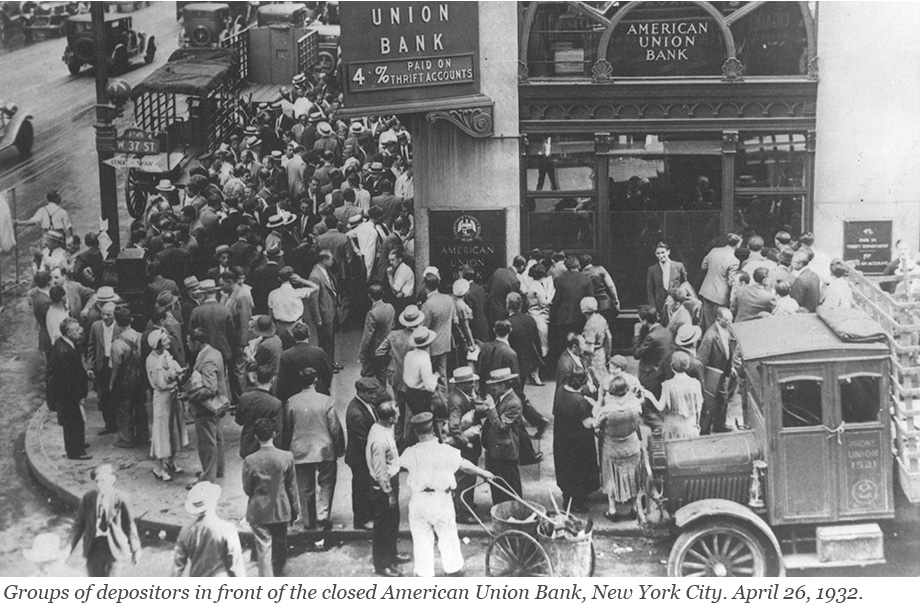

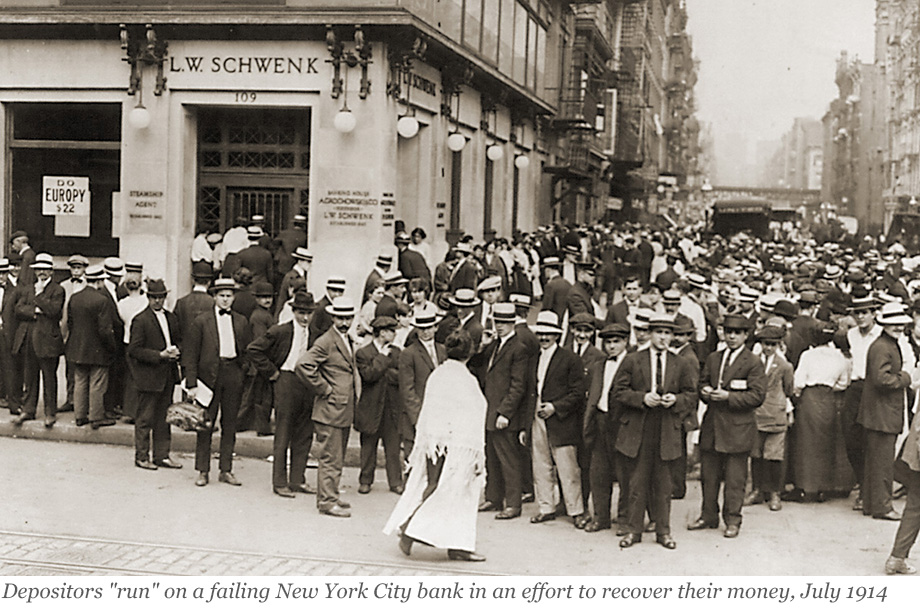

Anatomy of the Bank Runs in March 2023

Runs have plagued the banking system for centuries and returned to prominence with the bank failures in early 2023. In a traditional run—such as depicted in classic photos from the Great Depression—depositors line up in front of a bank to withdraw their cash. This is not how modern bank runs occur: today, depositors move money from a risky to a safe bank through electronic payment systems. In a recently published staff report, we use data on wholesale and retail payments to understand the bank run of March 2023. Which banks were run on? How were they different from other banks? And how did they respond to the run?

Posted at 6:30 am in Banks, Crisis, Financial Institutions, Lender of Last Resort, Panic | Permalink | Comments (1)

December 4, 2024

Using Stock Returns to Assess the Aggregate Effect of the U.S.‑China Trade War

During 2018-19, the U.S. levied import tariffs of 10 to 50 percent on more than $300 billion of imports from China, and in response China retaliated with high tariffs of its own on U.S. exports. Estimating the aggregate impact of the trade war on the U.S. economy is challenging because tariffs can affect the economy through many different channels. In addition to changing relative prices, tariffs can impact productivity and economic uncertainty. Moreover, these effects can take years to become apparent in the data, and it is difficult to know what the future implications of a tariff are likely to be. In a recent paper, we argue that financial market data can be very useful in this context because market participants have strong incentives to carefully analyze the implications of a tariff announcement on firm profitability through various channels. We show that researchers can use movements in asset prices on days in which tariffs are announced to obtain estimates of market expectations of the present discounted value of firm cash flows, which then can be used to assess the welfare impact of tariffs. These estimates suggest that the trade war between the U.S. and China between 2018 and 2019 had a negative effect on the U.S. economy that is substantially larger than past estimates.

December 3, 2024

Documenting Lender Specialization

Robust banks are a cornerstone of a healthy financial system. To ensure their stability, it is desirable for banks to hold a diverse portfolio of loans originating from various borrowers and sectors so that idiosyncratic shocks to any one borrower or fluctuations in a particular sector would be unlikely to cause the entire bank to go under. With this long-held wisdom in mind, how diversified are banks in reality?

November 25, 2024

Why Do Banks Fail? Bank Runs Versus Solvency

Evidence from a 160-year-long panel of U.S. banks suggests that the ultimate cause of bank failures and banking crises is almost always a deterioration of bank fundamentals that leads to insolvency. As described in our previous post, bank failures—including those that involve bank runs—are typically preceded by a slow deterioration of bank fundamentals and are hence remarkably predictable. In this final post of our three-part series, we relate the findings discussed previously to theories of bank failures, and we discuss the policy implications of our findings.

November 22, 2024

Why Do Banks Fail? The Predictability of Bank Failures

Can bank failures be predicted before they happen? In a previous post, we established three facts about failing banks that indicated that failing banks experience deteriorating fundamentals many years ahead of their failure and across a broad range of institutional settings. In this post, we document that bank failures are remarkably predictable based on simple accounting metrics from publicly available financial statements that measure a bank’s insolvency risk and funding vulnerabilities.

November 21, 2024

Why Do Banks Fail? Three Facts About Failing Banks

Why do banks fail? In a new working paper, we study more than 5,000 bank failures in the U.S. from 1865 to the present to understand whether failures are primarily caused by bank runs or by deteriorating solvency. In this first of three posts, we document that failing banks are characterized by rising asset losses, deteriorating solvency, and an increasing reliance on expensive noncore funding. Further, we find that problems in failing banks are often the consequence of rapid asset growth in the preceding decade.

November 14, 2024

Why Investment‑Led Growth Lowers Chinese Living Standards

Rapid GDP growth, due in part to high rates of investment and capital accumulation, has raised China out of poverty and into middle-income status. But progress in raising living standards has lagged, as a side-effect of policies favoring investment over consumption. At present, consumption per capita stands some 40 percent below what might be expected given China’s income level. We quantify China’s consumption prospects via the lens of the neoclassical growth model. We find that shifting the country’s production mix toward consumption would raise both current and future living standards, with the latter result owing to diminishing returns to capital accumulation. Chinese policy, however, appears to be moving in the opposite direction, to reemphasize investment-led growth.

October 21, 2024

The Dueling Intraday Demands on Reserves

A central use of reserves held at Federal Reserve Banks (FRBs) is for the settlement of interbank obligations. These obligations are substantial—the average daily total reserves used on two main settlement systems, Fedwire Funds and Fedwire Securities, exceeds $6.5 trillion. The total amount of reserves needed to efficiently settle these obligations is an active area of debate, especially as the Federal Reserve’s current quantitative tightening (QT) policy seeks to drain reserves from the financial system. To better understand the use of reserves, in this post we examine the intraday flows of reserves over Fedwire Funds and Fedwire Securities and show that the mechanics of each settlement system result in starkly different intraday demands on reserves and differing sensitivities of those intraday demands to the total amount of reserves in the financial system.

October 1, 2024

Are Nonbank Financial Institutions Systemic?

Recent events have heightened awareness of systemic risk stemming from nonbank financial sectors. For example, during the COVID-19 pandemic, liquidity demand from nonbank financial entities caused a “dash for cash” in financial markets that required government support. In this post, we provide a quantitative assessment of systemic risk in the nonbank sectors. Even though these sectors have heterogeneous business models, ranging from insurance to trading and asset management, we find that their systemic risk has common variation, and this commonality has increased over time. Moreover, nonbank sectors tend to become more systemic when banking sector systemic risk increases.

September 25, 2024

Flood Risk Outside Flood Zones — A Look at Mortgage Lending in Risky Areas

In support of the National Flood Insurance Program (NFIP), the Federal Emergency Management Agency (FEMA) creates flood maps that indicate areas with high flood risk, where mortgage applicants must buy flood insurance. The effects of flood insurance mandates were discussed in detail in a prior blog series. In 2021 alone, more than $200 billion worth of mortgages were originated in areas covered by a flood map. However, these maps are discrete, whereas the underlying flood risk may be continuous, and they are sometimes outdated. As a result, official flood maps may not fully capture the true flood risk an area faces. In this post, we make use of unique property-level mortgage data and find that in 2021, mortgages worth over $600 billion were originated in areas with high flood risk but no flood map. We examine what types of lenders are aware of this “unmapped” flood risk and how they adjust their lending practices. We find that—on average—lenders are more reluctant to lend in these unmapped yet risky regions. Those that do, such as nonbanks, are more aggressive at securitizing and selling off risky loans.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics