257 posts on "Macroeconomics"

July 13, 2023

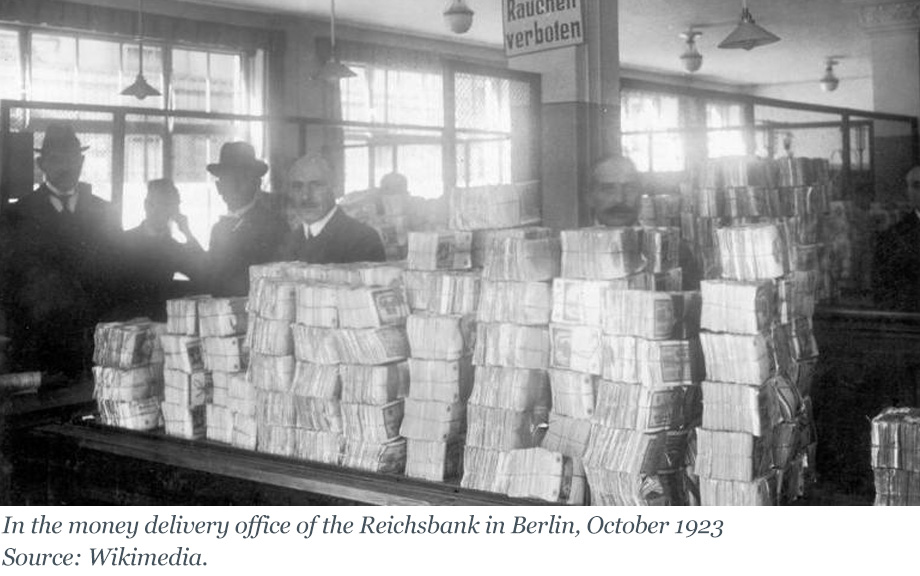

Inflating Away the Debt: The Debt‑Inflation Channel of German Hyperinflation

The recent rise in price pressures around the world has reignited interest in understanding how inflation transmits to the real economy. Economists have long recognized that unexpected surges of inflation can redistribute wealth from creditors to debtors when debt contracts are written in nominal terms (see, for example, Fisher 1933). If debtors are financially constrained, this redistribution can affect real economic activity by relaxing financing constraints. This mechanism, which we call the debt-inflation channel, is well understood theoretically (for example, Gomes, Jermann, and Schmid 2016), but there is limited empirical evidence to substantiate it. In this post, we discuss new insights from one of the key events in monetary history: the Great German Inflation of 1919-23. Because this case of inflation was both surprising and extremely high, Germany’s experience helps shed light on how high inflation impacts firms’ economic activity through the erosion of their nominal debt burdens. These insights are based on a recently released research paper.

July 6, 2023

Where Is Inflation Persistence Coming From?

Elevated inflation continues to be a top-of-mind preoccupation for households, businesses, and policymakers. Why has the post-pandemic inflation proved so persistent? In a Liberty Street Economics post early in 2022, we introduced a measure designed to dissect the buildup of the inflationary pressures that emerged in mid-2021 and to understand where the sources of its persistence are. This measure, that we labeled Multivariate Core Trend (MCT) inflation analyzes whether inflation is short-lived or persistent, and whether it is concentrated in particular economic sectors or broad-based.

June 23, 2023

The Credibility of Government Policies: Conference in Honor of Guillermo Calvo

Guillermo Calvo is a leading member of a group of economists who revolutionized macroeconomics by modeling how incentives and the anticipation of future policies affect aggregate outcomes. In celebration of his work, a conference was held in his honor at the Federal Reserve Bank of New York and at Columbia University on February 22-24, 2023. The conference program can be found on the event website. A longer version of this post with additional detail on the proceedings can be found here.

June 16, 2023

The New York Fed DSGE Model Forecast— June 2023

Editor's note: We have updated the "date of forecast" row in the forecast comparison table to display the correct year (2023, not 2024). (September 25, 2023, 5:04 p.m.)

This post presents an update of the economic forecasts generated by the Federal Reserve Bank of New York’s dynamic stochastic general equilibrium (DSGE) model. We describe very briefly our forecast and its change since March 2023.

June 2, 2023

MCT Update: Inflation Persistence Declined Significantly in April

This post presents an updated estimate of inflation persistence, following the release of personal consumption expenditure (PCE) price data for April 2023. The estimates are obtained by the Multivariate Core Trend (MCT), a model we introduced on Liberty Street Economics last year and covered most recently in a May post. The MCT is a dynamic factor model estimated on monthly data for the seventeen major sectors of the PCE price index. It decomposes each sector’s inflation as the sum of a common trend, a sector-specific trend, a common transitory shock, and a sector-specific transitory shock. The trend in PCE inflation is constructed as the sum of the common and the sector-specific trends weighted by the expenditure shares.

May 31, 2023

Do Economic Crises in Europe Affect the U.S.? Some Lessons from the Past Three Decades

In this post we summarize the main results of our contribution to a recent e-book, “The Making of the European Monetary Union: 30 years since the ERM crisis,” on the economic and financial crises in Europe since 1992-93, and focus on the spillovers of those crises onto the United States and the global economy. We find that the answer to the question in the title of this post is a (moderate) yes.

Posted at 7:00 am in Credit, Crisis, DSGE, Euro Area, Exchange Rates, Exports, International Economics, Macroeconomics | Permalink

May 23, 2023

Financial Stability and Interest Rates

In a recent research paper we argue that interest rates have very different consequences for current versus future financial stability. In the short run, lower real rates mean higher asset prices and hence higher net worth for financial institutions. In the long run, lower real rates lead intermediaries to shift their portfolios toward risky assets, making them more vulnerable over time. In this post, we use a model to highlight the challenging trade-offs faced by policymakers in setting interest rates.

May 17, 2023

Look Out for Outlook‑at‑Risk

The timely characterization of risks to the economic outlook plays an important role in both economic policy and private sector decisions. In a February 2023 Liberty Street Economics post, we introduced the concept of “Outlook-at-Risk”—that is, the downside risk to real activity and two-sided risks to inflation. Today we are launching Outlook-at-Risk as a regularly updated data product, with new readings for the conditional distributions of real GDP growth, the unemployment rate, and inflation to be published each month. In this post, we use the data on conditional distributions to investigate how two-sided risks to inflation and downside risks to real activity have evolved over the current and previous five monetary policy tightening cycles.

Posted at 10:00 am in Central Bank, Financial Markets, Forecasting, Macroeconomics, Monetary Policy | Permalink

May 10, 2023

Assessing the Outlook for Employment across Industries

Job gains exceeded output growth in 2022, bringing GDP per worker back down to its trend level after being well above for an extended period. Employment is consequently set to grow slower than output going forward, as it typically does. Breaking down the GDP per worker by industry, though, shows a significant divergence between the services and goods-producing sectors. Productivity in the services sector was modestly above its pre-pandemic path at the end of last year, suggesting room for relatively strong employment growth, with the gap particularly large in the health care, professional and business services, and leisure and hospitality sectors. Productivity in goods-producing industries, though, was depressed, implying that payroll growth is set to lag that sector’s GDP growth.

May 5, 2023

MCT Update: Inflation Persistence Continued to Decline in March

This post presents an updated estimate of inflation persistence, following the release of personal consumption expenditure (PCE) price data for March 2023. The estimates are obtained by the Multivariate Core Trend (MCT), a model we introduced on Liberty Street Economics last year and covered most recently in a March post. The MCT is a dynamic factor model estimated on monthly data for the seventeen major sectors of the PCE price index. It decomposes each sector’s inflation as the sum of a common trend, a sector-specific trend, a common transitory shock, and a sector-specific transitory shock. The trend in PCE inflation is constructed as the sum of the common and the sector-specific trends weighted by the expenditure shares.

RSS Feed

RSS Feed Follow Liberty Street Economics

Follow Liberty Street Economics